Short Volatility

One of the paramount goals when trading the financial markets is to maximize potential gains. Secondarily, most traders would likely prefer to minimize risk.

If you are trading short premium, there are a couple simple guidelines to follow which can arguably help with both.

These include the application of a trade management system; in tandem with filtering for only the best short premium opportunities—as outlined on a recent episode of Market Measures on the tastytrade financial network.

The great thing about this particular installment of the series is that the hosts use several helpful graphics to illustrate the power of these tactics, which consequently reduces the time needed to absorb the information.

Prior to jumping into the meat of the material, a short word on trade management.

In this context, trade management refers to a systematic approach to managing positions in a portfolio. Management when trading options is necessary because traders ultimately have two choices when it comes to closing a trade: it can be closed prior to expiration (active), or it can be left to expire on its own (passive).

While each approach may have merit, depending on one’s unique strategic approach and risk profile, research utilizing historical market data has consistently shown that active trade management can help with trade performance and optimization.

The aforementioned episode of Market Measures presents new tastytrade research that helps illustrate the power of trade management when combined with filtering for only the best short premium opportunities, and the tactics discussed on the show should help traders optimize their own approaches going forward.

Without further ado, a brief review of said research. The centerpiece of the show is a recently conducted tastytrade market research study.

Similar to previous studies, this involves the clear identification of a trading approach or strategy, which is then backtested using historical market data. tastytrade studies such as these typically involve tweaking the approach slightly and rerunning the backtest in order to compare how different filters and/or trade signals affect overall trade performance.

