New 200% Aluminum Tariff Designed to Punish Russia

Trading volumes surged in the aluminum futures market after the U.S. unveiled fresh tariffs on Russian aluminum exports

On Feb. 24, the Biden administration sent shockwaves through the global commodities market when it announced massive new tariffs on aluminum imports coming into the United States from Russia.

The new import tariffs are set at 200% and will be applied starting March 10.

Prior to that announcement, the tariff on aluminum imports from Russia was 10%—a level enacted by the previous administration. The new tariffs serve as a wake up call for the industry because they affect other countries involved in the aluminum supply chain beyond Russia.

For example, the new duties apply to any and all aluminum originally smelted in Russia, which means even intermediary countries that export Russian-sourced aluminum to the U.S. will be hit with the 200% tariff.

The tariffs on Russian aluminum imports will be officially enacted on March 10, while the secondary tariffs on Russian-sourced aluminum from intermediary countries go into effect on April 10.

The new duties are being positioned as fresh economic sanctions, with the intent of punishing the Russian government for its continued assault on Ukraine. An international coalition of countries has already attempted to cap the price at which Russia can sell its oil in the international market.

In many regards, the new aluminum tariffs represent a boycott, because they make Russian-sourced aluminum prohibitively expensive in the U.S. market. A 200% tariff means importers of Russian aluminum will need to pay twice the value of the goods imported.

So, an American importer purchasing $100,000 worth of Russian aluminum would need to pay $300,000 in total, with $200,000 of that going toward the tariffs.

Aluminum exports from Russia to the U.S. increased last year despite the onset of war in Eastern Europe, and the Biden administration is no doubt looking to reverse that trend—or wipe it out completely.

Trade-related diplomacy can be a powerful tool because it effectively creates a new set of winners and losers. In this case, Russia undoubtedly loses. And because China is the world’s largest producer of aluminum, there’s reason to believe that the Chinese domestic aluminum sector will be one of the winners.

China is the world’s largest player in the global aluminum market, producing nearly 36 million tons on an annual basis. After that, it’s India and Russia—both producing about 3.7 million tons annually.

The U.S. produces about 1.1 million tons of aluminum each year, but consumes as much as 5 million tons, which means U.S. businesses rely heavily on the export market to meet their annual supply requirements.

