Trading a Potential Rebound in the Bond Market

The bond market has gotten hammered in 2022, but the pain could be over soon as the current rate-hike cycle might near a conclusion

The 2022 trading year has been somewhat unusual because both the stock and bond markets have experienced concurrent corrections. As of early October, the S&P 500 is down roughly 25%, while the Bloomberg Aggregate Bond Index is down roughly 15%.

Sharp corrections in the stock market aren’t exactly common, but they aren’t rare either. Global stocks pulled back sharply a couple of years ago, as COVID-19 spread across the globe.

However, severe corrections—like the one observed in 2022—are less common in the bond market. Putting the current 15% pullback in perspective, consider that the bond market only dipped by about 10% during the Great Recession (2007-2009).

Bonds have undoubtedly taken it on the chin in 2022. That said, the worst may be over for the bond market—or at the very least, the end may now be in sight.

For bonds, the major headwind in 2022 has been rising interest rates. That’s because bond prices and interest rates share a strong, inverse correlation. When interest rates go up—as they have in 2022—bond prices go down. If anything, the 2022 trading year has served as a strong reminder of that long-standing relationship.

Due to the sharp increase in rates this year, the 2022 bond market is in rare company. Based on records going back to 1926, only two periods have arguably been worse for the bond market—in 1969 and during the Great Recession.

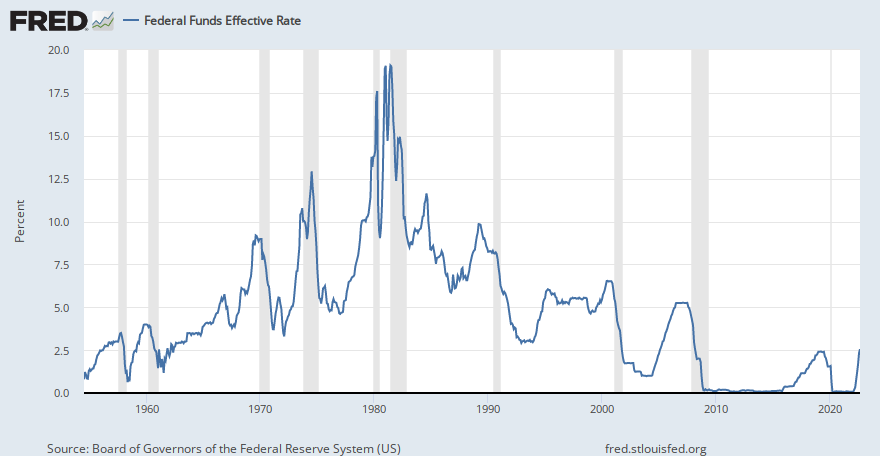

At this juncture, the most important factor for the bond market is where interest rates go from here. Today, benchmark short-term interest rates are currently hovering between 3% and 3.25%—the highest level in the federal funds rate since 2008.

Most projections suggest that the Federal Reserve will hike rates a further 1.25% during the remainder of 2022. Those hikes could potentially raise the federal funds rate to between 4.25% and 4.50%.

Depending on the rate of inflation in early 2023, the Fed could raise rates further, but current projections suggest those rate hikes would be smaller. For example, during Q1 2023, the Fed could hike by another 0.25%-0.50%. But few expect the Fed to raise short-term rates above 5%.

Taken all together, current data suggests that volatility in the bond market could finally abate in 2023. And looking back at history, bonds have traditionally performed well at the end of a significant rate-hike cycle.

In 1979, inflation was even higher than it is today, and the Federal Reserve proceeded to raise benchmark rates over the course of several years. During this period, the U.S. economy suffered through two different recessions, as well as elevated levels of unemployment.

But when that rate-hike cycle ended in 1982, and interest rates started to decline, the bond market came roaring back. According to several measures, 1982 was one of the best years for the bond market. One caveat is that rates had further to fall back then, because the federal funds rate was in the high teens in the early 1980s, as highlighted in the chart below.

Will the bond market rally hard in 2023? That’s difficult to say.

But one thing is certain: Bonds will become a more attractive asset class whenever the current rate-hike cycle comes to an end. And based on current projections, that could occur at some point next year.

But it’s important to keep in mind that a conclusion to the current rate-hike cycle could arrive even sooner, especially if inflation starts to cool in Q4.

To learn more about trading the bond market, check out this installment of Splash Into Futures on the tastytrade financial network. For more context on the 2022 bond market, watch this episode of The Skinny on Options.

For daily updates on everything moving the markets—including in the solar sector—check out TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.