Apple’s EV Advantage

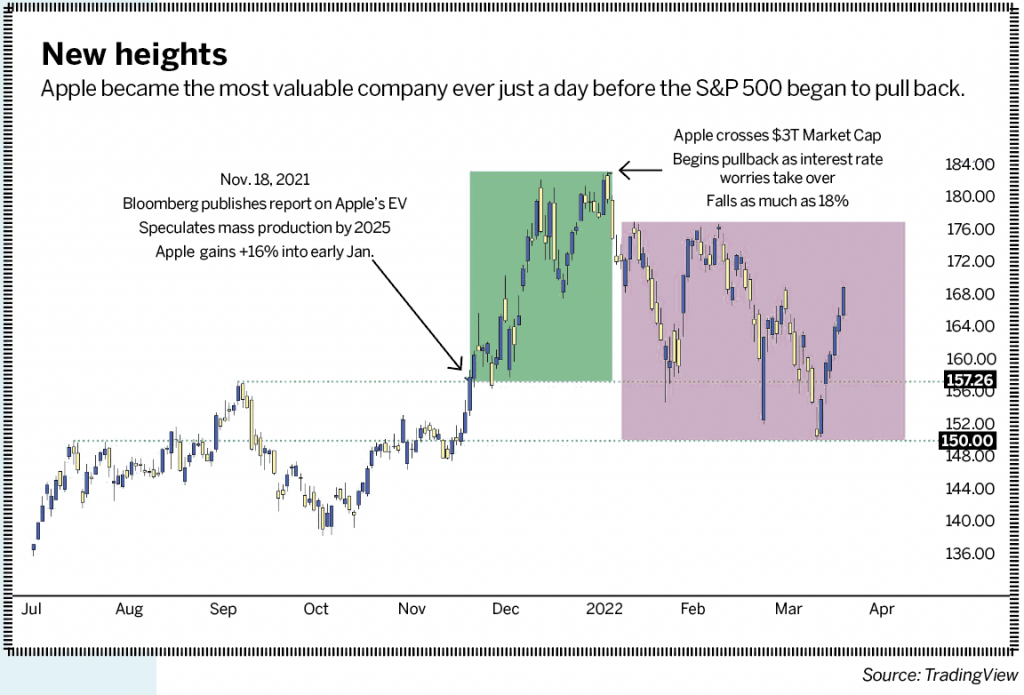

As the company’s market cap was topping $3 trillion, the highest ever for a U.S. company, details emerged about its electric car

Move over Tesla. Rumors of an Apple (AAPL) electric vehicle project had been swirling for quite a while when late last year, a Bloomberg story laid out some specifics about its planning and development.

The report came as Apple’s stock was reaching an all-time high, and that strength lasted through the end of 2021 and into 2022 as it gained another 16%. In fact, when trading opened for the year on Jan. 3, Apple became the most valuable company ever in the eyes of Wall Street.

It happened just a day before the S&P 500 began to pull back from its own all-time high and provided clear evidence of just how powerful something new can be for a well-established product lineup.

Apple might redefine electric cars in the same way it reinvented smartphones. The company may be working on what the National Highway Traffic Safety Administration (NHTSA) calls “Level 5” autonomy—cars that don’t require human intervention and might not even have a steering wheel or pedals. The seats would face each other because no one would be responsible for watching the road.

That would break new ground. At this stage, Tesla is marketing what the NHTSA categorizes as “Level 2,” which means that operators must pay significant attention to the road and have at least one hand touching the steering wheel.

The backstory

Like the iPhone or iPad or even the Apple Watch, Apple’s foray into automobiles has been surrounded by rumor long before the company made any formal product announcements. Development supposedly began in 2014 under the code name “Project Titan.” As many as a thousand experts and engineers worked in a secret location near Apple’s campus in Cupertino, California.

In the next six years, rumor sometimes had it that Apple had abandoned the project. The company’s penchant for secrecy made it difficult to obtain reliable information.

But Apple CEO Tim Cook hinted at what was to come when he announced in 2017 that the company was at work on autonomous systems.

“It’s a core technology that we view as very important,” Cook noted. “We sort of see it as the mother of all AI projects. It’s probably one of the most difficult AI projects to actually work on.”