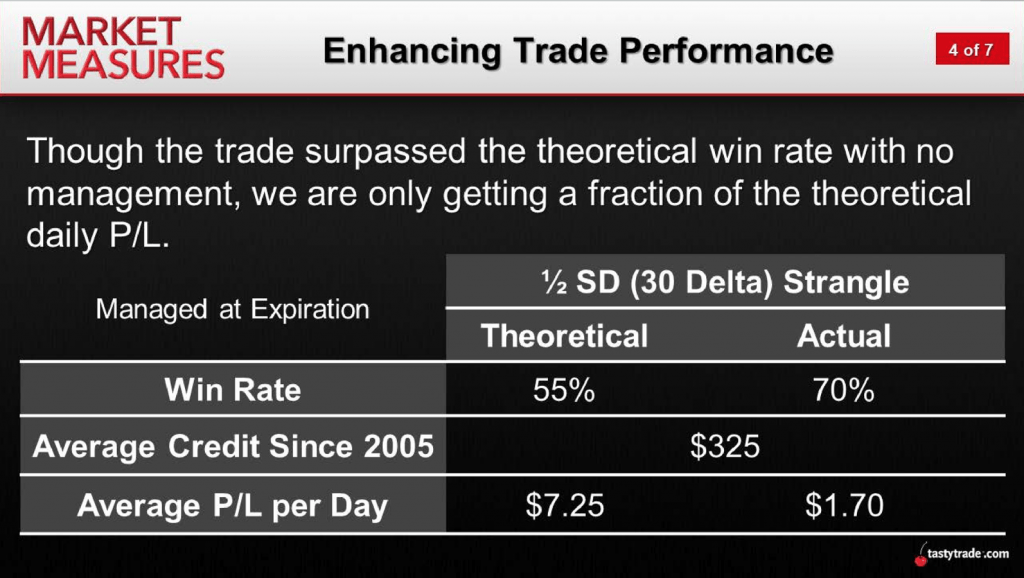

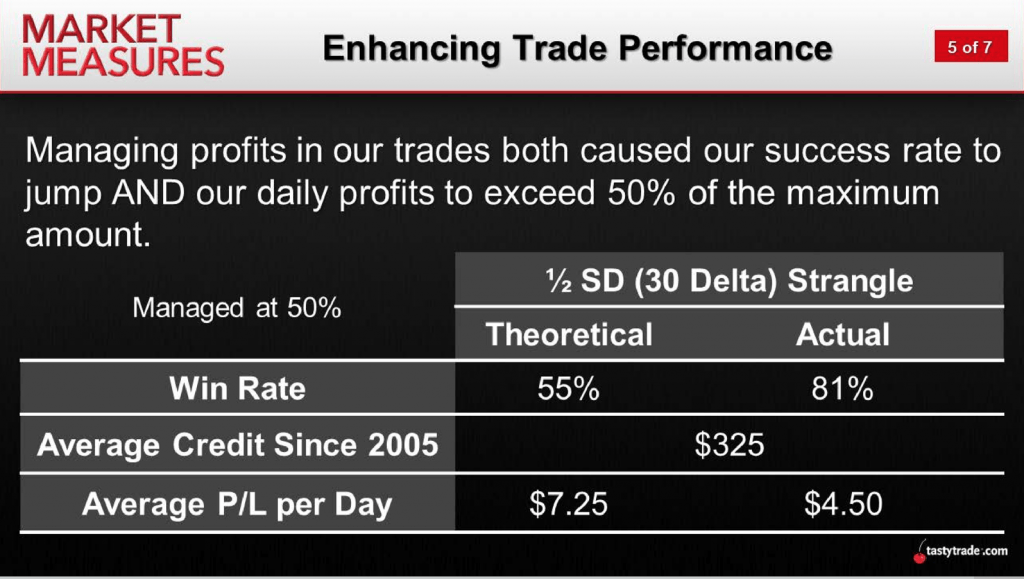

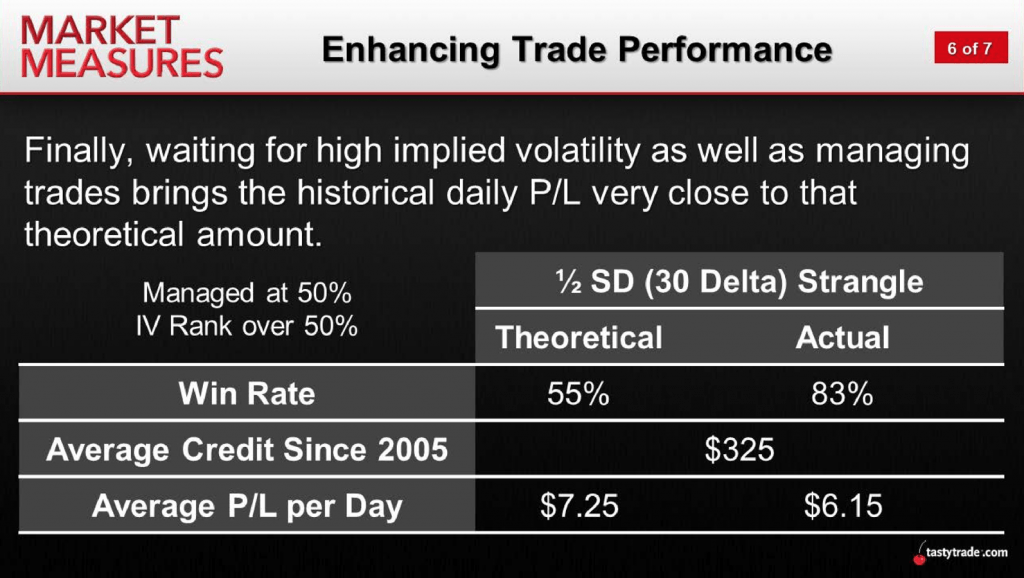

In this case, the goal was to backtest a short strangle (30 delta on each side) in SPY, using data from 2005 to present. The short strangle is an oft-used and well-known trading structure that is often tapped when short volatility opportunities present themselves.

The first backtest in the study simply evaluated the historical performance of the short strangle in SPY over the entire period covered (i.e. “all instances”). The results of this backtest provide the benchmark level of performance which can then be compared to additional backtests—backtests that involve slight adjustments to the trading approach.

For this particular study, the backtest was run two additional times. Once to examine how overall trade performance was affected when a simple trade management approach was applied, and then again to examine how trade performance was affected when both a trade management filter was applied as well as a filter for a minimum threshold of volatility.

The trade management filter applied to the second backtest is one often utilized at tastytrade, known as “50% of credit received.” In more detailed terms, this trade management approach calls for the automatic closure of a short premium trade when it achieves 50% of maximum profit.

In the third backtest, which included a minimum threshold for selling volatility, the metric used to filter trades was Implied Volatility Rank (IVR), specifically greater than 50%. To learn more about IVR, this summary is highly recommended.

The true power of this study is derived from a summarized presentation of the findings.

The first graphic below summarizes the performance of the short strangle in SPY across “all instances.” The second slide below summarizes the performance of the short strangle when coupled with a trade management approach. The third illustrates how the strategy performed when coupled with both a trade management approach, as well as a minimum volatility threshold (greater than 50% IVR).

Looking at the three graphics above, the most important trends to highlight are the improvement in the average win rate, and the average P/L per day produced when both the trade management and minimum volatility thresholds are layered into the simple short strangle approach.

As one can see in those respective columns, the performance of the short strangle consistently improves in terms of win rate and average P/L when coupled with two relatively straightforward strategic “enhancers.” While past results aren’t an indicator of future results, the findings from this study remain compelling.

Traders unfamiliar with such tactics may want to “mock trade” such tactics before applying them “live” in their portfolios. Mock trading (aka paper trading) allows traders to learn the behavior of a new strategy or tactic without the associated risk of capital losses.

Those seeking to review this study in greater detail are encouraged to review the complete episode of Market Measures when scheduling allows.For more information on the trade management philosophy, traders can also review this past installment of Market Measures, which serves as a great complement to the material discussed in this post.

Sage Anderson is a pseudonym. The contributor has an extensive background in trading equity derivatives and managing volatility-based portfolios as a former prop trading firm employee. The contributor is not an employee of luckbox, tastytrade or any affiliated companies. Readers can direct questions about topics covered in this blog post, or any other trading-related subject, to support@luckboxmagazine.com.