Rising Rates Could Pinch Hot Housing Market Later This Year

The red-hot U.S. housing market hasn’t slowed down in 2021, with low inventories and strong demand now catalyzing bidding wars in some parts of the country.

Strange times, and they may be getting even stranger. Take, for instance, the U.S. housing market.

Last year, amid the global pandemic, housing prices in the U.S. increased by 8.4%, on average.

This year, that trend has endured, and may actually be accelerating. Data released by Case-Shiller indicated that the National House Price Index in the United States increased by 11.2% in January (year-over-year).

And stories emerging from the real estate trenches suggest that prices should climb higher in the near term.

In 2020, the housing market was low on inventory and high on prices. Early returns suggest that the 2021 housing market may be even tighter on inventory, and consequently even higher on prices.

The real estate market in the U.S. has actually gotten so overheated that the somewhat worrisome “bidding war” trend has once again emerged. That’s right, there are so few homes up for sale these days that buyers are submitting bids at the asking price, only to find that others in the market have bid more.

The competition for homes has gotten so extreme that one real estate agent in Florida recently reported that a single-family home had received more than 30 separate bids.

In February, Redfin (RDFN) released data indicating that homes are going under contract after only 32 days on the market on average. That’s 23 days faster than the year prior. More importantly, 36% of home sales in February went for more than the original asking price.

Altogether, that means the market dynamics in 2021 appear to be similar to 2020, if not a bit more extreme. Not surprisingly, it appears that much of the same market factors are still in play.

Just like in 2020, the ultra-low interest rate environment in the U.S. appears to be reeling in especially motivated buyers. Beyond that, the ongoing pandemic continues to cap available inventory.

Last year, it was estimated that available housing inventory in the U.S. was 20% lower than in 2019—mostly due to eviction and foreclosure moratoriums associated with the pandemic. Currently, estimates suggest there are at least 8 million Americans behind on rent, and more than 3 million behind the eight ball on their mortgages.

The unique challenges presented by the pandemic have essentially created an inventory crisis, with fresh reports suggesting that available housing stock is even more limited this year than it was in 2020—down 50% (March 2020 vs. March 2021).

Given the close relationship between supply and demand in economics, it’s no wonder prices are rising accordingly. And there’s no telling when the situation might be alleviated.

On March 28, the nationwide moratorium on evictions and foreclosures was extended to the end of June—meaning any significant increase in housing inventories is likely a pipe dream in the near term.

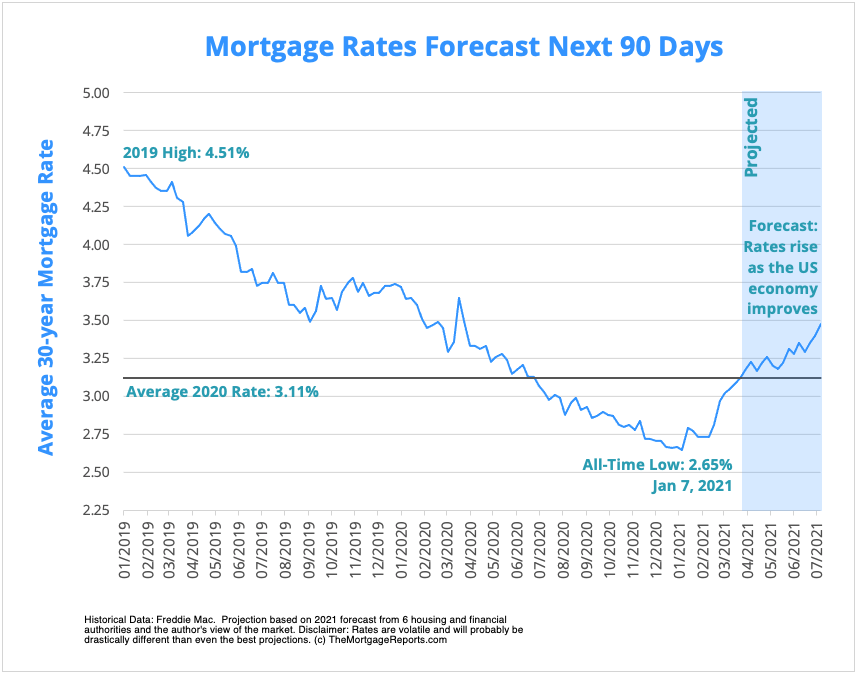

The one wrinkle in 2021, as compared to 2020, is the fact that interest rates have been rising. At the end of March 2021, the 30-year mortgage rate averaged roughly 3.17%. At the start of the year, that rate was closer to 2.65%.

Projections suggest that home buying activity could slow down once 30-year rates start trading above 3.5%. That means the recent home-buying frenzy—and associated bidding wars—may be short-lived. Maybe.

Ultimately, the future of the housing market could also hinge on whether the current vaccination campaign in the U.S. is successful in quelling another serious wave of COVID-19 cases. The same can likely be said for the broader U.S. economy.

Barring a worst-case scenario, it’s hard to envision the moratorium on evictions and foreclosures being extended beyond summer 2021. So at some point this fall, a flood of new inventory could hit the market—a development that could finally slow the rate at which housing prices have been rising.

And if the U.S. economy continues to flounder, a rising supply of inventory could even push housing prices lower—reversing the recent trend.

To track and trade the U.S. housing sector, investors and traders may want to add the following symbols to their watchlists: D.R. Horton (DHI), iShares U.S. Home Construction ETF (ITB), KB Homes (KBH), Invesco Dynamic Building & Construction ETF (PKB), PulteGroup (PHM), Realogy (RLGY), Redfin (RDFN), Re/Max (RMAX), Toll Brothers (TOL), SPDR S&P Homebuilders ETF (XHB) and Zillow (Z).

For more information about trading interest rates using Treasury yields, readers may also want to visit the Small Exchange.

Offer extended through April 1st: Subscribe to Luckbox in print and get a FREE Luckbox T-shirt!

See SUBSCRIBE or UPGRADE TO PRINT (upper right) for more info.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.