Mining the Future: Uranium’s Role in the AI Age

Despite the pullback in uranium prices, uranium stocks continue to soar

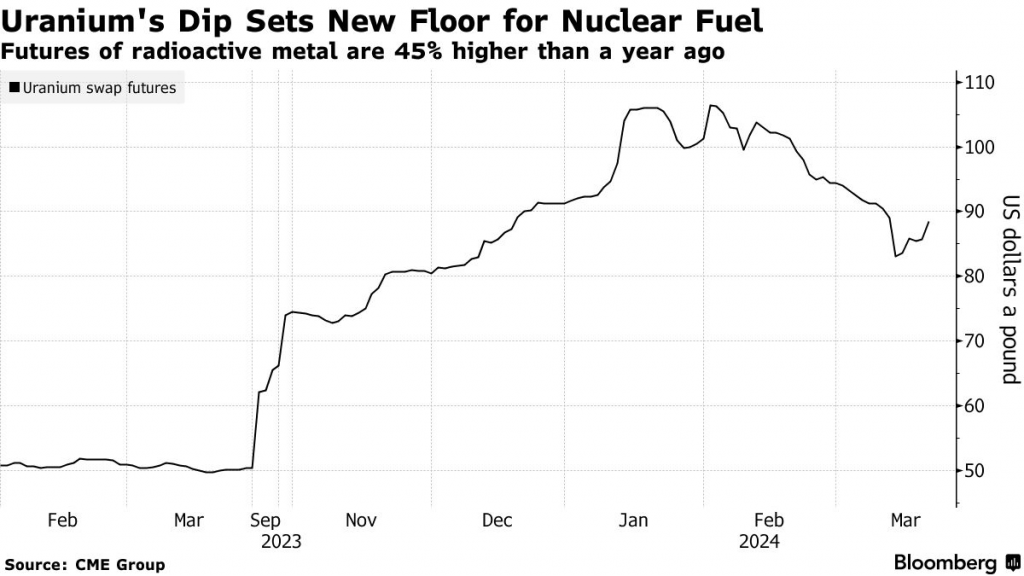

- Following a sharp rally in 2023, uranium prices have cooled slightly in 2024, stabilizing at around $86 per pound.

- Despite the pullback in prices, many uranium mining companies, including Cameco (CCJ), one of the world’s largest miners, have continued to see their shares rise.

- Renewed interest in the potential of small modular reactors (SMRs), which promise greater efficiency and adaptability, has also driven increased interest and investment in the uranium and nuclear sectors this year.

The AI revolution has created some unlikely heroes, and one of them has been uranium miners. This group has benefited from renewed interest in nuclear power, driven by the surging electricity requirements of AI-focused data centers. The immense computational power needed for AI applications has significantly increased the demand for reliable and consistent energy sources, making nuclear power an attractive option.

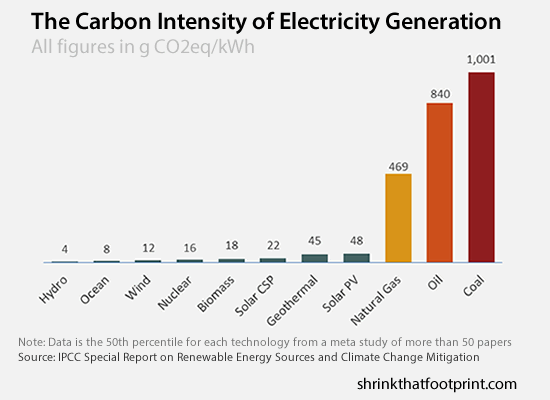

However, the nuclear energy sector, including uranium producers, is also benefiting from another tailwind. The carbon emissions from nuclear plants are minimal, making this energy source an appealing supplement to renewable energy. This is especially important in the context of aggressive global carbon reduction targets. As countries strive to meet their environmental commitments, nuclear energy offers a stable, low-carbon alternative that complements renewable sources like wind and solar.

Together, these trends have put nuclear power back into the spotlight after many years of relative obscurity. And the dual appeal of supporting the AI-driven energy demand surge while contributing to carbon reduction goals has undoubtedly revitalized the nuclear sector. As a result, uranium miners have seen increased interest in the capital markets, positioning them as important players in the evolving energy landscape.

Carbon-free energy goals benefit the nuclear/uranium sectors

Governments around the world have been working to adopt renewable energy to help reduce the amount of carbon entering the atmosphere.

While solar and wind have been popular methods, there’s also been a renewed push to use nuclear energy, and the United States is spearheading a global pledge to triple the world’s nuclear capacity by 2050.

