Mortgage Rates Just Topped 5%. What You Need to Know

The rate for a 30-year fixed mortgage in the United States just spiked above 5% for the first time since 2018, and that could have a big impact on the U.S. housing market.

The number of big stories playing out in the financial markets during 2022 is somewhat mind-boggling. There’s the war in Ukraine, the ongoing COVID-19 pandemic, record levels of inflation and the potential for a near-term recession.

And as of April 2022, it appears that another narrative has been added to the list—skyrocketing mortgage rates. As of early April, the average survey rate on a 30-year fixed mortgage spiked above 5% for the first time since 2018.

What’s even more surprising about that development is that at the start of 2022, the rate was roughly 2.8%.

Rising mortgage rates can be like kryptonite for the housing market, and that could be the case this time around, too. Due to the increase in rates, potential homebuyers will now need to fork over hundreds more per month on a 30-year fixed mortgage as compared to just a few months ago.

The reason for the sudden change in interest rates ties back directly to the more “hawkish” approach adopted by the U.S. Federal Reserve in 2022.

Last year, the Fed announced it would be raising benchmark interest rates in 2022 to fight a rapid increase in inflation. As most are aware, the American central bank dropped benchmark interest rates (known as the federal funds rate) in the United States to effectively 0% during the early stages of the COVID-19 pandemic to help stimulate the economy.

With the worst of the pandemic seemingly over, the Fed is now in the process of normalizing interest rates back to the levels observed pre-pandemic. And increases in benchmark rates have a direct impact on the market for things like car loans and home mortgages.

The big unknown is how this will ultimately impact the housing market.

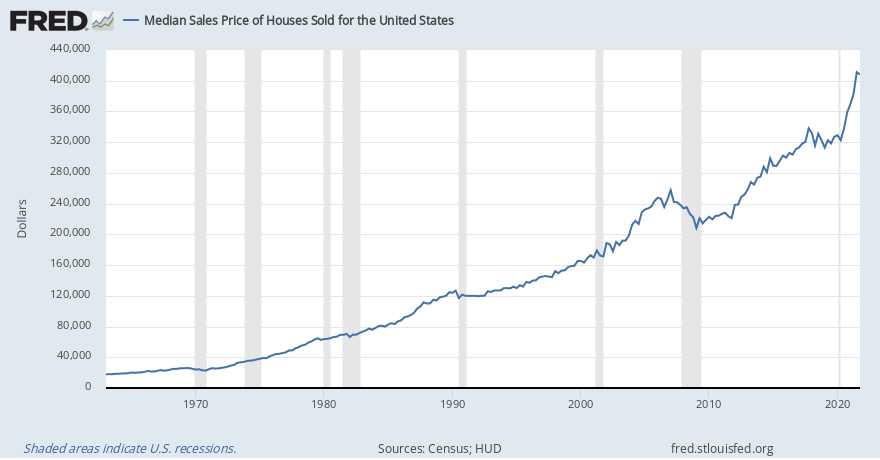

The average price of a home in the United States has risen dramatically during the last two years. Since the start of 2020, the median sale price for a home in the U.S. has risen from roughly $320,000 to $390,000. That’s obviously affected the affordability of homes throughout the country, and rising mortgage rates will likely exacerbate that problem.

Together, these two challenges (rising home prices and mortgage rates) will undoubtedly serve to cool off the overall housing market—but to what degree is unknown.

Readers seeking to track and trade the changing rates environment may want to keep a closer eye on U.S. yields going forward. Yields effectively represent the amount of interest that the U.S. government pays on its debt obligations, and they are highly correlated to benchmark interest rates.

Case in point, the U.S. 10-year Treasury yield dropped to its lowest level in history during the early stages of the pandemic—0.54%—when the U.S. Federal Reserve dropped benchmark interest rates to zero.

Since hitting that all-time low in March of 2020, the U.S.10-year Treasury yield has steadily increased. At the start of 2022, the yield on the 10-year Treasury was about 1.5%. Just three months later, it’s now trading at 2.67%.

The yield on the 10-year Treasury has been increasing in tandem with rising mortgage rates, as both are effectively tied to benchmark interest rates.

Investors and traders can directly trade the U.S. 10-year yield via the Small 10-Year U.S. Treasury Yield (S10Y) futures offered by the Small Exchange.

To learn more about trading interest rates using Treasury Yield futures offered by the Small Exchange, readers are encouraged to review the following episodes of Small Stakes on the tastytrade financial network:

- Small Stakes: Introducing the Small Treasury Yield (S10Y)

- Small Stakes: How to Trade Interest Rate Futures

For updates on everything moving the markets, readers can also tune into TASTYTRADE LIVE, weekdays from 7 a.m. to 4 p.m. CT, at their convenience.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.