Backtesting the Performance of Short Premium in 0DTE Options

Options with zero days-to-expiration (0DTE) have surged in popularity the last couple of years, and new tastylive research highlights the potential benefits and risks associated with short 0DTE options strategies

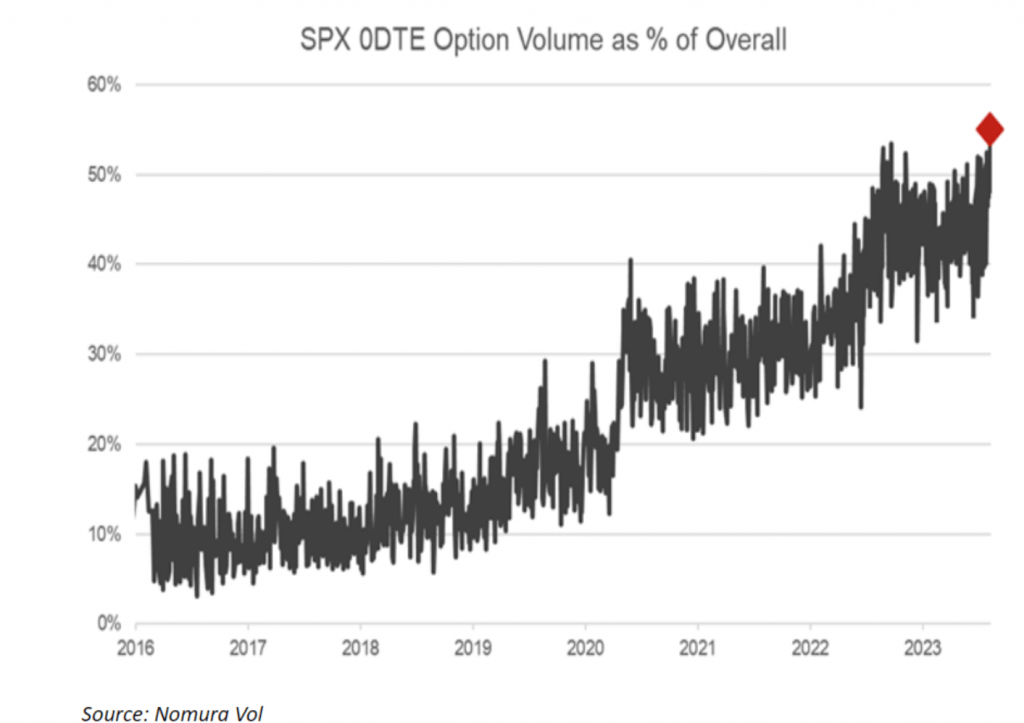

- Trading volume in options with zero days-to-expiration (0DTE) has surged in recent years.

- Short-dated options, such as 0DTE and weekly options, provide added flexibility and agility to active options traders seeking to capitalize upon fast-changing conditions in the market.

- Many options traders use short-dated options for speculation and hedging purposes, but new research indicates that selling short-term options can also produce consistent profits.

- But due to the substantial risks associated with selling naked options, defined-risk trading strategies may be preferred when selling short-term options.

In recent years, the options trading world has witnessed a notable shift towards shorter-dated options, with zero-day-to-expiration (0DTE) options gaining increasing popularity among active market participants. This shift is evident in options trading data, which highlights a growing trend towards the utilization of weekly and 0DTE options.

Options with zero days until expiration only exist for a single trading session and are commonly referred to as zero days-to-expiration (DTE) options, or 0DTE.

A 0DTE option could be a longer-term option that has reached the last day of its lifecycle (such as a monthly, weekly, or LEAPS option), or it could be a specific option that’s listed only for a single trading day.

Particularly striking has been the surge in options with just five days until expiration (5DTE), indicating a preference for shorter duration among traders seeking to capitalize on rapid market movements and volatility.

Recent estimates suggest that around 55% of the total trading volume in the S&P 500 options market now consists of contracts with less than five days until expiration.

Potential for quick gains

The allure of shorter-dated options often lies in their potential for quick gains. These contracts offer traders the opportunity to profit from short-term price fluctuations, providing a swift turnaround compared to longer-dated options.

With the ever-changing dynamics of the market, traders have been drawn to the flexibility and agility that shorter-dated options afford, allowing them to adapt their strategies to rapidly evolving market conditions.

While selling premium with 0DTE can be enticing due to the potential for immediate returns, it comes with substantial risks that can’t be overlooked. That’s primarily due to the acute exposure to sudden and unpredictable movements.

With zero days remaining until expiration, any adverse price action can result in significant losses, amplifying the impact of market volatility on option sellers.

In contrast to selling options premium, buying short-dated options entails defined risk, where the maximum loss is limited to the premium paid.

While the potential for profit may be lower compared to selling options, buyers benefit from capped risk exposure.

However, it’s essential to recognize that consistent purchases of shorter-dated options can also result in significant accumulated losses over time, particularly if the market fails to move in the anticipated direction.

New research on short 0DTE options premium

Keeping in mind the substantial risks associated with selling short-term options premium, recent research conducted by the tastylive financial network illustrates that over the last year, some short-term options trading strategies have been consistently profitable.

Using historical options data in the SPDR S&P 500 ETF Trust (SPY), tastylive conducted a series of comprehensive backtests that assessed the performance of selling short-dated options.

