Ghost Recession Could Get Scary in Fall

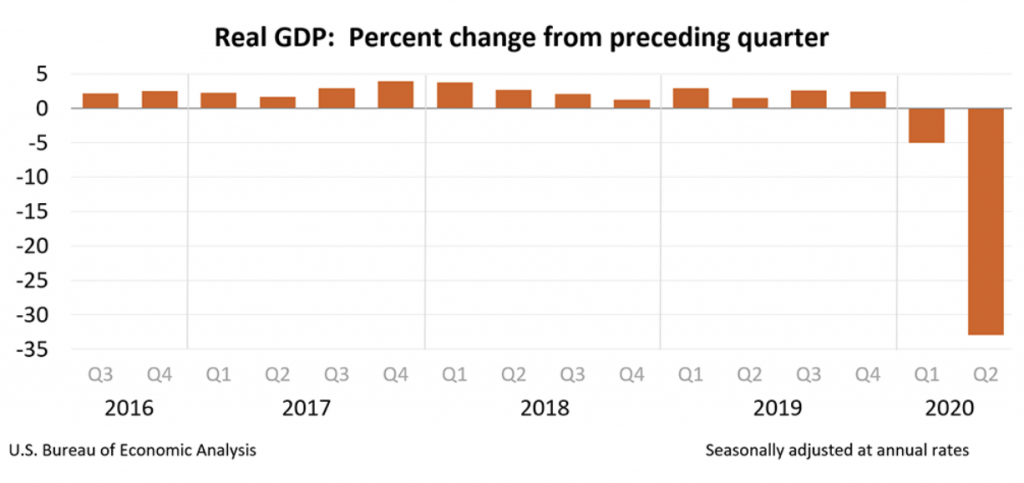

The American economy experienced the sharpest contraction on record in Q2 of 2020. GDP plunged by 33% last quarter, after a 5% decline in Q1.

Taken together, Q1 and Q2 in 2020 officially equate to an economic “recession”—typically defined as two consecutive quarters of negative growth in GDP. This is the first recession in the United States since the Great Recession (December 2007 to June 2009).

During periods of economic contraction, business profitability tends to suffer, which leads to job cuts. The resulting economic environment is characterized by rising loan defaults—whether they be business loans or mortgages paid by consumers.

So far, the economic contraction playing out in 2020 has been like a “ghost” recession—applying crippling pressure for some, while hovering menacingly in the background for others.

A huge question facing the country at this moment is whether the ghost will ever fully materialize, or if it will simply fade away.

Aggressive intervention by the U.S. government in the early stages of the coronavirus pandemic helped slow the negative impacts of coronavirus-related shutdowns on the economy. But that could all change if Congress doesn’t return from recess after Labor Day and finalize another stimulus package aimed at helping struggling businesses and unemployed workers.

The current unemployment rate is above 10%, which means that consumer loan defaults could start rising more rapidly in Q3 and Q4, especially if the extra $600-per-week federal unemployment insurance benefit isn’t reinstated soon.

It’s estimated that 25 million Americans lost those special benefits when they expired on July 25. And because Congress went on summer break starting Aug. 13, negotiations can’t continue until the nation’s top legislators return to work on Sept. 8.

President Donald Trump attempted to provide unemployed workers with a stopgap solution by signing four executive orders on Aug. 8. However, the legality of those orders isn’t completely certain, and the effect has been limited. Fourteen days after the orders were signed, only one state (Arizona) had started sending the extra $300-per-week benefit ordered by the President.

Without additional intervention by the government in the near future, it’s difficult to see how the economy won’t fall deeper into the abyss. There are reportedly 14 million more Americans looking for jobs at this time than there are job openings.