For its part, the U.S. aims to generate 100% of its electricity from carbon-free sources by 2035. To achieve that goal, the country must build and operate new nuclear power plants.

Ideally, these would be fusion-powered plants because they theoretically produce no waste. However, fusion is not expected to be commercially viable for at least another five to 10 years. In the meantime, the country will need to increase its reliance on fission-powered nuclear plants, which already provide a reliable and low-carbon energy solution.

Fission is created by splitting the nuclei of heavy atoms, such as uranium or plutonium, which triggers the release of immense amounts of energy. Nuclear fission has been used commercially to generate electricity since the 1950s, starting with the commissioning of the first commercial nuclear power plant in Obninsk, Russia in 1954.

The U.S. generates 19% of its electricity with nuclear power. At present, 92 nuclear facilities are operating in the nation. The two most recent additions are Vogtle Unit 3 and Vogtle Unit 4, which came online in July 2023 and April 2024, respectively.

Considering the importance of uranium in fusion, it’s no surprise recent pledges to increase the world’s nuclear capacity have carried over into the uranium market. Since the start of 2020, uranium prices have climbed from $25 per pound to $86 per pound, an increase of roughly 240%.

The year 2023 was a pivotal year for uranium prices. They surged from $48 per pound to over $100 per pound, marking a 16-year high. Since then, prices have moderated.

The recent upward trend in prices has been for miners of uranium. And despite the recent downturn in prices, uranium-focused stocks continue to rally in 2024. One of the largest and best-known uranium miners in the world, Cameco (CCJ), has seen its stock rally by nearly 30% in 2024.

Year-to-date performance in some of the other well-known uranium stocks and ETFs is highlighted below:

- Denison Mines (DNN) +32%

- Cameco (CCJ) +28%

- Fission Uranium (FCUUF) +23%

- VanEck Uranium+Nuclear Energy ETF (NLR) +19%

- Global X Uranium ETF (URA) +14%

- Isonergy (ISENF) +14%

- Sprott Junior Uranium Miners ETF (URNJ) +13%

- NexGen Energy (NXE) +10%

- Sprott Uranium Miners ETF (URNM) +10%

- Uranium Energy (UEC) 0%

- Sprott Physical Uranium Trust (SRUUF) -2%

- Ur-Energy (URG) -2%

- Energy Fuels (UUUU) -6%

Supply-side dynamics have been bullish for uranium miners

Currently, the United States mines only a small portion of its own uranium but is actively working to remedy the situation. In the meantime, key allies, such as Australia and Canada, both among the world’s top five uranium producers, play a crucial role in supplying uranium to the U.S.

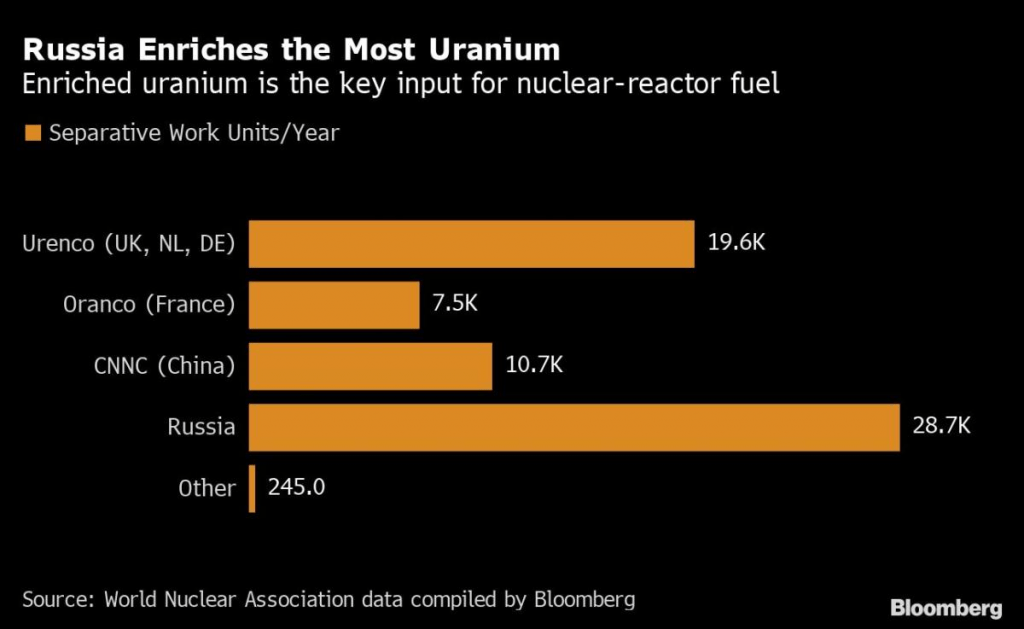

However, many nuclear plants require enriched uranium, which is harder to obtain. A significant challenge for the United States is that the Russian Federation is one of the world’s leading producers of enriched uranium. Russia controls approximately 40% of the global market for enriched uranium, posing a strategic challenge for the U.S. as it seeks to secure reliable and independent sources of this critical material.

