How to Trade the 2024 Surge in Gold and Silver Prices

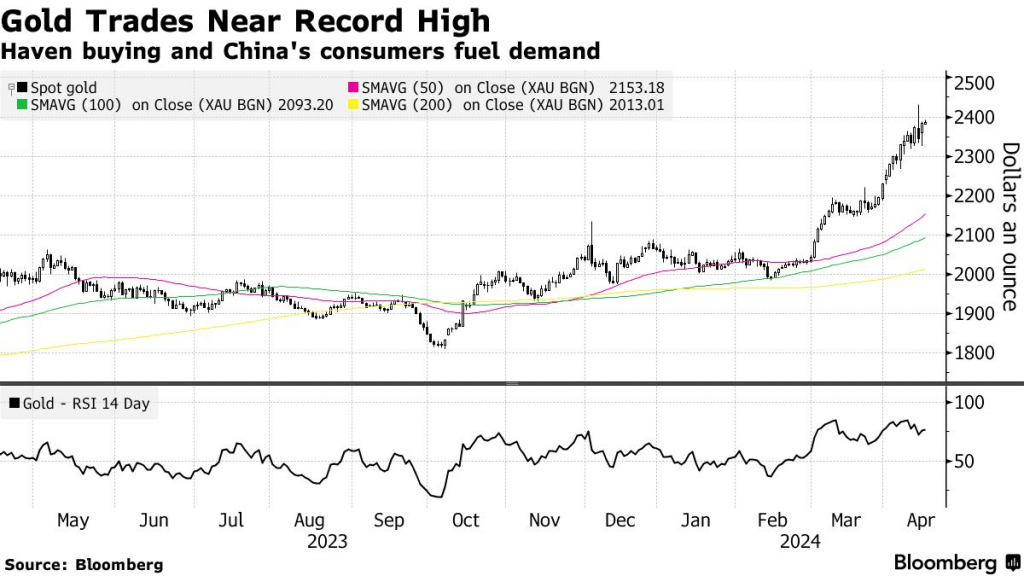

Gold bugs jumping as gold prices surge past $2,400 per ounce

- Gold has rallied by about 18% so far in 2024 and recently broke through $2,400 per ounce for the first time.

- The silver market also has been strong in early 2024, with prices rallying by about 19%. But the current price of $28.50 per ounce remains well below silver’s all-time high of nearly $50 per ounce.

- The gold/silver ratio is currently about 84, which indicates pairs trading opportunities may develop if the ratio continues to rise.

The global financial markets have produced some riveting action thus far in 2024, but one of the biggest surprises might be the rally in the precious metals sector.

Both gold and silver have cruised to significant gains for the year so far, with the former also notching a new all-time high.

Since the start of the year, gold prices are up roughly 18%, while silver is up about 19%. Notably, physical gold has performed better than the gold mining stocks, as forecasted last autumn in this previous Luckbox post.

Thus far in 2024, the SPDR Gold Trust (GLD) has rallied by nearly 16%, while the VanEck Gold Miners ETF (GDX) is up about 8%.

Gold-mining stocks diverge

However, those figures don’t tell the full story. As outlined below, a couple of the key gold miners have seen their shares trade lower this year, despite the strong bull run in physical gold prices. Here are year-to-date returns for selected gold miners:

- Harmony Gold (HMY), +45%

- Gold Fields (GFI), +24%

- Freeport-McMoRan (FCX), +17%

- Agnico Eagle Mines (AEM), +14%

- Alamos Gold (AGI), +14%

- Kinross Gold (KGC), +7%

- Franco-Nevada Corp (FNV), +5%

- Royal Gold (RGLD), +1%

- Newmont Corp (NEM), -7%

- Barrick Gold (GOLD), -8%

As noted above, there’s been a divergence in gold miners’ performance this year. As such, one would have needed to pick the right gold stock to benefit from the rise in prices. That’s why physical gold—or securities linked to it—is arguably the optimal choice, because if gold prices rise, owners of these assets/securities are virtually assured to benefit.

On the other hand, gold mining companies are partly exposed to the underlying price of gold and partly exposed to the general direction of the stock market. The former because they mine and sell gold—thus relying on prevailing prices—and the latter because they are publicly traded stocks.

A company’s success in the stock market often hinges on how well it’s run. In the case of the gold miners, year-to-date stock performance appears to indicate HMY, GFI and FCX were in the best position to benefit from rising prices.

Historically, gold miners have maintained hedges to help offset losses in the event of correction in the gold market. But according to a recent report by The Wall Street Journal, hedges are far less prevalent than they used to be.

It’s easy to see why many gold bugs prefer assets/securities levered more closely to physical gold, to help ensure a bullish gold bet pays off as expected. Because it can be especially painful to watch a gold stock position decline in value amid a strong rally in the underlying price of gold.

Key factors pushing gold prices higher in 2024

Two key factors appear to be pushing gold prices higher: rebounding inflation and strong demand for physical gold in the global marketplace.

In the fourth quarter of last year, most investors and traders expected inflation to continue to tick lower through the first half of 2024 and the Federal Reserve would slowly cut benchmark interest rates to help ensure stability in the underlying economy.

