What You Need to Know About the Ponzi Scheme Affecting Rural China

Thousands of banking customers in the rural Chinese province of Henan have purportedly fallen victim to a wide-ranging Ponzi scheme and haven’t been able to access their accounts since April—an alarming situation that recently transformed into an attempted bank run.

The Chinese economy is the second-largest on the planet, so when cracks appear in its foundation, global investors and traders tend to pay attention.

On July 10, the cracks in China’s financial system seemingly widened, as a peaceful protest turned violent when security officers dispersed a large crowd gathered in front of a local bank. Reports indicate that the protests stem from the mismanagement (and likely theft) of funds deposited into four financial institutions operating in the Henan region.

Based on interviews conducted with attendees, it appears that the protestors gathered in the provincial capital of the region—Zhengzhou—to voice their displeasure over the handling of their savings accounts. These depositors, and many other thousands like them, have been unable to access their accounts (and associated funds) since April.

It’s becoming clear that people likely fell victim to a wide-ranging Ponzi scheme—one that was orchestrated and facilitated by key members of the business community and the provincial government in Henan province.

The situation can’t technically be defined as a bank run because the depositors in question are completely frozen out of their accounts. Bank runs traditionally occur when a large group of frenzied depositors pulls their money out of a financial institution due to fears over the organization’s ongoing solvency.

An old-fashioned bank run would have materialized in Henan province, though, had the financial institutions in question allowed withdrawals. Tragically, it appears that some of the key criminals involved in the scheme have fled the region, if not the country.

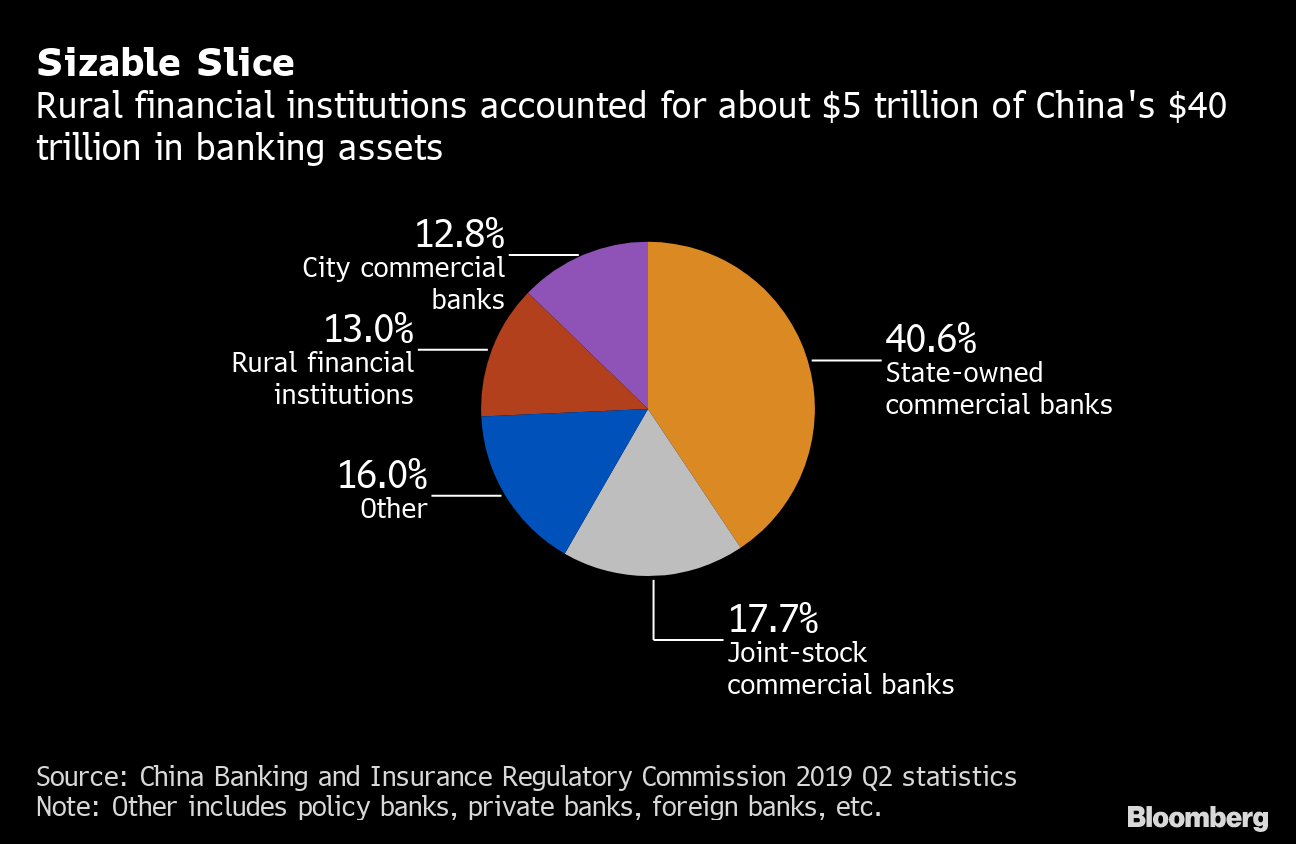

The Chinese central government has been left to pick up the pieces, which at this time includes four financial institutions and a large group of disgruntled depositors/investors. Estimates suggest that billions of dollars worth of savings may have been illegally absorbed by the criminal syndicate.