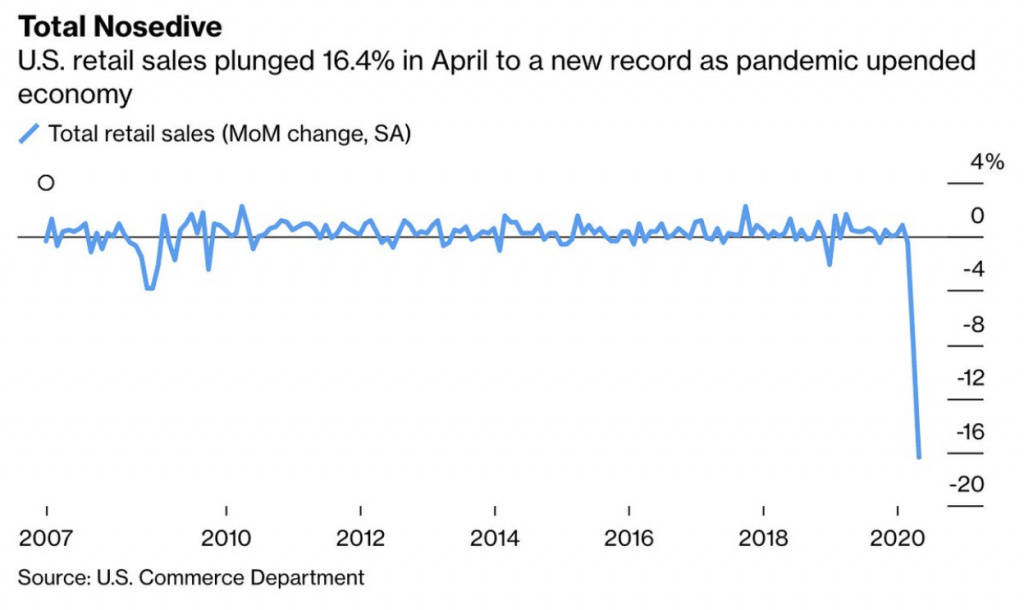

Moreover, a tepid rise in retail sales (1.2%) during the month of July revealed that consumer sentiment is once again wavering. Retail sales were down 8.3% in March, and then a record 16.4% in April, before bouncing significantly in May and June.

But the relatively meek growth in July shows that consumer confidence may be losing steam.

With the $600 in extra unemployment insurance off the table in August, the retail sales numbers for the current month will be anxiously anticipated when they are released in mid-September. Those figures will provide important insight into the strength of the economy without the $600-per-week supplement pulsing through it.

Another big reveal, as it relates to the health of the economy, will occur in mid-October. That’s when banks and other financial institutions will release their Q3 earnings reports. While revenues and profits will make the headlines, only slightly behind in importance will be updates on loan loss provisions.

When financial institutions expect a rash of loan defaults, one of the first actions they take is to inflate loan loss provisions. In accounting parlance that means the banks set aside extra capital to cover expected funding deficits represented by bad loans. If loan loss provisions grow significantly again in Q3, that would be a huge red flag, and a possible indicator that the recession is intensifying.

Going back to the year 1900, the average recession in the United States has lasted about 15 months. The recession immediately preceding this one, the Great Recession, went on for 18 months.

With the 2020 recession officially starting in February it’s reasonable to think it could be over by May of 2021—but only if it’s an “average” recession. With unemployment reaching higher levels in 2020 than in 2008-2009 it’s entirely possible the current recession could last longer than average, or longer even than the 2007-2009 recession.

The unemployment and retail sales figures released in early September, as well as bank earnings in mid-October, will provide more insight into which type of recession the country is currently facing.

If those numbers aren’t good, and no further stimulus measures are adopted by Congress, the ghost recession will undoubtedly be haunting more Americans by the time Halloween arrives at the end of October. To learn more about how the stock market has behaved during previous recessions, readers can review a past installment of Market Measures on the tastytrade financial network when scheduling allows.

“Sage Anderson” is a pseudonym for a contributor who has traded equity derivatives and managed volatility-based portfolios as a prop trading firm employee. He is not an employee of Luckbox, tastytrade or any affiliated company. Readers may direct questions about this blog post, or any other trading-related subject, to support@luckboxmagazine.com.