Luckbox leans in with Ed Yardeni on the Measuring Misery

Yardeni, an investment industry veteran known as the “Wall Street Seer,” has held positions with the Federal Reserve Bank of New York, the Fed Board of Governors and the U.S. Treasury Department. He served as the chief investment strategist at Prudential Equity Group and Deutsche Bank and as chief economist at Prudential-Bache Securities and EF Hutton. He’s currently president of Yardeni Research and has written seven books on the markets and the economy. His latest, In Praise of Profits, is profiled here.

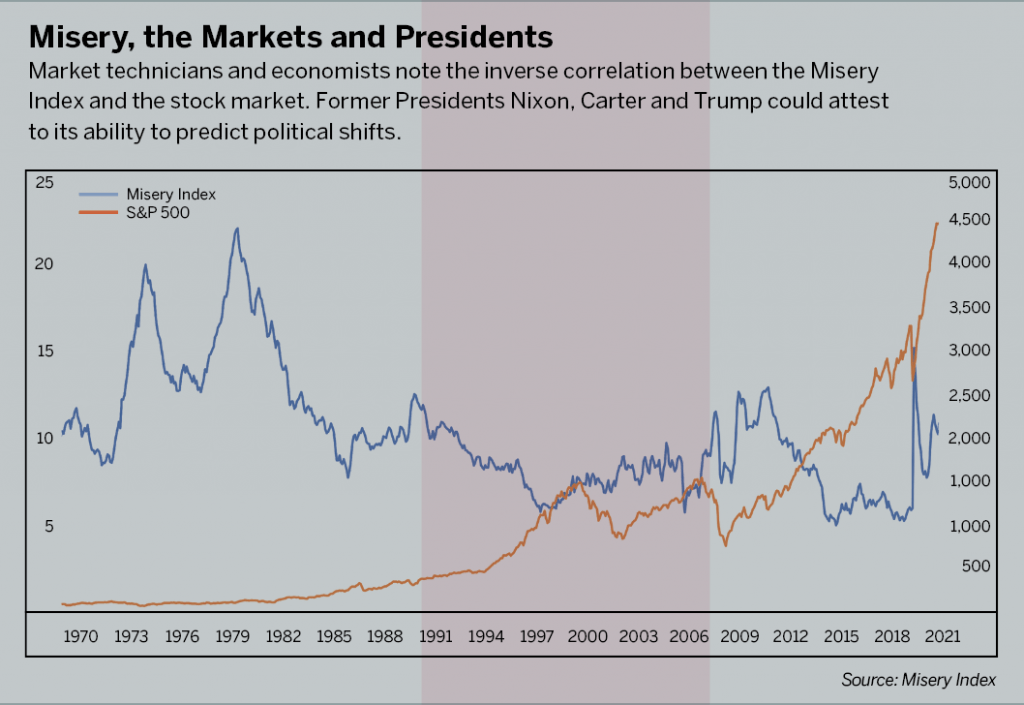

The Misery Index, one of the indicators that helps Yardeni analyze the economy, combines unemployment and inflation rates. Higher readings indicate increased economic and social woes.

Just before press time, Luckbox leaned in with Yardeni to discuss October’s inflation numbers and the latest Misery Index reading.

You’ve observed the Misery Index for decades. What is it telling you right now?

It’s clearly flashing orange. It’s always better to see the Misery Index near its historical lows. And now, we’re seeing wages going up, costs going up, supply disruptions and, as a result, the CPI inflation rate has been moving higher. The inflation rate is a very regressive tax on everybody. It’s important to see wage increases in nominal terms, but if they’re eroded by rising inflation, it doesn’t do anybody any good—all you get is a wage-price spiral.

For the stock market, a falling unemployment rate should indicate a very solid improvement in earnings. On the other hand, a rising inflation rate tends to be negative for the valuation multiple. So now we may see the market challenged by concerns about inflation because the Fed cannot continue to maintain ultra-easy monetary policy when inflation is clearly accelerating.

If the Misery Index is flashing orange, what would cause it to flash red?

If it begins to appear that the inflation we are seeing here is similar to what happened in the 1970s instead of just a passing problem related to the pandemic. But we have had experiences where soaring energy prices caused recessions, so I would be concerned about that possibility. We clearly have seen fossil fuel prices increase dramatically in China and Europe and even in the United States. If prices continue to go higher, we could get a recession, which then would cause a bear market.

Are you surprised that the Fed’s prior tapering announcements didn’t precipitate a market adjustment?

Not really. The Fed has provided so much liquidity in the system that even when they start to taper they’re still buying bonds—just at a slower pace. They’re still adding liquidity to the system, and they’ve added so much liquidity since the start of the pandemic. There has never been so much liquidity. So much of it is sitting in bank deposits earning absolutely nothing. The Fed is only talking about adding rum punch into the punch bowl at a slower pace. They’re not taking the punch bowl away.

Do you view the Consumer Price Index (CPI) as an adequate and appropriate measurement of inflation?

Do you think it overstates or understates inflation?

Considering all the components of the CPI, the one that has the most immediate impact on whether we’re more or less miserable is the price of gasoline. We all pass a gas station, one way or the other, and we all fill up our tanks and see what that price is doing.

October’s 6.2% CPI number is the highest reading in 31 years. What does it tell us?

There was a morsel of good news. The year-over-year comparisons saw base-effect slowing in some segments such as airline fares. But rent costs and new car prices picked up substantially. The bottom line is that October CPI confirms that inflation isn’t transitory. It’s persistent.

What else does the recent increase in the Misery Index suggest?

Well, when the Misery Index is rising, political incumbents become more vulnerable. This could have a tremendous impact on who’s in the White House. Jimmy Carter arguably lost largely because inflation was viewed as out of control. If there is no change come midterms, the Democrats are vulnerable to losing their majority in both houses. And if Biden runs again he’s vulnerable to losing to a Republican.

Assuming energy prices do not move materially higher, does the market continue to advance?

Yes, I believe so. I’ve got 4,800 [for the S&P 500] by the end of this year, 5,200 by the end of 2022 and 5,800 by the end of 2023.