Master the Rebound: Long Stock or the Short Put?

When an investor or trader purchases stock, he is obviously hoping that the value of the underlying will increase. For situations in which a trader is expecting a sharp rise in the price of the underlying in the near-term, long stock is certainly one choice available to the trader.

However, there may be situations when different position structures, such as short puts, may be a more appropriate position choice – depending on one’s outlook and risk profile.

As a reminder, the risk to a long stock position is that the underlying drops (possibly precipitously) and that the associated position incurs losses. After such a drop, a decision must be made whether to hold the stock or to cut one’s losses and close the position.

When selling puts, a trader is also at risk of getting long stock. If the strike of a short put is breached, and the options are exercised, the short put seller must purchase 100 shares of stock at the strike price for every contract sold.

In this regard, both a long stock position, and a short put position, can ultimately end up as the same exposure (long stock). Sizing is therefore extremely important for option sellers because the addition of each contract represents another 100 shares at risk. Aside from a down move in the underlying, short puts can also lose money if implied volatility rises.

But what if a trader envisions a stock sitting still for the foreseeable future? Or at least expects it to trade in a relatively tight range?

In that hypothetical scenario, a trader might consider selling puts as opposed to buying stock, because the position should generate a more attractive return on capital for the expected circumstances. Obviously a long stock position that sits still at best breaks even. A short put under the same conditions can work perfectly, with similar overall exposure (assuming correct sizing).

A short put also theoretically comes with a buffer built into the position – that being the premium received from the option sale. For example, if hypothetical stock ABC is trading for $33, and a trader sells the $30 put with 45 days-to-expiration for $1.50, the position breaks even if ABC drops to $28.50.

On the other hand, if the trader purchases long stock for $33/share in ABC, and the stock drops to $28.50, the trader will lose money all the way down.

One should also keep in mind the reverse situation: If ABC rallies. Under that hypothetical scenario, the long stock position does offer additional potential upside rewards, as compared to a short put, assuming it rallies significantly.

These examples help illustrate why a variety of approaches can be considered – it all depends on what is expected, and the risk profile desired in the position.

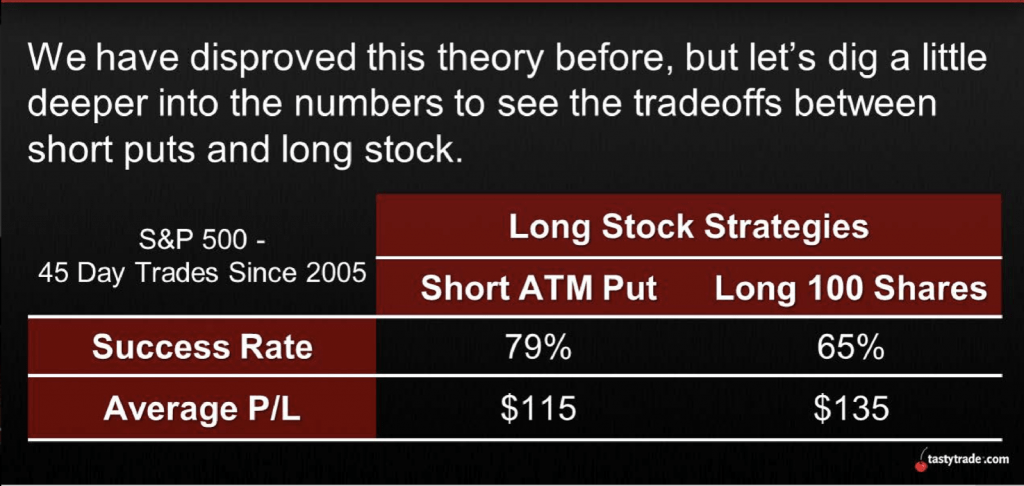

A natural question to ask at this point is which of the two strategies has performed better over time?

On a previous episode of Market Measures on the tastytrade financial network, a comprehensive market study is presented which highlights the historical performance of long stock versus short puts in SPY.

The results of at study, as summarized below, can help traders better understand how each strategy has performed in a side-by-side comparison:

It should be noted that the research conducted for this comparison was only in SPY (an index). This means that the approach may not necessarily be applicable to other underlying symbols, particularly single stocks.

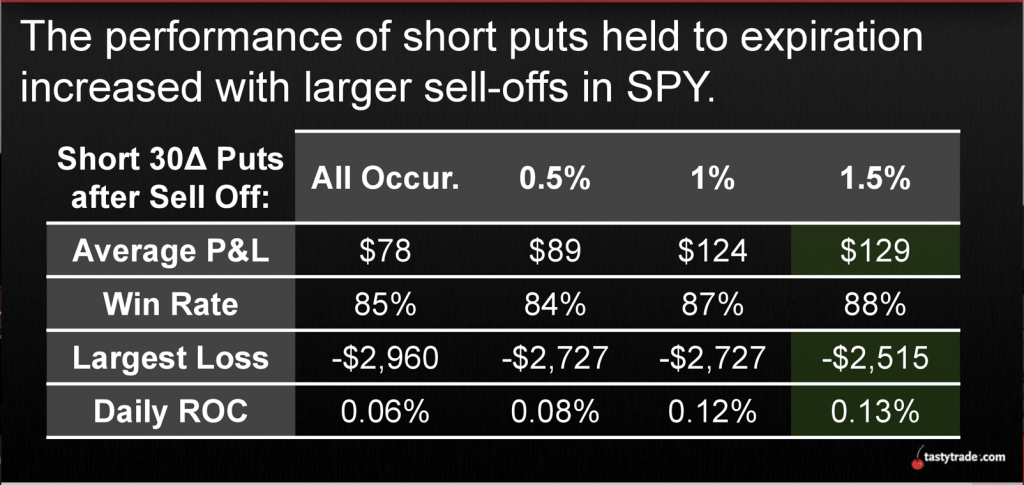

Recently, the tastytrade research team further examined this topic, specifically by analyzing whether the short put approach can be optimized by selling into market weakness, which means the short put approach was backtested when deployed only after significant down days in the stock market.

Down days were broken down into three different categories (0.5%, 1.0%, and 1.5%), to help ascertain whether there were any major differences in performance. The results of this research are summarized below:

As one can see in the data above, the performance of short puts did improve when filtering for opportunities in the wake of market weakness, especially as the down move got relatively more severe.

Due to the complexity of this material, traders may want to review the complete episodes of Market Measures focusing on short puts and long stock when scheduling allows.

Sage Anderson is a pseudonym. The contributor has an extensive background in trading equity derivatives and managing volatility-based portfolios as a former prop trading firm employee. The contributor is not an employee of luckbox, tastytrade or any affiliated companies. Readers can direct questions about any of the topics covered in this blog post, or any other trading-related subject, to support@luckboxmagazine.com.