Trading Metals Amidst a Looming Recession

During previous economic contractions, gold has been a relatively safe place to park capital, which is why investors and traders may want to give this niche of the financial markets a closer look in 2022.

Amidst the rise of emerging digital assets such as cryptocurrencies and non-fungible tokens (NFTs), the precious metals sector of the financial markets has been subject to some serious reputational damage in recent years.

For example, crypto enthusiasts have argued that digital coins are stealing market share from gold as a store of value, and that the crypto sector will one day replace precious metals as a top safe haven in the financial markets.

While that may one day come to pass, recent market activity indicates that paradigm shift has yet to occur. During the recent bout of market turbulence, which has seen the major U.S. market indices correct by more than 20%, Bitcoin’s value has dropped by roughly 57%, while the price of gold is only down 17%.

Considering those respective performance figures, it’s safe to say that owners of gold in 2022 are feeling a lot happier than owners of bitcoin.

Gold’s performance this year—holding its value better than many stocks and cryptocurrencies—is par for the course, from a historical perspective. Market data from the last 70+ years demonstrates that gold prices generally hold up well during periods of economic uncertainty.

That was certainly the case amidst the two most recent recessions in the United States—during 2008-2009 and 2020.

For example, when the COVID-19 pandemic first took hold in the U.S, gold prices actually soared to their highest-ever absolute levels—trading up to an all-time high of $2,074.88/ounce on August 7 of 2020.

The precious metals sector responded in a similar fashion during the Great Recession, when gold rallied from a price of roughly $750/ounce in October of 2008, all the way up to $1,800 in August 2011—a jump of 140% in under three years.

Today, gold is trading at about $1,700/ounce, having dropped about 17% since March.

Gold Performance During Other Recessions

Looking back further in history, market data shows that gold’s relative outperformance during past recessions or depressions isn’t just a recent trend.

During the only other major recession of the 21st century—in 2001—gold prices also outperformed. Starting in March of 2001, gold prices rallied from roughly $430/ounce, all the way up to $650/ounce, as of late 2003.

Prior to the 21st century, gold also exhibited relatively attractive performance during economic contractions in the U.S. And while the returns in precious metals weren’t always in the double digits, gold prices have at least historically held their value during periods of economic recession or depression—suggesting that as a store of value, gold has been a solid performer for many years.

The list below highlights some of the most severe economic recessions observed in the U.S. during the second half of the 20th century, and gold’s associated performance during those periods:

- 1973 Recession, Gold +87%

- 1981 Recession, Gold +2%

- 1990 Recession, Gold +0%

With gold tumbling by 17% since March of this year, a natural follow-up question might be: Why has gold been losing value lately, especially with the threat of a recession looming?

The answer to that question ties back to another integral component of gold’s relationship with the financial markets, particularly the U.S. dollar.

Gold’s Relationship with the U.S. Dollar

One headwind for gold this year has been a massive surge in the value of the U.S. dollar.

In the U.S., gold is priced in U.S. dollars, which means fluctuations in the value of the dollar, especially large fluctuations, can affect the price of gold.

As a general rule, when the value of the dollar increases relative to other currencies worldwide, the price of gold tends to fall in U.S. dollar terms. And in 2022, the value of the dollar has roared higher against many of the world’s other fiat currencies, which helps explain at least a portion of the pullback in gold.

The U.S. dollar has been so strong this year that it’s trading at some jaw-dropping levels against some of the world’s other major currency heavyweights. For example, the exchange rate between the dollar and the euro recently dropped to parity—meaning they can now be exchanged 1-for-1.

The last time the euro was so weak against the dollar, the year was 2002. The dollar has been strong against the Japanese yen and the British pound, too.

On July 14, the Japanese yen dropped to a 24-year low against the dollar, when the USD/JPY exchange rate hit 139. That means it takes ¥139 to purchase a single dollar, whereas, at the start of the year, only ¥115 was required to purchase a dollar.

