Mastering the Vertical Spread

Many options traders have a good idea of the specific trading approach they might choose to employ when identifying an opportunity in the marketplace, especially if it capitalizes upon an extreme level of volatility or price.

For example, a short straddle or short strangle tends to be a popular choice when volatility is high, while naked options can be a great go-to for a high-confidence directional bet.

However, there’s another choice available to traders when they hold an opinion on both volatility and price direction—the vertical spread.

The key to understanding a vertical spread is to visualize it as a naked options position, but with a “wing” deployed as a hedge to help protect the position from outsized losses. It should be noted that the wing in a vertical can also serve to reduce potential gains – depending on what type of vertical is deployed, and what ultimately unfolds in the underlying.

Along those lines, the wing (the second leg of the spread) in a vertical spread is essentially what transforms this position into a defined-risk exposure – meaning the potential maximum gains and losses of the spread are clearly defined prior to trade deployment. This can be a huge benefit to traders that are seeking to reduce the risk of unexpected losses in their portfolios.

Getting down to actual position mechanics, a vertical spread is constructed using one long option, and one short option. In a vertical, both options should be of the same type (two calls or two puts) and in the same expiration month, but of different strike prices.

Accordingly, a vertical consists of a long call and a short call, or a long put and a short put. Moreover, one of the options in the spread will be in-the-money (ITM), while the other will be out-of-the-money (OTM). The latter, OTM option, serves as the “wing” of the position.

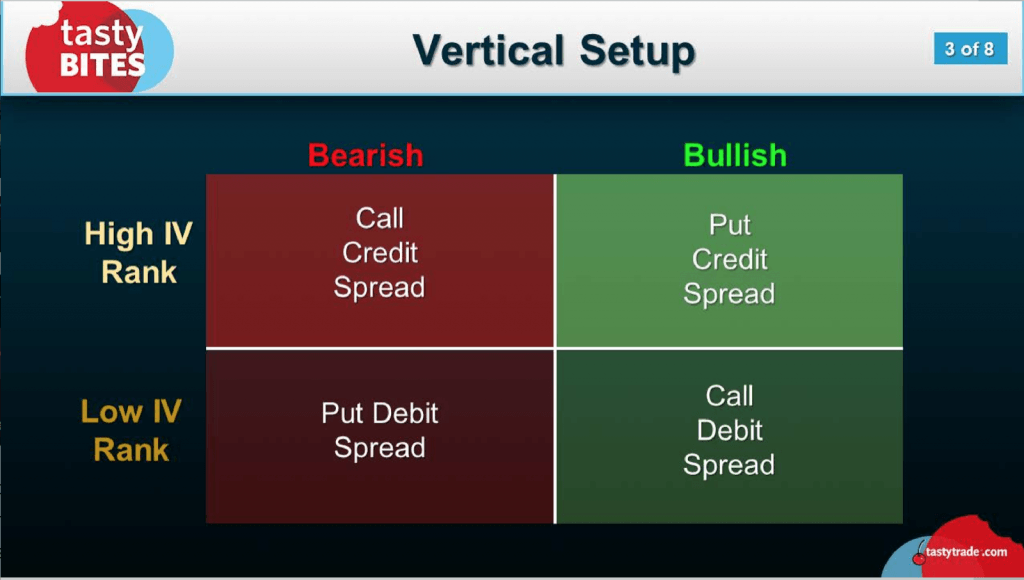

Taking the above all together, a vertical spread can be deployed in four different ways:

- long ITM call, short OTM call (call debit vertical spread)

- short ITM call, long OTM call (call credit vertical spread)

- long ITM put, short OTM put (put debit vertical spread)

- short ITM put, long OTM put (put credit vertical spread)

Citing a hypothetical example using the first bullet point (call debit vertical spread), imagine there exists a publicly traded technology company that is preparing to announce a new product offering. For example, imagine that company ABC is preparing to announce a new smartphone that features foldable screen technology.

For the sake of this example, let’s further assume there exists a trader who is a strong believer in the new product, and is expecting a moderately bullish move in the wake of the announcement. Let’s also assume that this trader believes the market has overlooked the potential impact of this event, and views the implied volatility in the options of ABC as “cheap.”

As mentioned at the outset of this piece, this trader essentially holds a view on both price and volatility – as opposed to a view on only one or the other. The vertical that best fits this outlook is outlined in the first bullet point above, a long ITM call against a short OTM call.

The reason this structure is particularly suitable is threefold. First, the trader will have expressed his/her bullish opinion using the long ITM call – the more elementary aspect of the position. Second, the trader will have expressed his/her opinion that volatility is cheap by purchasing option premium, also via the long ITM call.

The last piece of the puzzle is the short OTM call. This leg of the position provides a potential benefit to the trader if his/her outlook ends up being incorrect. That’s because the short OTM call provides the trader with a credit (i.e. short premium) which effectively reduces the cost of the ITM call debit (i.e. long premium).

The total “cost” of a debit vertical spread is calculated by taking the long premium less the short premium, which in sum is referred to as the total “debit.” If the event comes to pass, and underlying ABC fails to rally, or goes down in value, the trader will have saved himself/herself valuable capital via short OTM call premium.

The maximum potential loss from a call debit vertical spread is the total premium outlaid to establish the position. And one can see fairly easily how the short OTM call “wing” helps to reduce the maximum loss.

However, the maximum potential gain is also capped when employing this position structure.

The maximum potential gain from a call debit vertical spread is the difference between the two strikes, less the net debit paid for the spread. So if the distance between strikes is $5, and the net debit for the spread is $2, then the maximum potential gain would be $3 (multiplied by 100 times the number of contracts, or $3 x 100 x 1 contract = $300). The maximum potential loss in this same example is $2 x 1 contract x 100, or $200.

These numbers help illustrate that an important consideration for a trader employing this structure is that the underlying rallies dramatically, in which case the short OTM call ends up capping the potential gains from the long ITM call. That’s one reason the call debit vertical is possibly more suitable when a moderate rally is expected in the underlying, as opposed to a dramatic rally – although the position would still profit under both scenarios.

While the above example describes a spread typically referred to as Call Debit Vertical Spread (long call vertical), the other three types of vertical spreads can also be easily understood and utilized to fit specific market outlooks, as illustrated in the chart below.

As a reminder, “credit spreads” refer to positions in which the trader collects premium when taking into account the combined cost of the spread, whereas “debit spreads” refer to positions in which the trader outlays premium when taking into account the combined cost of the spread.

Generally speaking, debit spreads are long premium positions which benefit from rising implied volatility environments, while credit spreads are short premium positions which benefit from declining implied volatility environments.

Traders seeking to learn more about the type of market outlook that might fit each of the four vertical spreads may want to review a recent episode of tasty Bites on the tastytrade financial network. This episode provides a comprehensive review of vertical spreads, including some key insights on sizing the distance between strikes, and how to manage verticals once they are deployed.

A summarized version of key points related to vertical spreads can also be reviewed in the tastytrade LEARN CENTER.