What You Need to Know About Trading ‘Zero-day’ Options

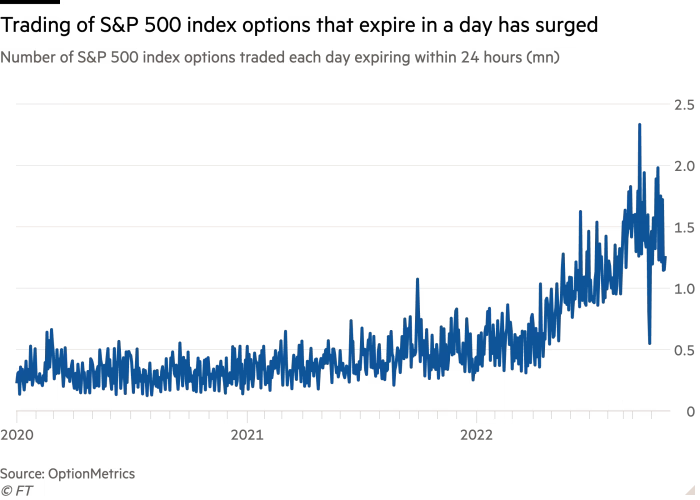

Options with zero days until expiration only exist for a single trading session, and recent market data suggests that trading volume in these Zero-day, or 0DTE, contracts has been surging in recent months

Trading activity in the options markets has exploded since the start of the COVID-19 pandemic, and that’s led to some new approaches to trading options. Or at the very least, popularized some old approaches to trading options.

The latest craze involves options with zero days until expiration—commonly referred to as zero days-to-expiration (DTE), or 0DTE.

Trading volume in 0DTE options has grown rapidly in recent months. Estimates now suggest that the total notional value of all 0DTE options has risen to roughly $1 trillion on any given day.

Moreover, it’s believed that approximately 46% of the total trading volume in the equities options market now consists of contracts with less than five days until expiration. That estimate is based on data released by the CBOE Options Exchange.

The ABCs of 0DTE options

Options with zero days until expiration only exist for a single trading session. Therefore, a 0DTE option could be a longer-term option that has reached the last day of its lifecycle, or it could be a specific option that’s listed only for a single day.

For example, in April 2023, the expiration date for regular monthly equity options is April 21.

That means monthly options in April expire as of 4 p.m. EST on April 21. After the close of trading on April 20, those regularly monthly April options have essentially become 0DTE options. They exist for only a single trading session, on April 21.

The same is true of weekly options. For instance, a weekly option that starts trading on the morning of March 6, 2023 will expire at 4 p.m. EST on March 10, 2023. Those weekly options transform into 0DTE options after the close of trading on March 9.

A 0DTE option can also be an option that’s specifically listed for only a single day. Meaning the entire length of the associated contract is a single trading session. For example, since April of last year, the SPDR S&P 500 ETF Trust (SPY) has offered 0DTE options for every single day of the trading year.

Explanations of 0DTE options, like from this YouTube video provide active traders with more information on the fundamentals of trading 0DTE options.

Rapid growth in the 0DTE niche appears to be linked to growing retail participation in the broader options market. The percentage of trading volume attributable to retail investors and traders has increased dramatically since the first quarter of 2020.

The chart below highlights how smaller lots (<10 contracts per trade), which are more indicative of retail trading activity, now constitute a much larger percentage of total options trading volume.

0DTE value proposition

Growing demand for 0DTE options appears to be attributable to some of the same factors that attracted fresh participants to the options market back in 2020.

Options are unique because they are essentially leveraged short-term bets. That generally means they offer higher potential rewards and higher potential risks.

For option buyers, that can equate to outsized rewards in exchange for a minimal outlay in capital. However, such positions are generally low-probability bets—meaning they frequently result in a loss. And a multitude of tiny losses can quickly add up to a significant loss of capital.

The market selloff last year has also likely contributed to the rise in popularity of 0DTE options. Last year, upside call buyers looking for a quick payday suffered extensively, as highlighted below.

With less capital to play with in 2023, retail traders appear to have zeroed in on 0DTE options. In absolute terms, 0DTE options are cheaper than weekly and monthly options.

However, that’s not necessarily the case when analyzing the relative cost of 0DTE options.

According to new research conducted by the tastylive financial network, the overall value proposition offered by 0DTE options may be lacking, in some regards.

For example, the aforementioned research revealed that the start-of-day implied volatility for 0DTE options can be twice as high as that of their monthly equivalents. That means options buyers in the 0DTE niche are paying a steep price for such options, in relative terms.

But that doesn’t necessarily mean that selling 0DTE is an advisable strategy, either.

According to the same tastylive research, the gamma risk associated with 0DTE options can be eight times higher than that of monthly options with 30-60 days until expiration. This is attributable to the risk of large, unexpected one-day moves in the market.

Investors and traders should conduct their own analysis on the overall value proposition offered by 0DTE options to assess whether they fit one’s unique market approach, market outlook and risk profile.

To assist in that process, check out this YouTube video which focuses on some of the potential benefits and drawbacks of trading 0DTE options.

As always, monitor daily market activity via tastylive—weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastylive or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.