New Market Math: New Highs + Sustained Volatility = Short Calls

The 2020 trading year has been unusual, and it’s arguably getting weirder.

For most, the weirdness of 2020 has been illustrated through stock market indexes making all-time highs, set against the backdrop of a besieged economy plagued by record levels of unemployment.

But bullish trends in U.S. stock indexes (S&P 500, Nasdaq 100, Russell 2000) don’t tell the full story. There’s plenty of weirdness lurking behind the numbers.

Typically, all-time highs in the stock market are coupled with corresponding lows in market volatility (i.e. low VIX). After all, the S&P 500 and VIX are known to share a strong, negative correlation—when one goes up, the other goes down, and vice versa.

However, this summer, bullish behavior in the indexes has been accompanied by stubbornly high volatility.

Consider for a moment the following: When the S&P 500 set its all-time high earlier in 2020 (February), the VIX was trading around 14.

These days, with the S&P 500 once again charging back toward all-time highs, the VIX is trading around 24—well above its historical average of 18-19, and well above the 14-level observed in February.

What’s especially interesting about the current dynamic is that it opens up a new angle on trading the financial markets, particularly as it relates to options and volatility.

For example, when equity markets have made all-time highs in the past, associated levels of implied volatility have been low. That means short options trades weren’t necessarily attractive because short volatility typically gathers the most interest when implied volatility is relatively high.

This time around, the S&P 500 is once again closing in on its all-time high, but the VIX is trading well above its average, making potential short options approaches relatively more attractive.

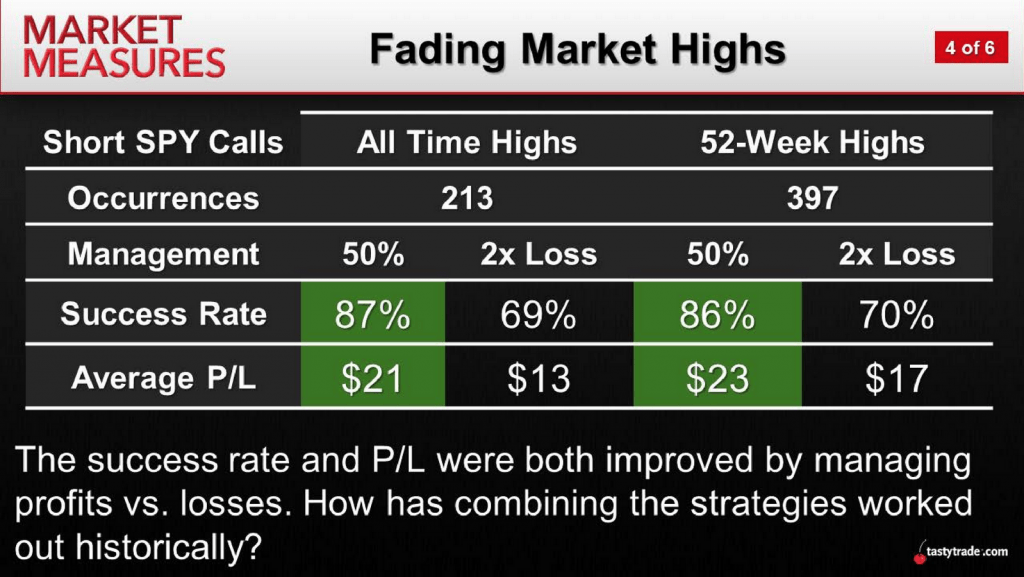

According to research conducted by tastytrade, short calls have historically performed well when indexes are setting all-time—or 52-week—highs. Tastytrade has conducted several studies on this topic, but one in particular is worth highlighting at this time.

Examining the historical performance of short calls at market highs, researchers at tastytrade designed a series of back tests using the following parameters:

- Underlying symbol studied: SPY

- Time period: 2005 to 2019

- Strategy: Short 30 delta calls

- Comparison: All-time highs vs 52-week highs

- Trade management filters:

- 50% of max profit

- Managed losses at 2x credit received

- Held through expiration (i.e. no management, control group)

The market study’s results are compiled in the graphic below.

As one can see, using all-time highs and 52-week highs as trading signals for selling calls has historically demonstrated attractive success rates. As it relates to the trade management approaches used in conjunction with this trading strategy, the back tests further revealed that the “50% of max profit” was the most optimal.

Readers seeking more information on this topic may want to review this previous episode of Market Measures when timing allows.

Because short calls are usually deployed as “covered calls,” as opposed to naked short options, a previous episode of Tasty Extras titled “The Mechanics of Covered Calls” is also recommended.

“Sage Anderson” is a pseudonym for a contributor who has traded equity derivatives and managed volatility-based portfolios as a prop trading firm employee. He is not an employee of Luckbox, tastytrade or any affiliated company. Readers may direct questions about this blog post, or any other trading-related subject, to support@luckboxmagazine.com.