However, things aren’t playing out as some traders expected. In early April, the U.S. government reported inflation rebounded slightly in March. A rebound in inflation is suboptimal for a variety of reasons. At the top of the list, higher inflation could preclude the Fed from lowering benchmark interest rates in the near term.

After the latest inflation report, the interest rate futures market shifted its expectation for the Fed’s first rate cut from the end of Q2 to early Q3. As a result, fresh uncertainty linked to inflation and rate cuts has been supportive of higher prices in the gold market.

Gold is traditionally a “safe haven” asset, which means buying activity often intensifies when uncertainty/fear is amplified in the financial markets.

Updating its outlook on the gold market, Goldman Sachs recently forecast gold prices would end the year trading closer to $2,700/ounce, as compared to its previous target of $2,300/ounce.

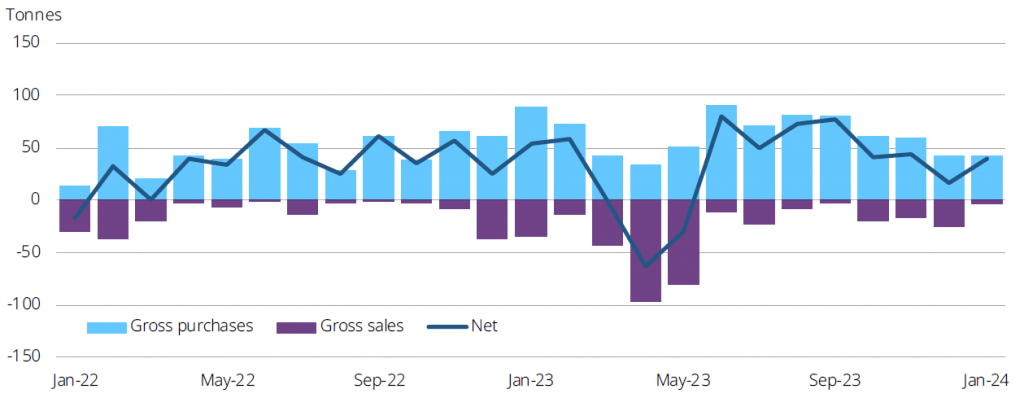

Global central banks continue to hoard gold

Another key dynamic in the 2024 gold market relates to supply and demand, which is always an important consideration in global commodities markets. From this angle, gold prices appear to be benefiting from persistently strong demand from the central banking sector.

Sovereign nations have been building their reserves of gold for some time now, but transaction data from the first month of 2024 revealed a sharp increase in gold purchases as compared to the end of last year.

In December of 2023, global central banks bought 17 net tons of gold. But in January, net purchases were closer to 34 tons—double the December level. As highlighted below, gold sales also shrunk in January, which helps explain why the net purchase amount was so much higher in January.

According to recent reports, six central banks were responsible for the sharp increase in net purchases during January.

At the top of the list was the Central Bank of Turkey, which bought 12 net tons of gold in January. The next largest buyers were the People’s Bank of China (+10 tons), the Reserve Bank of India (+9 tons), the National Bank of Kazakhstan (+6 tons), the Central Bank of Jordan (+3 tons) and the Czech National Bank (+2 tons).

