Volatility Contraction Part 1: Mean Reversion

In finance, mean reversion describes the tendency of asset prices to move toward their average, over time.

A mean reversion-based trade therefore expresses the belief that an asset has deviated too far from its real value—or at least from its mean price—and that opportunities for profit exist when reversion to the mean occurs.

Contrarians, whether they consciously accept it or not, are essentially practitioners of the mean reversion trading philosophy.

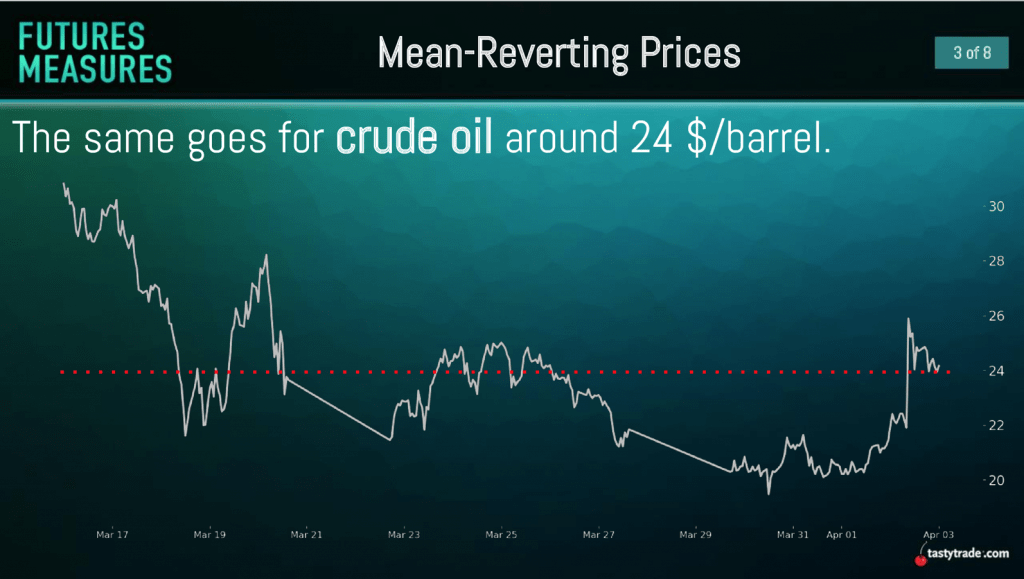

Using a current example, oil prices have plummeted in 2020 due to complications associated with both the demand and supply sides of the world’s most-followed energy source. And with oil prices currently sitting near 18-year lows, traders buying crude exposure at these price extremes are likely doing so because they expect the value of crude to rise back toward its long-term mean.

The chart below illustrates how crude has been orbiting around its shorter-term mean, of late:

Looking at another niche of the financial markets, option securities have consistently demonstrated a tendency to mean-revert, which suggests that volatility traders in the options space are essentially contrarians as well.

The mean-reverting nature of options is best understood through the dual lenses of implied and historical volatility, as outlined below:

- Implied Volatility: Implied volatility is derived from the dollar-and-cent prices of options trading on exchanges and reflects the market’s expectation for movement in the associated underlying over the duration of the contract. This value therefore represents the ongoing market price for volatility in a given options contract.

- Historical Volatility: Every stock has a specific opening and closing price for each trading day of its existence. This historical data can be used to compute what’s known as historical volatility (aka “actual volatility”), which reports exactly how much a security has varied over a defined period of time.

Summarizing the above, implied volatility basically reflects the market’s expectation for movement, while historical volatility (aka “actual volatility”) reports what has actually occurred.

Looking at an example, consider hypothetical stock XYZ that has a one-month historical volatility of 20.

If options with a one-month duration in XYZ are trading with an implied volatility of 29, an opportunity theoretically exists to sell that option with the expectation that actual volatility in the underlying over the upcoming one month period will be less than 29 (and potentially closer to the recent historical volatility of 20).

This sample position, of course, isn’t guaranteed to turn a profit because future volatility at the end of the day is unknown.

At the same time, implied volatility has consistently exhibited mean-reverting behavior, as demonstrated by a wide range of market studies. That means a portfolio composed of many high-probability mean-reversion trades would be expected to be profitable, on average, over time.

The tastytrade financial network developed a term known as “Implied Volatility Rank,” or IVR, to help identify when implied volatility (i.e. the price of an option in volatility terms) has reached an extreme. Implied Volatility Rank reports whether implied volatility is high or low in a specific underlying based on the past year of implied volatility data.

For example, if hypothetical stock XYZ has had an implied volatility between 30 and 60 over the past year and implied volatility in XYZ is currently trading at 45, then XYZ would theoretically have an IVR of 50%.

When IVR is high (above 50%), one can usually expect a contraction to the mean. When IVR is low (below 50%), one can usually expect an expansion to the mean.

Monitoring implied volatility in conjunction with IVR is therefore crucial for options traders because these figures provide important context on the relative price of a given option.

While other trading considerations need to be taken into account, an IVR above 50% might therefore be indicative of attractive options selling opportunities, while an IVR below 50% might be indicative of attractive buying opportunities, due to the mean-reverting nature of implied volatility.

The actual decision to deploy a trade remains dependent on the specific opportunity at hand, as well as a given trader’s associated outlook, strategic approach and risk profile.

Furthermore, another factor that needs to be kept in mind is the existence of time decay, which dictates that all else being equal, options lose value as they approach expiration (i.e. as time passes).

As such, the existence of theta decay puts additional pressure on the long volatility side of the market, because while low implied volatility can mean-revert higher, the positive effects of this action can sometimes be counteracted by time decay.

These are all factors to keep in mind when weighing the deployment of volatility-based positions.

For further reinforcement of the concept of mean reversion, readers are encouraged to review a recent episode of Futures Measures on the tastytrade network that reviews recent movement in a variety of asset classes and provides a clear illustration of mean-reverting behavior in the marketplace, particularly when it comes to directional ranges.

To learn more about implied and historical volatility as they relate to trading options, readers are encouraged to review this previous episode of Ryan & Beef.

Sage Anderson is a pseudonym. The contributor has an extensive background in trading equity derivatives and managing volatility-based portfolios as a former prop trading firm employee. The contributor is not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about topics covered in this blog post, or any other trading-related subject, to support@luckboxmagazine.com.