Managing Risk with Beta and Implied Volatility

Active investors can use beta and implied volatility together to cover systematic and unsystematic risks in the market.

Risk in the financial markets is ever-changing, as evidenced clearly by the 2022 trading year.

So far, the S&P 500 is down roughly 16%, while the technology-heavy Nasdaq Composite is down 25%.

At the outset of the year, few would have predicted such poor returns in the stock market, based on how 2021 ended. However, few would have predicted that a full-scale war would break out in Eastern Europe, as well.

But the market is often unpredictable, which is why many investors and traders diversify their holdings in order to help protect against losses when markets experience corrections.

For example, an investor holding the well-diversified SPDR S&P 500 ETF Trust (SPY) is only down 16% so far in 2022, whereas a hypothetical investor only holding Netflix (NFLX) stock would theoretically be down nearly 70% this year.

If both portfolios were valued at $100,000 to start the year, the S&P 500 portfolio would be down to $84,000 right now, while the portfolio holding NFLX would be down to $30,000. That’s an incredible difference.

So how can active investors manage their risk exposure in the stock market? There are many portfolio measurements and tactics used to address risk, but one relatively straightforward metric to track is beta.

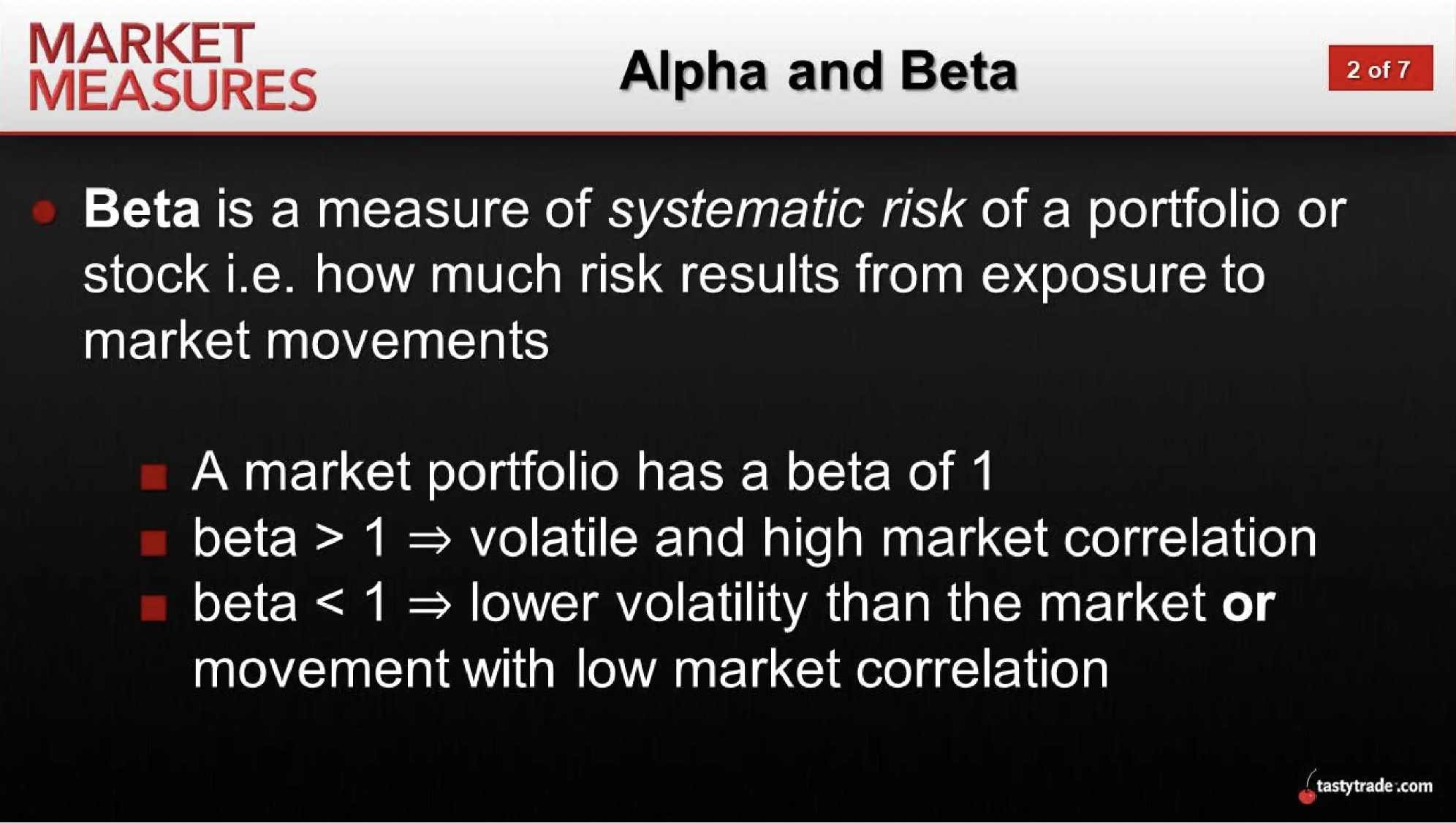

In the financial world, beta measures a security’s risk compared with the market as a whole. For this reason, beta is often referred to as a “market risk” or “systematic risk” measurement. It should be noted that beta provides an approximation of risk and can change over time.

