Stronger Dollar a Theme in 2022?

As the Issue with Inflation gets ready to drop (11/30) next week, the Luckbox team is putting together its annual Issue with Predictions to follow up. One question will be, "What lies ahead for the U.S. Dollar?"

The dollar has strengthened in value of late—as evidenced by a rally in the U.S. dollar index (DXY)—but that strength has yet to materialize in the USD/RMB exchange rate.

The U.S. dollar took a hit during the COVID-19 pandemic, as central bank easing and a variety of government stimulus programs flooded the financial markets with greenbacks.

But as those programs have tapered off in recent months, the dollar has rebounded. The U.S. dollar index (aka the “DXY”)—which measures the value of the dollar relative to a basket of six foreign currencies—has rallied about 8% since May.

Recently, strength in the dollar has been attributed to an expectation that the U.S. Federal Reserve will get more hawkish in the coming months. In the short term, that means the Fed is expected to start gradually dialing back its assistance to the economy—a process commonly referred to as tapering.

But in the longer run, it’s also expected that the Federal Reserve will not only remove pandemic assistance to the economy, but also start normalizing benchmark interest rates. Currently, projections suggest the Fed will increase the benchmark federal funds rate one or two times in 2022, taking the rate from its current level of zero, up to 0.25-0.50%.

A tightening of monetary policy is generally viewed as bullish for the dollar, because higher yields attract more investors (domestic and international) into U.S. bonds and other rate-sensitive products. For international investors, that process requires the conversion of local currency into dollars, which in effect increases demand for the dollar—thus pushing up its value.

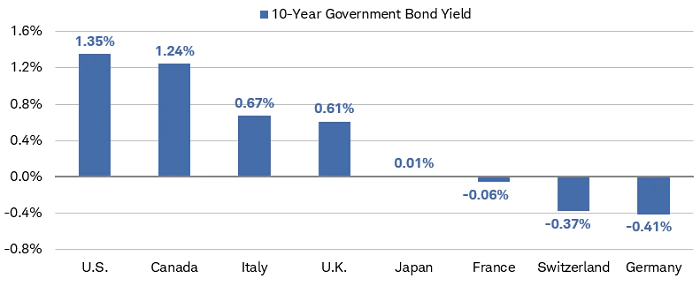

As illustrated below, U.S. yields are already relatively more attractive than yields in many other parts of the world. That suggests any marginal increase in U.S. yields, absent reciprocal increases by other central banks, could catalyze a strong push toward the dollar and dollar-denominated bonds.

Source: advisoryservices.schwab.com

Interestingly, however, not all metrics suggest the dollar is increasing in value.

As many are aware, the value of the U.S. dollar is always quoted relative to something else. The aforementioned U.S. dollar index (DXY) is calculated using the exchange rates of six major world currencies, including the euro (EUR), Japanese yen (JPY), Canadian dollar (CAD), British pound (GBP), Swedish krona (SEK) and Swiss franc (CHF).

But due to the weighting of the index, the primary driver of the U.S. dollar index tends to be the relationship between the dollar and the euro. The euro accounts for nearly 58% of the U.S. dollar index, while the currency with the second-highest weight—the Japanese yen—only constitutes 14% of the index.

That reality indicates that movement in the euro/dollar exchange rate is the biggest driver of the U.S. dollar index. And indeed, the euro has been steadily losing value against the dollar in recent months, which in turn has pushed the DXY lower.

Since May of 2021, the EUR/USD exchange rate has dropped about 8%, from roughly 1.22 to 1.12. That’s basically the same amount the U.S. dollar index has rallied during the same period.

Currently, Europe is grappling with a surge of COVID-19 cases. As a result, economic lockdowns have appeared across Europe, which has pushed down economic forecasts for the Eurozone during Q4 2020 and Q1 2022.

That situation is a big factor weighing on the value of the euro, relative to the dollar. The fact that the U.S. Federal Reserve is planning to tighten monetary policy, while the European central bank is expected to maintain its current accommodative stance—another factor that’s likely contributing to strength in the dollar vis-a-vis the euro.

But when analyzing the relationship in the U.S. dollar relative to the Chinese yuan (aka Renminbi or RMB), the “strong dollar” narrative doesn’t appear as convincing.

Last year, when the U.S. dollar weakened during the onset of the pandemic, the dollar lost considerable value relative to the Chinese yuan. But during the dollar’s recent rally against the euro, it hasn’t managed to claw back any appreciation against the yuan. It’s actually given up more ground in recent weeks.

Prior to the onset of the COVID-19 pandemic, the USD/RMB exchange rate was about 7—meaning one US dollar could be exchanged for roughly 7 RMB.

But starting back in May of 2020, the dollar started to steadily depreciate against the RMB, and it is now trading for about 6.38. That’s only slightly above the five-year low, which was 6.27.

So why does the EUR/USD exchange rate tell one story, while the USD/RMB exchange rate tells another?

The answer isn’t easy to come by. Certainly, Chinese exports—the heart and soul of the economy—have remained strong throughout the pandemic, and even increased lately.

But the Chinese economy itself has faltered in recent months, and is exhibiting slower growth as compared to its normal high octane quarterly churn. Moreover, China has also been grappling with a credit implosion in its real estate sector. Those are the types of challenges that would normally serve as an anchor for the Chinese currency.

But China has also opened its economy to increased foreign investment this year, and that might be a reason for steady demand in the yuan, relative to the dollar. It might also stem from domestic borrowers (in China) taking advantage of the weak dollar and strong yuan to repay dollar debt.

Or, it’s even possible that the Chinese are manipulating the exchange rate in their favor. But that doesn’t match previous policy in the Middle Kingdom, because leaders in China usually prefer a weak yuan—making China-made products relatively more attractive in the export market.

Regardless of the reason, this divergence probably won’t last much longer. Either the DXY will reverse course, or the dollar will start to gain ground against the yuan. And based on hawkish posturing by the U.S. Federal Reserve, it’s more likely to be the latter.

To learn more about recent strength in the U.S. dollar, readers are encouraged to review a new installment of Options Jive on the tastytrade financial network. And to get started trading foreign currencies, this link should also prove helpful.

For more on the U.S. Dollar and other 2022 forecasts, subscribe to Luckbox for free at getluckbox.com.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.