What You Need to Know About the Latest Inflation Report

Parallels between the current bout of inflation and the one observed in the late 1940s suggest that record inflation could normalize at some point in H2 2023 or H1 2024

On December 13, the U.S. government released its latest report on inflation, which summarized inflationary data for the month of November.

The report indicated that inflation clocked in at roughly 7.1% last month. That means over the last 12 months—from November 2021 to November 2022—prices rose on average at a rate of 7.1%, as calculated by the Consumer Price Index (CPI).

That figure compares somewhat favorably to the October inflation report, which saw a higher level of annual inflation—7.7%. Together, these two reports indicate that inflation has cooled slightly as compared to the summer, when CPI peaked above 9%.

A downtick in inflation is definitely good news, but it’s important to recognize that inflation is still running extremely hot by historical standards. As part of its so-called “dual mandate” on employment and inflation, the Federal Reserve targets an annual inflation rate of 2% in the U.S. economy.

With inflation still running well above 7%, it’s easy to see why anxieties over record-high inflation remain high. And why the Federal Reserve is so hellbent on reigning it in.

With that in mind, it’s worth examining how long record-high levels of inflation could persist into the future.

When will inflation drop back to “normal” levels?

One complication with this type of analysis is that inflation hasn’t been this high in the United States since the early 1980s. And prior to that, the other significant period of high inflation was observed just after World War II—in the late 1940s.

From a glass-half-full perspective, that means the U.S. economy has been well-buffered from extreme inflation for many years. But it also makes it difficult to forecast how long inflation could persist these days, because of the difficulty in comparing economic conditions across eras.

In the 1970s, inflation remained stubbornly high for many years, with most measurements indicating that it persisted for almost a decade. Back then, the country was facing an employment crisis—in 1975 the unemployment rate peaked at about 9%.

Moreover, the world economy was grappling with the fall of the Bretton Woods system back in the 1970s, which effectively terminated the convertibility of fiat currencies into gold. This period in U.S. history is so infamous it is often referred to as the Great Inflation, much like the 2008-2009 period is referred to as the Great Recession.

Today, the U.S. employment rate is hovering around 3.7%, which is toward the lower end of the metric’s historical range.

Unfortunately, the U.S. economy has been battling with the repercussions of the COVID-19 pandemic. And from that perspective, the current bout of inflation may be more comparable to the inflationary conditions observed during the late 1940s, as opposed to the 1970s and early 1980s.

After World War II, the baby boom catalyzed a huge spike in demand for durable goods. In some ways, this period was similar to the early stages of the COVID-19 pandemic, when consumer demand for durable goods surged, alongside a decline in demand for services—mostly due to rolling lockdowns and remote working/learning.

Already beset by the pandemic, global manufacturers were overwhelmed by a surge in demand, and couldn’t ramp up production quick enough to satisfy the needs of the market. As supplies dwindled, prices spiked—catalyzing the rapid appreciation in prices that consumers are still dealing with today.

Importantly, however, demand for durable goods has declined in recent months, while demand for services has risen. And as the supply chain has loosened, some of the bottlenecks in the system that were fueling inflation have dissipated.

Last month, the U.S. economy added 263,000 new jobs, with many of the gains coming from service-related industries such as education, health care and hospitality. This data provides evidence that the economy may be “normalizing,” as demand for services catches up, and demand for durable goods reverts to pre-pandemic levels.

At present, Federal Reserve projections indicate that inflation could revert to normal levels by the end of 2023. And using the 1940s as a blueprint, that may be a reasonable estimate.

In the wake of World War II, a flood of pent-up demand was unleashed upon the economy, which saw a large group of motivated consumers chasing a limited amount of goods. That’s similar to what was observed during the onset of the COVID-19 pandemic, when consumer demand for electronics, furniture, appliances and recreational goods all skyrocketed.

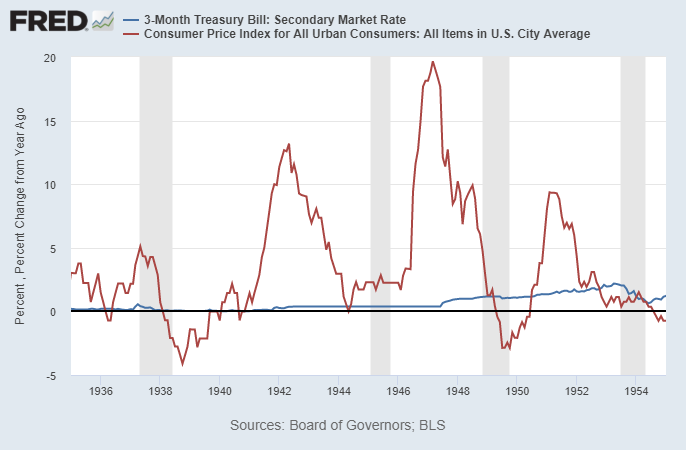

After World War II ended, inflation peaked at roughly 20% in 1947, and then proceeded to moderate. By the end of 1948, inflation had mostly normalized—as demand subsided, and manufacturers bulked up available supply. That downdraft in inflation (as illustrated through CPI) is highlighted below.

These days, it’s reasonable to think that inflation might follow a similar path. If inflation truly peaked during the summer of 2022 at just over 9%, it’s possible CPI could return to normal by the second half of 2023, or early 2024. At least that’s what one might surmise based on the historical record.

On the other hand, it’s a bit harder to envision the U.S. economy entering a second Great Inflation—another ten years of rampant inflation—because the economic conditions and headwinds observed in 2022 simply don’t match those of the 1970s.

Of course, the future is unknown, and other challenges could arise that cause disruptions within the global supply chain. Under that scenario, inflationary pressures could persist for longer than the Federal Reserve currently anticipates.

For more background on inflation, and its impact on the global financial markets, check out this recent installment of Truth or Skepticism featuring tastylive co-host Tom Sosnoff and longtime market pundit Dylan Ratigan.

To follow everything moving the markets during the remainder of 2022 and beyond, monitor tastylive, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastylive or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.