These backtests covered data from March 2023 through February 2024. One of the approaches studied was the iron butterfly, which represents a defined risk strategy.

The iron butterfly strategy combines elements of the short straddle and long strangle strategies. It involves selling an at-the-money (ATM) straddle in conjunction with buying an out-of-the-money (OTM) strangle.

The addition of the OTM strangle provides protection for the short straddle, and therefore caps the potential losses in the worst case scenario.

Defined risk refers to the fact that the maximum potential loss is known, and limited to a specific amount, prior to trade deployment. In contrast, an undefined risk options spread is a strategy where the maximum potential loss is not capped, and can theoretically be unlimited.

The iron butterfly is often used when traders anticipate low volatility in a given underlying and expect the underlying price to remain within a certain price range through expiration.

While an iron butterfly is often thought of as the combination of a short straddle and long strangle, it can also be viewed as the combination of a call vertical spread and a put vertical spread.

Regardless, the most vital aspect of an iron butterfly is that in the worst case scenario, the OTM strangle options provide protection to the short straddle. The maximum potential loss from an iron butterfly is therefore the difference between the net credit received for initiating the spread, subtracted from the width of the spread (the difference between the strike prices of the ATM and OTM options).

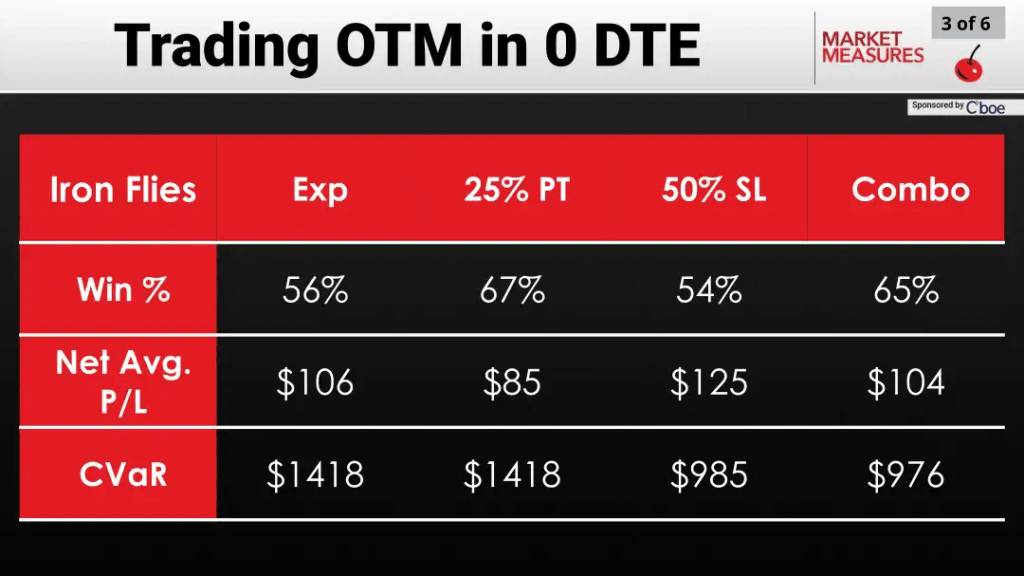

Circling back to the aforementioned research, the 11-month backtest on 0DTE options in SPY showed that the iron butterfly structure produced attractive win rates over the period studied. Several backtests were conducted using different trade management techniques. The results from these backtests are summarized below.

In the above slide, “exp” refers to holding the position through expiration. On the other hand, “25% PT” and “50% SL” are both trade management approaches used in the options world.

The 25% PT refers to closing the position once it reaches 25% of its maximum profit potential, while 50% SL refers to closing the position when it reaches a 50% loss of the initial credit received.

Win rates and risk

In addition to the above, the “combo” (combined) backtest was also conducted, which involves executing the trade management strategy that comes first—whether that be 25% PT or 50% SL.

As shown in that chart above, the 25% PT and combo approaches produced the highest win rates, while holding through expiration and 50% SL produced the highest net average P/Ls.

In terms of risk, the CVaR statistic indicated that the 50% SL and combo trade management approaches possessed the lowest level of risk. In terms of overall risk and reward, that suggests that the combo strategy might be the preferred risk management approach, depending on one’s outlook and risk profile.

In the financial world, CVaR stands for conditional value at risk, also known as expected shortfall. It is a risk metric used in finance to measure the potential loss of an investment or portfolio beyond a certain confidence level.

From a risk management perspective, lower CVaR values are generally preferred, as they indicate a smaller expected loss beyond a given confidence level. A lower CVaR suggests a more conservative and risk-averse approach, which may be desirable for investors seeking to minimize downside risk.

To supplement the iron butterfly data, the tastylive network also ran several backtests involving the iron condor strategy using 0DTE options in SPY. The results of those backtests were also compelling, demonstrating performance statistics on par with the iron butterfly.

Considering the encouraging results of this research, active options traders may want to review the potential of these short 0DTE options strategies in greater detail. To do so, readers can check out this installment of Market Measures on the tastylive financial network.

Andrew Prochnow has more than 15 years of experience trading the global financial markets, including 10 years as a professional options trader. Andrew is a frequent contributor Luckbox magazine.

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.