Trading the Latest Bloodbath in U.S.-listed Shares of Chinese Stocks

U.S.-listed stocks from China have suffered this year, and the pressure is increasing in the wake of the country’s recent National Congress, with shares sliding toward 52-week lows

Global stocks have been under pressure throughout 2022, but the carnage in Chinese-affiliated stocks has been especially savage.

Chinese-exposed stocks—especially in the technology sector—have been facing several key headwinds this year, including severe regulatory pressure at home and the possibility of a mass delisting from American exchanges.

However, in the last couple of weeks, a couple of new concerns have been added to the pile.

At the top of the list has been a crackdown on new Chinese initial public offerings (IPOs) in the United States—particularly of the small-cap variety. This fresh round of regulatory pressure appears to stem from the fact that some small-cap Chinese IPOs have been making gargantuan (and seemingly inexplicable) moves of late.

One instance might be considered an anomaly, but after a spate of these crazy moves, regulators and exchange operators have apparently had enough and are suspicious that illegal market manipulation may be involved.

For the time being, the Nasdaq Stock Market has stopped approving the IPOs of small-cap stocks from China. The Nasdaq is currently conducting due diligence into the “interested parties” of such deals.

This narrative first popped up on the radar back in July, when AMTD Digital (HKD) jumped over 150% on its first day of trading.

HKD then proceeded to rally by another 15,000% from mid-July through early August. Importantly, the company made no material announcements during this period, meaning there weren’t clear grounds for HKD’s meteoric appreciation in value.

On a one-off basis, regulators, exchange operators, and market participants may have been able to explain that situation away as a perplexing market anomaly. However, a similar situation unfolded again in early August when the Hong-Kong based financial company named Magic Empire Global (MEGL) experienced a similar surge—climbing by more than 2,000% on its first day of trading.

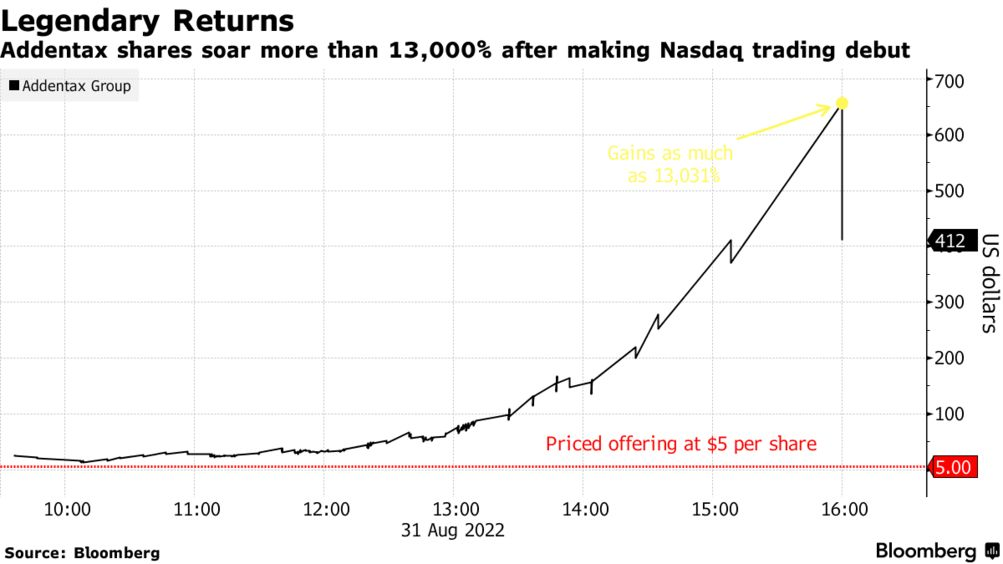

Then, later in August, shares in the Addentax Group (ATXG) soared by more than 13,000% after the Chinese garment maker was uplisted to the Nasdaq on Aug. 31 (illustrated below). Considering this series of events, it’s no great surprise that action is being taken to better understand what’s behind this unusual market activity.

Zero-COVID approach slows Chinese economy

Unfortunately, strange moves in small-cap stocks aren’t the end of the story when it comes to recent action in Chinese-affiliated shares. Chinese stocks listed in the U.S. got slammed across the board after President Xi Jinping was promoted to a third term in China in late October.

While it’s never easy to pinpoint the exact reason for a sharp pullback in asset values, one of the prevailing concerns appears to stem from the Chinese leader’s continued support for a “zero-COVID” approach in the mainland.

Zero-COVID refers to an umbrella public health policy in China which leverages stringent measures to stop the spread of the virus. This approach features continuous mass testing of the population, as well as rolling lockdowns in neighborhoods/districts/cities/regions to help prevent the spread of infection.

Unfortunately, these tight controls have had a significant negative impact on China’s underlying economy. Businesses in China simply haven’t been able to operate normally in the current environment, which has adversely affected overall production.

Case in point, the official purchasing managers’ index for manufacturing in China fell to 49.2 this month, down from 50.1 in September, according to China’s National Bureau of Statistics. Moreover, sub-indicators on factory employment, production, new orders and supplier delivery time all suffered contractions from September to October.

In 2022, Chinese economic growth has been relatively thin—lagging behind greater Asia for the first time since 1990. Asia, excluding China, is expected to grow by about 5.3% in 2022. In comparison, China’s economy is expected to grow by under 3% this year.

Slowing growth in China has undoubtedly weighed on Chinese stocks, and the continuance of the zero-COVID approach has clearly been interpreted as an incremental negative.

On Oct. 24—the day after China’s National Congress adjourned—Chinese stocks experienced a sharp selloff. That day, tech bellwethers like Alibaba (BABA), JD.com (JD), and Baidu (BIDU) were all down nearly 15%. The KraneShares CSI China Internet ETF (KWEB)—a closely followed China ETF—likewise slumped by 14%.

Going forward, that means Chinese stocks will face not only regulatory pressure back home and the potential for a mass delisting from U.S. exchanges, but also the continued negative impact of stringent COVID-19 controls, as well as a temporary halt on new listings in the U.S.

The big question going forward is whether the most recent nosedive in Chinese shares represents an opportunity, or a sign that bigger problems lie ahead.

For daily updates on everything moving the markets—including Chinese stocks—monitor TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.