Many took that as a reference to an Apple automobile, and the statement still reverberates.

Apple’s advantage

On Nov. 18, Bloomberg confirmed Apple’s plans for an electric vehicle and described specifics about what Apple is contemplating with an electric car.

Apple shelved plans for a vehicle with limited self-driving capability, which would have competed with today’s Tesla-like offerings, the Bloomberg article said. Instead, Apple is concentrating on vehicles that need no human intervention.

The November update also indicated Apple has completed the core work for the EV project, which was called “the most advanced component that Apple has developed internally.”

That can enable Apple to redefine the EV market and set itself apart from the pack. It could also transform Apple from a consumer electronics company into a transportation company that may revolutionize the way Americans commute.

Possible timelines

Elon Musk often laments that it’s expensive to get into the automotive business and the margins aren’t that attractive. Innovation requires investments in research and development that can discourage entry.

Even though Apple is sitting on $200 billion in cash, it doesn’t seem prudent to enter such a capital-intensive process. That’s why many expect Apple will form a partnership with an established automaker. The question is which one that might be.

Apple was struggling to find a proper fit and may be looking into contract manufacturers, such as Foxconn, which has a relationship with the company as the main producer of iPhones. Foxconn recently rolled out an electric vehicle chassis and a software platform to help manufacturers hit the market more quickly, and this could be a good fit for Apple.

Apple is close to signing a contract with LG Magna e-Powertrain, but that option offers less manufacturing capacity and would likely be a much smaller rollout, according to a report in The Korea Times. That would be an attractive option if Apple wanted to test the product and gauge acceptance before tackling the mass market.

Recent reports also pointed to a possible partnership with Porsche, which is in its own cycle of change. The company may be looking at an IPO in the coming months or years as it splits off from Volkswagen (VW). So, a partnership with Apple could cement that move as VW, Porsche and Apple team up to roll out a new, cutting-edge technology that benefits from the expertise of all three companies.

When to expect such a product seems like a much larger question. Bloomberg’s report suggested the company is targeting a 2025 release. But, more recent comments from noted Apple supply chain analyst Ming-Chi Kuo indicated much of the team had been dissolved and would need to be reorganized within the next three to six months in order to begin mass production by 2025.

This was taken from a comment in mid-March, which would put the timeframe for reorganization between June and September of 2022 to move toward mass production in 2025.

Apple’s stock

A week before Thanksgiving, Apple’s stock price was back up to $157. The company reached an all-time high at that price a couple of months earlier, but that was followed by a 12% drawdown.

When the price approached that level again in November, traders started to tighten up—the way they often do on a second test of a major spot of resistance. But then the report of Apple’s EV hit the wires and gave investors a new reason to get excited.

But Apple’s market capitalization poses a problem for the growth of its stock price. To rise 33%, the company would need to add about a trillion dollars in market cap. That seems unrealistic because only a handful of companies are worth more than a trillion dollars in today’s market.

However, strong growth rates seem reasonable. Apple is trading at a price-to-earnings ratio of 27, comparable with Google’s 24 or Microsoft’s 32. That places Apple in line with other consumer electronics companies. With a PE ratio for the S&P 500 as a whole of $25.44, Apple is trading in line with the broader blue-chip index, too.

But compared with EV manufacturers, Apple begins to look at value play. Tesla is trading at 185x earnings, and other EV competitors, such as Lucid or Rivian, aren’t profitable so they don’t even have a PE ratio, yet both are currently worth over $40 billion in market cap. Hope and potential drive the EV industry, and the fact that Apple trades closer to Microsoft than Tesla speaks to growth potential for Apple if it succeeds in the EV market.

What’s more, it seems that hope for Apple’s EV project has not been priced into the company’s stock, which has continued to trade around the same $157 level that previously set resistance. As markets pulled back in January for fear of a hawkish attitude on the Federal Open Market Committee, Apple’s stock responded, too, dropping by as much as 18%.

It appears investors can buy stock in the Apple consumer electronics business at a reasonable valuation. Meanwhile, they gain the long-term growth kicker of Apple’s potential redefinition of the EV car. That can make Apple an attractive candidate for long-term EV exposure without taking on the risk of a highly speculative, unprofitable new entrant, such as Rivian or Lucid.

