Trading the Post-Earnings Volatility Crush

Corporate earnings season is usually a treat for options traders. Opportunities multiply as implied volatility swirls in different directions across a wide swath of symbols.

And while most traders have already identified how they like to approach an “earnings play,” the post-earnings playbook can be less robust. Post-earnings depression for volatility traders can be a bit like the empty feeling football fans experience after the Super Bowl.

But does that need to be the case?

According to research conducted by tastytrade, the aftermath of earnings season may be just as bountiful as earnings season itself—depending on one’s unique trading approach and risk profile.

On a previous installment of Market Measures, data is presented that helps illuminate the value of staying active in the volatility market even after earnings have been announced.

And given that the uncertainty surrounding these events has passed, this approach may actually represent less risk when compared to trading the actual earnings events themselves.

As most options traders are already well aware, corporate earnings announcements are usually accompanied by a run-up in implied volatility—especially in the expiration month that captures the release.

This is due to the fact that earnings are somewhat unpredictable, and can potentially catalyze big moves in the underlying stock. But once the “event” has passed, the market has theoretically received a comprehensive update on all pertinent financial and operational data relating to the company in question.

Given those realities, one might wonder what could move the stock going forward.

Some scenarios include a stock-specific merger or acquisition, or a broad-based macro event that catalyzes a big move in equity indices. But those are risks facing options traders on any given day, not just after earnings.

A more pertinent question therefore revolves around how long and short premium trading approaches have historically performed in the wake of earnings. And the fact that implied volatility tends to get “crushed” after earnings is one important dynamic to keep in mind when considering one’s strategic positioning.

One hypothesis is that lowered levels of implied volatility after earnings might provide traders with a good opportunity to purchase premium. However, the results of a comprehensive market study conducted by tastytrade suggest otherwise, and serve as a great reminder that low implied volatility doesn’t necessarily equate to “cheap” implied volatility.

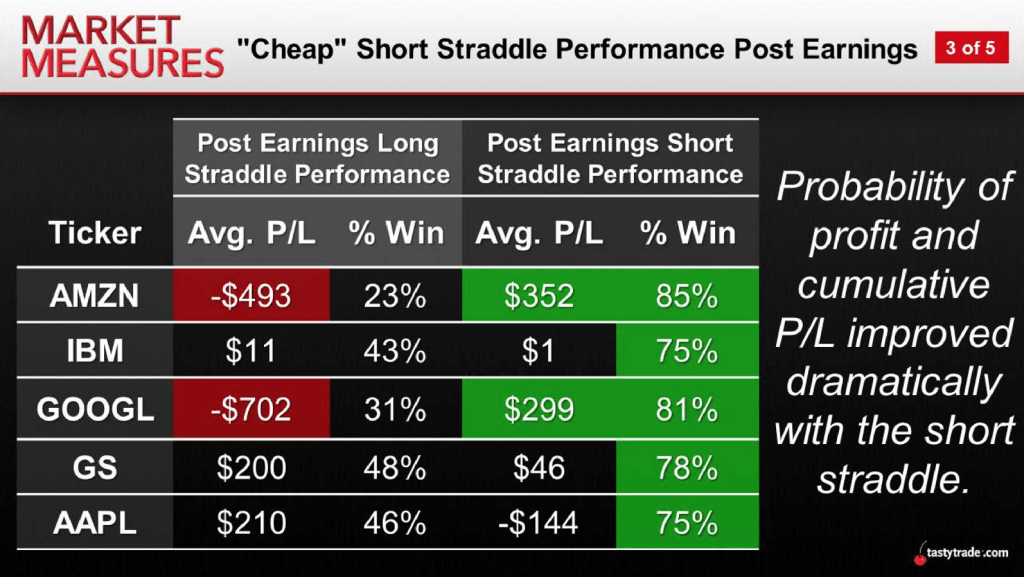

In order to produce the data necessary for the aforementioned analysis, the Market Measures team at tastytrade designed a study using 12 years of historical earnings data for five different symbols: AMZN, IBM, GOOG, GS, and AAPL.

The study hinged on two different backtests, the first of which evaluated the historical performance of a long premium trading approach deployed after earnings, and the second evaluated the historical performance of a short premium approach deployed after earnings.

The study included the following parameters:

- Backtest 1: Studied the performance of short straddles after earnings

- Backtest 2: Studied the performance of long straddles after earnings

- Trade entry: End-of-day after earnings release

- Symbols included: AMZN, IBM, GOOG, GS, AAPL

- Period studied: 12 years

- Total trades involved: 256

The graphic below summarizes the results from these two backtests—selling premium after the “earnings crush” as compared to buying premium after the earnings crush.

At first glance, the above data might raise a few eyebrows, especially given the most glaring trend observed in the findings: the success rate of selling premium even after implied volatility has gotten crushed.

As one can see in the graphic above, the winning percentage for the short straddle approach was attractive for all five symbols. Likewise, selling premium after earnings produced a positive P/L (on average) for four of the five symbols included in the study.

In contrast to those results, the data illustrated that the deployment of a long straddle trading approach after earnings produced a win rate that was less than 50% in each of the five symbols backtested. Likewise, the average P/L for two of the five symbols included in the long premium backtest are considered “outsized” in terms of the degree of the losses.

While GS and AAPL did produce an average P/L that was positive for long straddles deployed after earnings, one must keep in mind that this was after the “earnings crush,” which provides a great illustration of just how low implied volatility needs to get before a long volatility approach can produce even semi-attractive returns.

Overall, one of the important takeaways from the study is the fact that win rates for the short premium approach remained very high, even after implied volatility got hammered.

While the reason for this can’t be known exactly (due to the wide variety of factors in play), the theory that earnings announcements remove some uncertainty from the volatility equation is probably at least partially valid.

On the other hand, there was some mild success on the long premium side as well, which may indicate there’s merit in filtering for the best possible opportunities after earnings—whether they be “cheap” or “expensive” volatilities.

Traders seeking to learn more about this tastytrade study focusing on the historical performance of both long and short premium strategies deployed after earnings may want to review the complete episode of Market Measures when scheduling allows.Additional information relating to the earnings trade is also available in the tastytrade LEARN CENTER.

Sage Anderson is a pseudonym. The contributor has an extensive background in trading equity derivatives and managing volatility-based portfolios as a former prop trading firm employee. The contributor is not an employee of luckbox, tastytrade or any affiliated companies. Readers can direct questions about topics covered in this blog post, or any other trading-related subject, to support@luckboxmagazine.com.