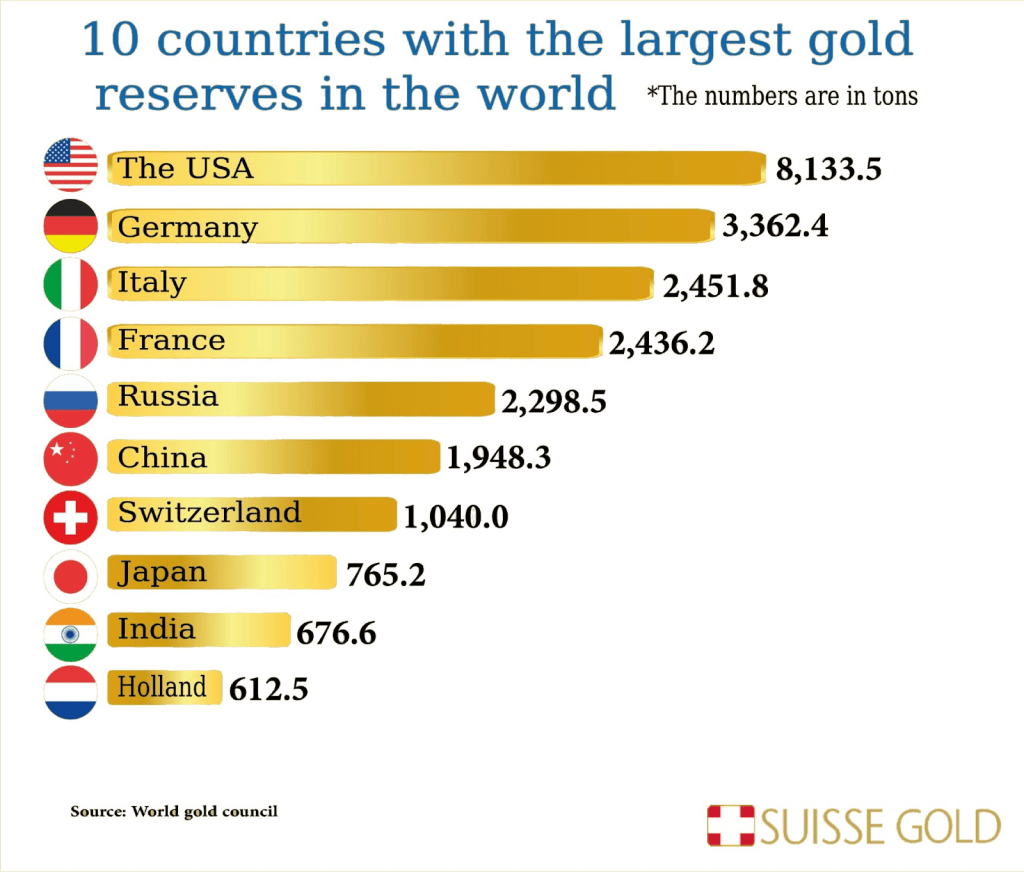

For China, January represented the 15th-consecutive month of net additions to its national gold reserves. As highlighted below, China currently holds the sixth-largest hoard of gold reserves.

Last year, data compiled by Bank of America showed the three largest buyers of gold were China, Poland and Singapore. Last year, China’s central bank is estimated to have bought around 225 net tons of gold. Importantly, sovereign nations aren’t the only consumers of gold. Lately, it appears gold prices are also benefiting from increased buying by private buyers.

In China, for example, increased gold purchases are believed to stem from uncertainty in the domestic real estate market. Along those lines, John Reade—chief market strategist at the World Gold Council—told Bloomberg TV recently, “From the start of the year, we’ve seen enormous Chinese retail buying … record amounts of buying on the domestic Shanghai Gold Exchange.”

Illustrating the positive sentiment in the market, gold prices broke through $2,400 per ounce for the first time in history on April 16. For context, silver prices have also started the year on strong footing but remain well below all-time highs. Silver currently trades at about $28.50/ounce, while the all-time high is closer to $50 per ounce.

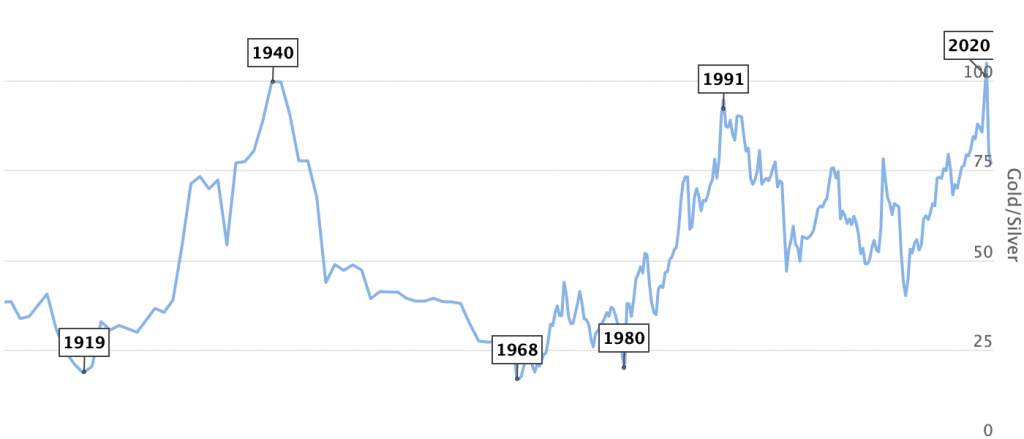

Tracking the gold/silver ratio for potential pairs trading opportunities

If gold prices continue to surge higher, and silver starts to lag, this could create an opportunity to pair these two metals against each other. Traditionally, precious metals traders use the gold/silver ratio to identify potential pairs trading opportunities.

The gold/silver ratio is the price per ounce of gold divided by the price per ounce of silver. The quotient of that equation reports how many ounces of silver are required to buy a single ounce of gold.

During the last 20 years, the gold/silver ratio has ranged between roughly 40 and 110. That means at its current level of 84 ($2,400/$28.50 = 84), the gold/silver ratio is trending toward the upper end of its historical range and is worth monitoring going forward.

What pairs traders do

Traditionally, pairs traders sell gold and purchase silver when the gold/silver ratio reaches an extreme at the upper end of its historical range. This position theoretically benefits from a drop in the ratio—requiring gold to go lower, silver to move higher, or a combination. The opposite position is typically deployed (long gold, short silver) when the gold/silver ratio declines toward the lower end of its historical range.

For more background on the gold/silver ratio, readers can check out this installment of Splash Into Futureson the tastylive financial network. To follow everything moving the markets, including the options and futures markets, readers can tune into tastylive—weekdays from 7 a.m. to 4 p.m. Central Time.

Andrew Prochnow has more than 15 years of experience trading the global financial markets, including 10 years as a professional options trader. Andrew is a frequent contributor Luckbox magazine.

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.