The self-driving EV

Investors have some time to consider Apple’s prospects, given the company won’t bring big changes to the EV industry before 2025. Meanwhile, Apple remains solid in operations and iterative releases of the iPhones, iPads and MacBooks that keep operating cash flow at high levels. The dividend yield of 0.53% illustrates that profitability.

As the Federal Reserve tries to tame inflation, it may continue to hike interest rates. That’s highlighted in the recent sensitivity of tech stocks, Apple included, and could open the door for an attractive buying opportunity possibly later this year.

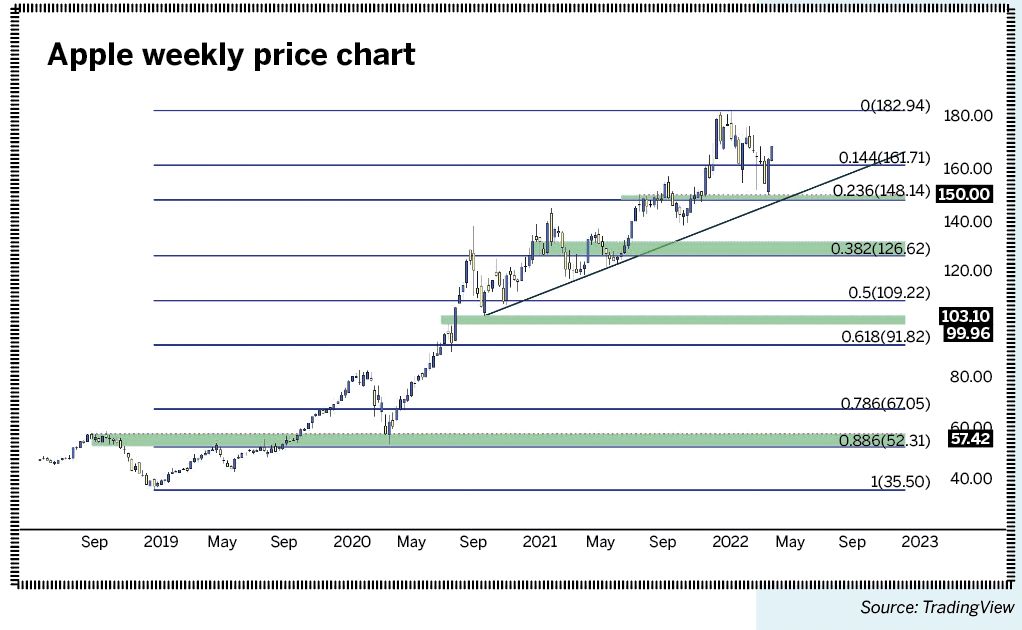

Taking a long-term view of Apple’s chart, the price of around $57.50 jumps out because that was the high in 2018 that helped cauterize support in March of 2020, as COVID-19 was getting priced into U.S. markets. But for that zone to come into play, the market would need to pull back more than 65%.

If that happens, the S&P 500 would probably enter the 2,000 area, which seems unrealistic. So, $57.50 could remain a key support level in Apple, but it seems incredibly unlikely that will come into play unless the markets blow up. But if that scenario does occur, that’s a very attractive level for long-term accumulation of Apple’s equity.

More reasonable, however, would be a pullback to the $150 level, which had functioned as resistance during the summer of 2021 and showed up again for support in March 2022. For investors skeptical of a larger market correction or pullback later this year on the basis of a hawkish Fed, this could be an attractive support level for entry. This price is confluent with a bullish trend line connecting the lows from late-2020, and if price holds, then the bullish trend remains in working order.

Investors can seek deeper support in the area around $130, and there’s another spot around the psychological level of 100. Each of these prices could support longer-term approaches on Apple, looking to institute value-based logic in response to a larger market correction.

At current earnings per share of $6.08, prices trading in the $130 area would be a price-to-earnings ratio of 21.3, while the $100 support level would be 16.45, both of which could be attractive valuations for Apple’s current operation and even more so with the added kicker of growth potential from EV product announcements.

James Stanley, a senior strategist for DailyFX, helps direct educational articles and web seminars. @jstanleyfx