The Next Fed Meeting is in December, Here’s How to Trade It

The last 2022 meeting of the Federal Reserve is set for Dec.13-14, and market participants can trade that event using Treasury yield futures or government bond ETFs

Benchmark interest rates in the United States have jumped by more than 4,000% this year, making this niche of the financial markets one of the most dynamic on earth.

Short-term interest rates in the U.S. are controlled by the Federal Reserve via the federal funds rate. The federal funds rate started 2022 pegged at effectively 0%, and is currently hovering between 3.75% and 4.00%.

Traditionally, the Federal Reserve exercises its control over U.S. monetary policy by raising or lowering the federal funds rate. By adjusting rates the Fed can influence the borrowing behavior of individuals and businesses.

For example, when the economy is contracting, the Fed can lower benchmark interest rates to help embolden borrowers. A good example of this approach was observed during the Great Recession, when the Federal Reserve dropped the federal funds rate to zero for the first time in American history.

The goal at that time was to entice fresh borrowing to help promote a much-needed expansion in the underlying economy.

In 2022, the Federal Reserve has been forced to do the opposite as a result of rampant inflation. So far this year, the Fed has raised the federal funds rate by more than 4,000%. That’s the sharpest and most rapid increase in benchmark rates since the early 1980s.

Not coincidentally, the early 1980s was also the last time the U.S. experienced an inflationary environment like the one observed during the last 18 months.

Trading Fed Interest Rate Decisions Using Treasury Yields

The federal funds rate can’t be traded directly, so most investors and traders use what’s known as Treasury yields to trade their outlook on interest rates.

In this context, Treasury refers to U.S. government debt, while yield refers to the interest rates paid on that debt. The federal funds rate, controlled by the Federal Reserve, shares a strong positive correlation with Treasury yields.

As noted previously, the federal funds rate has increased from zero to about 4.00% in 2022. During that same period, the yield on the 10-year Treasury bond—one of the most visible U.S. government bonds—has increased from 1.50% to 4.10%.

The 10-year Treasury yield is one of the most followed government bonds on earth, which is why it is usually cited as the benchmark for U.S. rates.

There are other U.S. government bonds with different durations. For example, the 2-year Treasury bond and the 30-year Treasury bond. Those products typically trade with a slightly different yield than the 10-year Treasury due to the varied duration of each product.

Generally speaking, however, Treasury yields typically rise across the board as the federal funds rate goes up, while Treasury yields typically decline as the federal funds rate goes down.

Trading Fed Decisions with Treasury Yields and ETFs

Investors and traders involved in the Treasury bonds market typically use futures and/or bond ETFs to express their market opinions.

For example, the Small Treasury Yield (S10Y) offered by the Small Exchange is directly tied to the percentage yield of the U.S. 10-year Treasury bond—one of the most widely accepted global benchmarks for interest rates.

So if an investor or trader expects interest rates to increase further, he or she might purchase the S10Y. Conversely, a trader expecting interest rates to decline might sell the S10Y.

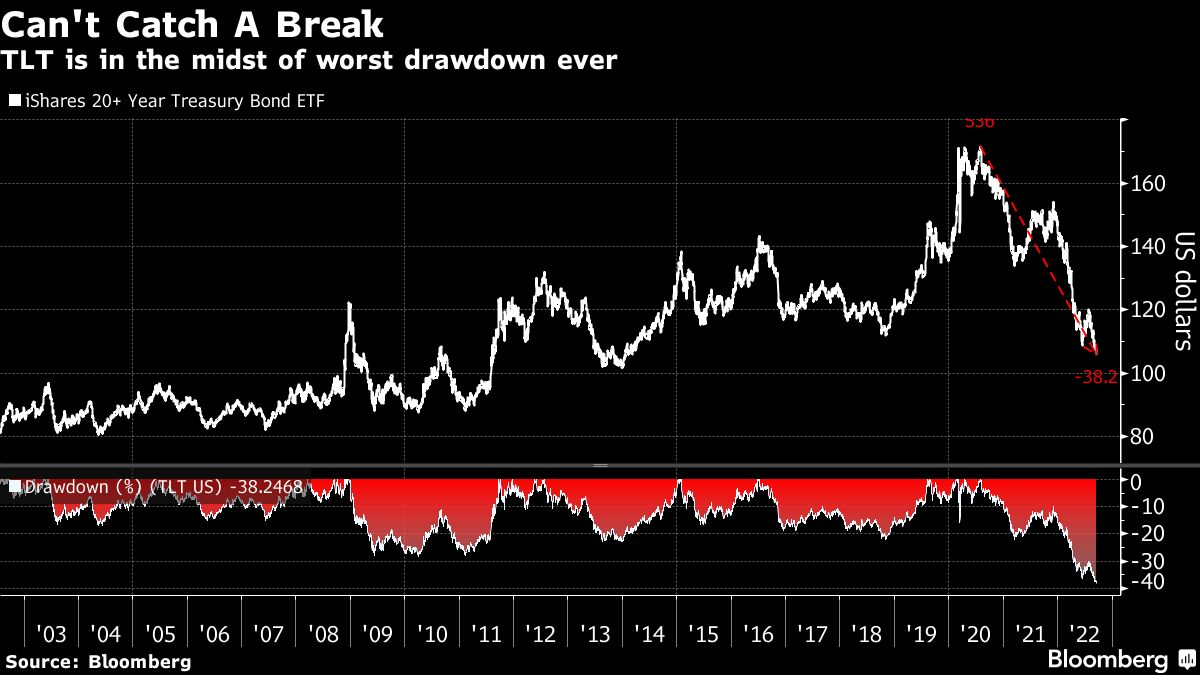

Investors and traders that want to trade interest rates, but don’t want to do so using futures products, can also consider bond-focused ETFs. One of the best-known ETFs in this space is the iShares 20+ Year Treasury Bond ETF (TLT).

TLT is a close proxy for long-term U.S. government bond prices (20+ years) in ETF form. This is outlined in the TLT fund summary, which indicates that TLT invests “at least 95% of its assets in U.S. government bonds.”

Bond prices are inversely correlated with interest rates. Meaning that when interest rates go up, bond prices go down. That in turn means when interest rates go up, TLT goes down.

So far in 2022, aggressive rate hikes have been instrumental in pushing government bond valuations lower—and along with them, the TLT.

TLT started 2022 trading at $144/share, and is currently trading about $98/share—a year-to-date decline of roughly 32%. Based on current projections for additional rate hikes, that means there may be further downside ahead for TLT.

On the other hand, an investor or trader expecting interest rates to reverse course might consider buying TLT. Most projections suggest the Fed will stop raising rates at some point in H1 2023 (if not earlier). Whenever that day arrives, the so-called Fed pivot could be a positive for TLT.

As always, it can be prudent to mock trade (i.e. paper trade) a new product before deploying a new live position, just to better understand the associated risk dynamics of that product.

The next meeting of the Federal Reserve is set for Dec. 13-14, with most projections indicating the Fed will hike rates by another half point—or three-quarters of a point—during the group’s final meeting in 2022.

For more context on government bond ETFs, check out this recent installment of Market Measures. For daily updates on everything moving the markets—including interest rates and Treasury yields—monitor TASTYTRADE LIVE, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.