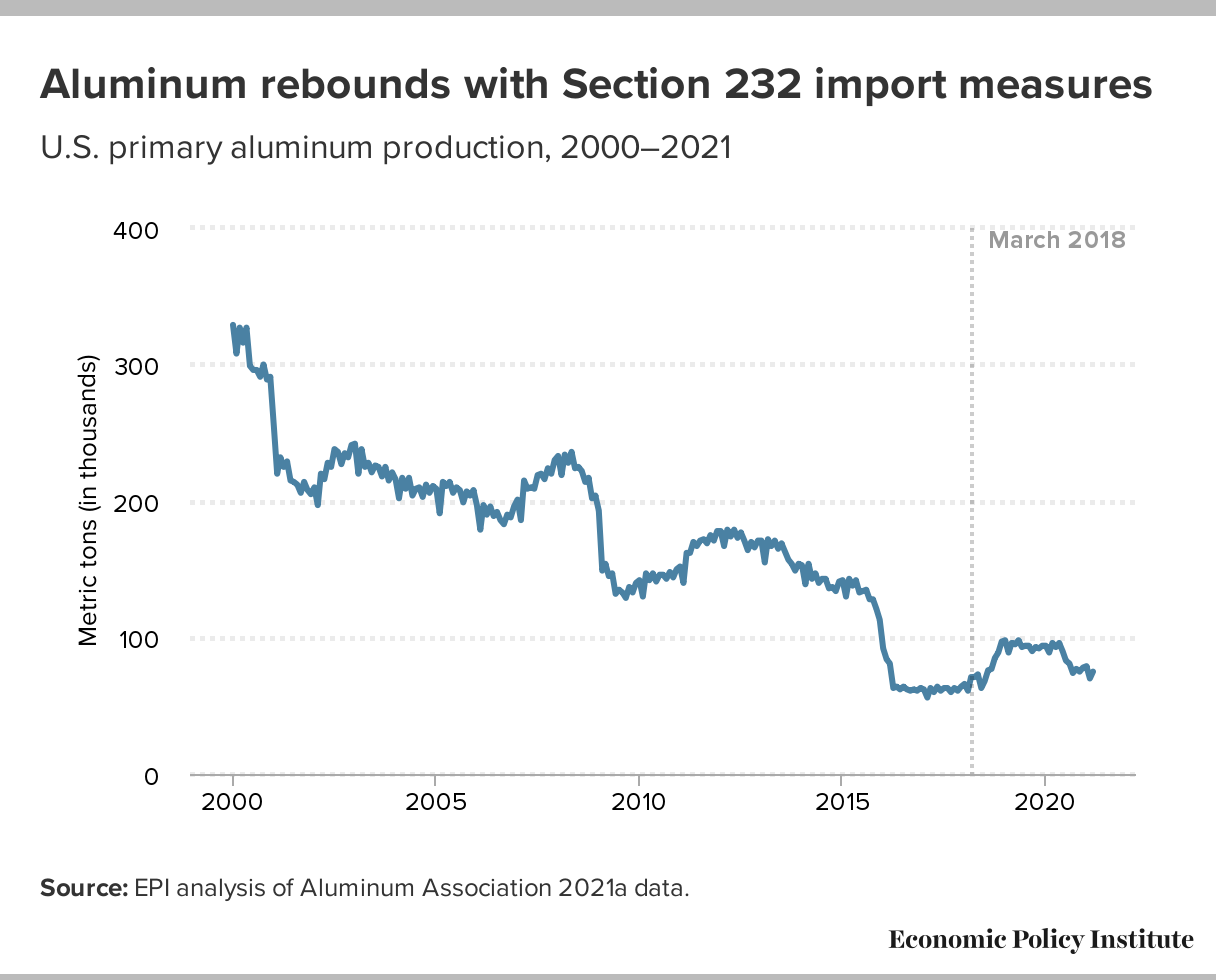

After the original aluminum tariffs were enacted against Russia back in 2018, the U.S. saw an increase in domestically-produced aluminum. But the bump in production was only temporary due to the onset of the COVID-19 pandemic (illustrated below).

The fact that American production of aluminum increased back in 2018 when the 10% tariff was first applied suggests that the American aluminum sector could benefit this time around.

That possibility was underscored by the American Primary Aluminum Association (APAA)—a key industry association for aluminum products—which voiced its strong support for the new import duties.

In a statement released by the APAA, the organization said of the new tariffs, “The APAA, its members, and its workers stand with the Biden administration in support of its decision to robustly defend the U.S. aluminum industry in the face of continued Russian aggression and blatant disregard for international economic and security norms.”

Trading the aluminum sector

In the wake of the tariff announcement, an avalanche of fresh trading volume swept through the U.S. aluminum futures market, as major players repositioned their pieces on the board.

The Chicago Mercantile Exchange (CME) announced in early March that the aluminum futures market set a new record for average daily volume in the month of February.

Last month, the average daily trading volume was roughly 3,100 contracts, which was three times higher than the year prior. The CME also reported that total open interest in the aluminum futures market has crested toward record highs, as illustrated below.

Source: CMEGroup.com

Aluminum prices did move higher in the wake of the tariff announcement, but modestly.

That’s likely because of concerns over the strength of the global economy, which have served as a headwind in the commodities market. Similar to copper, aluminum prices have traditionally exhibited a strong correlation with the underlying economy.

As a result of this link, it’s possible the Biden administration held back on rolling out the aluminum tariffs in 2022—to avoid an unwanted spike in prices amid record inflation. However, with global manufacturing activity slowing in recent months, demand for aluminum has softened. That means the impact of the tariffs is theoretically reduced, from a market standpoint.

Aluminum prices are up roughly 3% since the tariffs were announced on Feb. 24. But two key American aluminum producers—Alcoa (AA) and Century Aluminum (CENX)—have seen their shares rally considerably more over the same period.

Alcoa, for example, has rallied by roughly 19% since the date of the tariff announcement, while Century Aluminum has seen its shares spike by nearly 30%. Considering those gains, it’s clear that market sentiment has shifted in favor of American producers.

Worldwide, some of the largest companies in the aluminum sector include Chalco (China), Hongqiao (China), Rusal (Russia), Xinfa (China), Rio Tinto Alcan (Australia), Alcoa (United States), Emirates Global Aluminum (UAE) and Norsk Hydro (Norway).

Of those, only Alcoa (AA), Norsk Hydro (NHYDY) and Rio Tinto (RIO) are listed on American exchanges. The only pure-play aluminum ETF in the market is the Global X Aluminum ETF (ALUM).

To track and trade the aluminum sector, investor and traders can add the following symbols to their watchlists:

- Alcoa (AA)

- Arconic (ARNC)

- Century Aluminum (CENX)

- Constellium (CSTM)

- Global X Aluminum ETF (ALUM)

- Kaiser Aluminum (KALU)

- Reliance Steel and Aluminum (RS)

- Rio Tinto (RIO)

- Vedanta (VEDL)

To follow everything moving the markets—including global commodities markets—monitor tastylive, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastylive or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.