Trading Skew with Debit and Credit Spreads

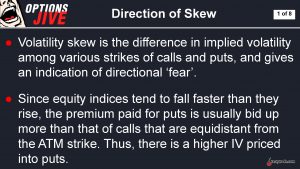

Puts are traditionally more expensive than calls in the options marketplace due to the existence of “skew.”

When trading options and volatility it’s paramount that market participants understand “skew.”

Skew is a risk concept, and can provide investors and traders with important insights into the perceived risk in a given underlying.

For example, puts usually trade slightly richer than calls in the options marketplace because of the potential for price corrections. The sharp selloff in the financial markets on Sept. 20 provides a timely illustration of why this has traditionally been the case.

In that regard, skew accounts for the fear that markets crash down more frequently than they do up. That fear is represented in the “skewed” pricing of options—meaning puts are usually more firmly bid than calls due to the added risk premium inherent in these contracts.

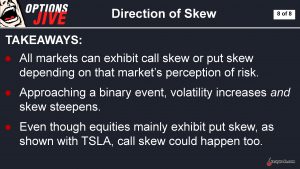

However, there are also instances in which skew materializes in reverse fashion—which is why it’s typically referred to as “reverse skew.”

In such cases, the calls are normally priced higher than the puts. Reverse skew is often found in high-flying “momentum” names from the technology sector, or the “meme” group.

Another sector that often exhibits reverse skew is precious metals. This makes sense because precious metals typically benefit from a “flight to safety” during a market-wide correction. As a result, the risk of “crashing up” in precious metals is perceived to be greater than the risk of “crashing down.”

The above means that for a traditional underlying such as J.P. Morgan (JPM), one could pull up the associated options market and find that calls and puts trading equidistant from the current price of the stock would be trading in traditional skewed fashion—meaning the puts would be trading at a slightly more expensive price than the calls, all else being equal.

Alternatively, in a meme stock such as AMC Entertainment (AMC) or a precious metal’s ETF such as VanEck Vectors Gold Miners ETF (GDX), one might reasonably expect to see the options market skewed to the upside, with calls trading slightly richer than puts—all else being equal.

Considering that one of the primary goals of options trading is to sell expensive options and purchase cheap options, one can see why an understanding of skew is paramount in this endeavor. And the importance of risk management in trading and investing is another reason that an awareness and understanding of skew is so critical.

It’s important to note that skew is not a predictor of price direction. Just because an options marketplace is skewed toward the puts or the calls, that doesn’t mean the underlying is more likely to move in that direction.

Theoretically, that means some options traders and investors might view a skewed options marketplace as an opportunity—depending on one’s unique strategy, outlook and risk profile.

One tactic market participants can use to take advantage of skew are credit and debit spreads. These spreads are “defined-risk” positions typically deployed when an investor or trader views a given option as too cheap or too expensive.

Importantly, when option premium is purchased, such transactions are typically referred to as a “debit,” because the amount paid for the option is “debited” from the investor/trader’s account. Alternatively, when an options market participant sells an option, the premium received from the sale is typically referred to as a “credit.”

The terms “debit” and “credit” are also used when trading option spreads, even though such positions usually involve both the purchase and sale of two (or more) different options. In this usage, debit or credit refers to the net result of the combined position.

For example, “credit spreads” refer to positions in which the investor/trader collects premium when taking into account the net cost of the spread, whereas “debit spreads” refer to positions in which the trader outlays premium when taking into account the net cost of the spread.

As it relates to skew, one can see how an options trader might seek to sell credit spreads on the skewed side of the options marketplace—if such options are deemed expensive. And alternatively, why an options trader might seek to purchase options on the non-skewed side of the marketplace—if such options are deemed cheap.

In these instances, spreads may be deemed more appropriate than naked options positions, due to their defined-risk nature. Defined-risk refers to the fact that maximum potential gains and losses are known prior to position deployment, which can be an important consideration when trading in symbols with heavy skew.

At the end of the day, skew materializes as a result of market perception—meaning that investors and traders have pushed up the value of a certain group of options because they perceive that a higher degree of movement is possible. But as noted earlier, that doesn’t mean the underlying is any more likely to actually move more than usual, or in a particular direction.

To learn more about skew in the options marketplace, and how to take advantage of it, readers are encouraged to review a new episode of Options Trading Concepts Live on the tastytrade financial network. More information on skew can also be reviewed on this previous episode of Options Jive.

For updates on everything moving the markets, TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CST—is also recommended.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.