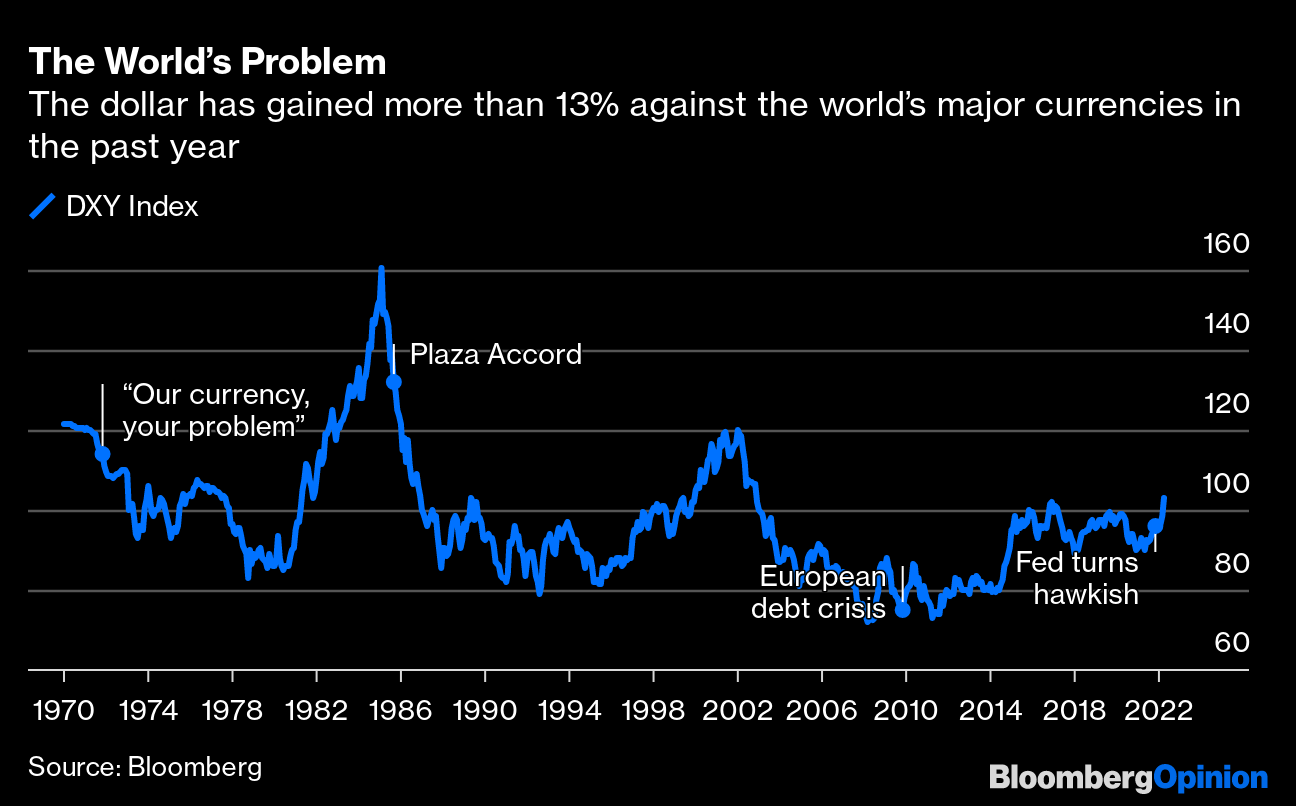

The U.S. Dollar Index (DX-Y.NYB), also known as the DXY, is one of the most followed gauges of the dollar’s ongoing value, in basket terms. The DXY measures the value of the U.S. dollar relative to a group of currencies that essentially constitute the country’s closest trading partners—the euro, Japanese yen, British pound, Canadian dollar, Swedish krona and Swiss franc.

In 2022, the dollar is up 13% versus its DXY peers, and that figure is even more interesting when one considers that gold has dropped by about 17% so far this year.

The aforementioned figures help illustrate that gold’s recent decline may have more to do with dollar strength than it does with gold weakness.

With a recession looming, it’s difficult to envision the bottom falling out of gold prices anytime soon—especially considering gold’s relative strength during past economic recessions.

For these reasons, investors and traders should keep an eye on the precious metals market, as there may be an opportunity to capitalize on the recent pullback—whether that be via a long directional position, or an options/volatility position.

For more background on the gold trade, check out this past installment of Market Measures on the tastytrade financial network. For more context on the U.S. dollar’s surge in 2022, watch this episode of Small Stakes.

To follow everything moving the financial markets, tune into TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.