Beta is essentially a statistical measure of a stock’s relative volatility to that of the broader market, which is why it is interpreted as a measure of “riskiness.”

By definition, the market itself has a beta of 1.0, and individual stocks are ranked according to how much they deviate from the macro market. High-beta stocks (>1.0) are supposed to be riskier but provide the potential for higher returns. Low-beta stocks (<1.0) theoretically pose less risk but also lower potential returns.

For example, if hypothetical stock XYZ has a beta of 1.5, then we would expect XYZ to move, on average, 50% more than the market. So if the S&P moves up or down 1%, we would expect to see XYZ move up or down 1.5%.

Using some real-life examples, the above means that the SPDR S&P 500 ETF Trust (SPY) has a beta of 1.0. On the other hand, the current beta for Tesla (TSLA) is 1.44, while the current beta for Netflix is 0.97.

Those betas indicate that if SPY were to move up by 1%, then TSLA would theoretically move up by 1.44%, while NFLX would theoretically move up by 0.97%.

By tracking a security’s beta, active investors can therefore get a better feel for how that security might move during a big rally, or a big correction—the latter of which has played out in 2022.

But one can’t overlook the fact that beta only estimates the market (aka systematic) risk associated with a given security. Stocks are also subject to unsystematic risk (aka stock-specific risk), which can help explain why a given security might be moving more than the amount implied by its beta.

In 2022, Netflix provides a good example of stock-specific risk.

As part of the company’s Q1 earnings report, Netflix revealed that it had suffered a decline in subscribers for the first time in 10 years. That unsystematic (aka stock-specific) risk likely helps explain why NFLX is down so much this year—and why it has performed even worse than what was implied by the stock’s beta.

Together, both systematic and unsystematic risks are referred to as “total risk.”

At a high level, systematic risk is often viewed as the risk inherent in carrying a particular class or type of assets, whereas unsystematic risk involves the risk associated with a specific investment/trading opportunity.

To gauge total risk, market participants can use implied volatility in the options market, in addition to beta, to help ascertain the risks associated with a given underlying.

While options are priced in dollars and cents in the marketplace, these values can be reverse-engineered to calculate a market value in volatility terms. The resulting calculation is called “implied volatility” and represents the market’s expectation for future movement in the price of a given underlying.

Looking at an example, imagine that implied volatility in SPY is currently 15%. That means that over the next year, SPY is expected to close between 15% up and 15% down from today’s price. According to standard deviation theory, this has a 68% chance of occurring.

Because implied volatility is the value observed in the market, that means it represents the sum of all market’s participant’s expectations. It’s therefore the market’s best estimate of the future performance in a given underlying—reflecting the total inherent risk, including systematic and unsystematic factors.

Active investors can therefore refer to implied volatility to help gauge risk, even if they aren’t specifically trading options or volatility. For reference, the current implied volatility in NFLX is 63%.

Of course, the CBOE Volatility Index (VIX) can also be used to assess the market’s assessment of high-level risk in the market.

The VIX represents a theoretical weighted blend of prices on a range of OTM options in the S&P 500 index. The value of the VIX index therefore changes with the demand for these options, which is why it is said to reflect the market’s appetite for risk.

The VIX is currently trading roughly 29. Interestingly, the 30s level has come to represent significant resistance in the VIX because the metric has not traded above 40 since 2020. As highlighted recently in Luckbox, that’s a level to watch closely in the coming weeks.

And to manage total risk most effectively going forward, market participants can track and utilize all the aforementioned metrics: beta, implied volatility and VIX.

For more background on beta, readers can review this previous installment of Market Measures on the tastytrade financial network. To learn more about implied volatility and its practical application in the markets, this episode of Engineering the Trade is also recommended.

To follow everything moving the markets, readers can also tune into TASTYTRADE LIVE at their convenience.

Get Luckbox! Subscribe to receive 10-issues of Luckbox in print! See SUBSCRIBE or UPGRADE TO PRINT (upper right) for more info or visit getluckbox.com.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.