The Russo-Ukrainian War has complicated U.S. purchases of Russian uranium. The United States is wary of sending hard currency to Russia, which could be used to support its war against Ukraine.

To address this issue, the United States has been collaborating with allies to enhance their capacity to produce enriched uranium. Four companies dominate this critical market: Rosatom (Russia), CNNC (China), Urenco (a Western consortium) and Orano (France).

Addressing the market, Lindsey Walter—the director of international policy for climate and energy at Third Way—recently told Foreign Policy that “Russia and China dominate the market, and Russia has proven its desire to weaponize energy for geopolitical gain.”

Fortunately, the Russian government hasn’t disrupted Rosatom’s agreements to supply Europe and the United States with enriched uranium. But the uranium market could become vulnerable to intense volatility.

To help remedy the situation, the United Statesn allocated $2.7 billion this year to help develop domestic uranium enrichment capabilities. Moreover, the U.S. is working with its partners in Urenco, which include Germany, the Netherlands and the United Kingdom, to boost output.

Growing interest in small modular reactors (SMRs)

Last but not least, investors should be aware of the small modular reactors (SMRs), which appear to be a key method for expanding the nuclear industry.

SMRs are small-scale fission reactors designed to be more flexible and efficient than traditional reactors. They are typically modular and can be manufactured as a series of smaller, combinable segments instead of one large unit. That modularity is also expected to provide greater scalability, while offering reduced costs and and a superior value proposition.

Excitement over the potential of SMRs has been palpable this year, with one of the standout names in this niche—NuScale (SMR)—rallying by more than 300% year-to-date. That makes it a 2024 top-performer among companies with market capitalizations between $2 billion and $10 billion.

Another company that’s gained attention in this niche is Oklo (OKLO), which recently debuted on the New York Stock Exchange. It’s backed by the CEO of OpenAI, Sam Altman, who also serves as the chairman of Oklo’s board of directors.

As of now, Oklo has no material revenue and no nuclear reactors in operation. But during a May 9 appearance on CNBC, the CEO of Oklo—Jacob DeWitte—indicated the company’s first reactor would come online around 2027. Importantly, the company plans to operate its own facilities, meaning Oklo won’t sell the reactors—at least not initially—and instead plans to generate revenue by selling the energy produced by its reactors.

Notably, the Nuclear Regulatory Commission denied Oklo’s initial application to build an SMR in Idaho. However, the company is reapplying for approval, and expects to activate its SMR in Idaho by 2026 or 2027. For background, Oklo derives its name from a place in the African nation of Gabon, where naturally occurring nuclear fission reactions are believed to have occurred billions of years ago.

Shares of Oklo haven’t performed as well as those of NuScale in 2024. Oklo’s stock has dropped by about 29% this year, compared to NuScale’s impressive return of over 300%. It’s important to note, however, that NuScale shares were down nearly 70% in 2023 before rebounding sharply in 2024. This demonstrates that sentiment can shift quickly, suggesting Oklo could experience a similar turnaround if the company achieves key milestones.

That’s why active investors interested in the nuclear industry should monitor shares of Oklo and NuScale, as well as the leading uranium miners and ETFs. The performance of these securities should provide insight into the future trajectory of the nuclear industry, influencing not only the global energy landscape but also the rapidly advancing AI sector.

Editor’s Note: Some of the stocks covered in this article are small cap and/or over-the-counter (OTC) stocks. Readers should be aware that investing/trading small cap and over-the-counter (OTC) stocks involves unique and potentially significant risk. These stocks are often more volatile and less liquid than their large-cap counterparts, which may result in high-magnitude price fluctuations and/or difficulties in buying or selling shares. Additionally, OTC stocks may have less stringent reporting requirements, resulting in limited publicly available information and higher susceptibility to fraud or manipulation. Investors should therefore conduct thorough research and consider their risk tolerance before investing in (or trading) small cap and OTC stocks.

Andrew Prochnow has more than 15 years of experience trading the global financial markets, including 10 years as a professional options trader. Andrew is a frequent contributor of Luckbox Magazine.

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.