The four banks caught up in the chaos are: Yuzhou Xinminsheng Village Bank, Shangcai Huimin County Bank, Zhecheng Huanghuai Community Bank and New Oriental Country Bank of Kaifeng.

However, it appears a so-called third-party platform was used to fleece not only the depositors but also possibly the banks. Third-party platforms were banned by the Chinese government in 2021 when banks were forbidden from selling deposit products via third-party online partners.

At this time, it’s not clear why a third-party scheme was still in place in Henan province, but early reports indicate that local government officials were complicit in allowing the illegal activity.

One organization linked to the wrongdoing is the Henan New Fortune Group, which no longer has an operational website.

Based on previous statements by China’s main banking regulator, it appears that the scheme was first uncovered in May, after the April freeze went into effect for many accounts.

Back in May, the China Banking and Insurance Regulatory Commission told the state-run Xinhua News Agency, “Henan New Fortune Group, a shareholder of the four village banks, has illegally absorbed the public’s funds through internal and external collusion, the use of third-party platforms, and fund brokers.”

Tension in the region has been building for weeks, and the July 10 protest was therefore simply the culmination of those simmering frustrations. On July 11, the office of the banking regulator in Henan province issued the following statement, “[Authorities] are coming up with a plan to deal with the issue, which will be announced in the near future.”

Further light will undoubtedly be shed on this situation as more details of the Ponzi scheme are uncovered. The more worrisome scenario is that banking customers in other regions of the country were also caught up in the scheme, or something similar.

Shares of NIO Under Pressure on Reports of Accounting Irregularities

While there’s no good time for a Ponzi scheme to be uncovered, this is a particularly tough time for the Chinese financial system.

The real estate sector in China has been under intense pressure as some of the country’s largest developers have revealed precarious financial positions.

On top of that, Chinese companies listed on American exchanges have been mandated to allow American regulatory auditors access to their financial records. And due to associated legislation passed by the U.S. Congress, any Chinese-listed company that doesn’t comply with that order will be involuntarily delisted from U.S.-based exchanges at some point in 2024, if not earlier.

There are currently more than 250 Chinese companies listed on American exchanges.

Many investors and traders will recall that a slew of accounting irregularities have been discovered in Chinese-listed shares in the 21st century, with the most recent being Luckin Coffee (LKNCY).

As of June, there’s another company teetering on the brink due to purported problems with its financial statements.

On June 28, Grizzly Research published a report suggesting that the Chinese electric vehicle maker Nio Inc. (NIO) was using an “unconsolidated related party to exaggerate revenue and profitability.” Leadership at Nio has denied those claims, but did say the company was “reviewing the allegations and considering the appropriate course of action to protect the interests of all shareholders.”

Since peaking in January 2021 above $60/share, NIO shares are currently trading at around $20/share. And while NIO must be presumed innocent until proven guilty, this type of exposure isn’t exactly ideal when it comes to the Chinese delisting story.

American regulators have been pressing hard for strict enforcement of the auditing mandate, which means the timing of these allegations could provide that initiative with fresh momentum.

Chinese companies have been trading on U.S. exchanges for many years. But it was recently discovered that Chinese companies have been exploiting a loophole in the system that allows them to sidestep the stringent auditing standards typically required of overseas listings.

That shell game officially came to a close in 2020 when Congress passed the Holding Foreign Companies Accountable Act (HFCAA). Under the new law, all foreign companies listed on American exchanges will be delisted if they fail to turn over audit results for three consecutive years.

Chinese companies are especially vulnerable to this new law because the Chinese government often serves as a major roadblock when it comes to the release of sensitive information to foreign agencies.

As a result, a slew of Chinese delistings could materialize in 2024, if not sooner. Presently, there are an estimated 250 Chinese companies listed on U.S. exchanges, which together represent more than $1 trillion in combined market capitalization.

Investors and traders with existing positions in such companies, or considering new positions, may therefore want to tread cautiously.

To learn more about stock delistings, review this recent installment of Options Trading Concepts Live on the tastytrade financial network. For more context on binary events—like a mass involuntary delisting of Chinese shares—check out this episode of Options Jive.

To follow everything moving the financial markets on a daily basis, tune into TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.