Nvidia’s Earnings Were Great, But …

Nvidia (NVDA) reported strong earnings in Q1, but results from other parts of the AI sector suggest the industry may be facing increased headwinds.

- Q1 earnings revealed that not all AI-focused companies are thriving, with some stocks experiencing significant post-earnings declines.

- Companies such as Dell, MongoDB, Salesforce and UiPath all saw their shares fall sharply after reporting underwhelming earnings, particularly in terms of AI potential.

- Current valuations in the stock market are based on a continuation of strong earnings growth in 2024 and may therefore end up being overly optimistic.

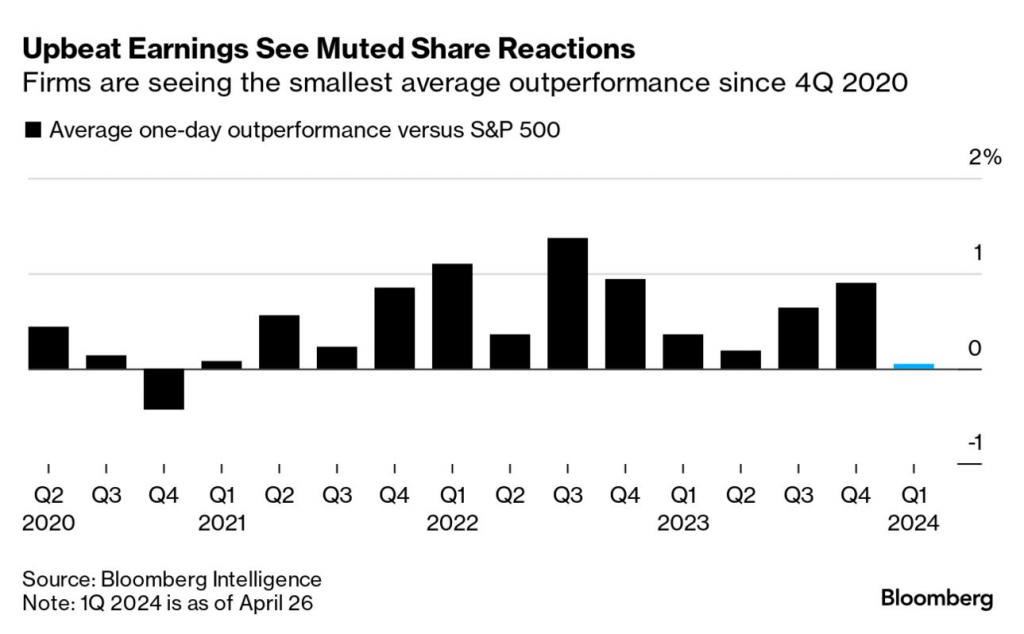

Investor enthusiasm for the AI sector has helped drive stock market gains in early 2024. However, several prominent companies that have invested heavily in AI experienced sharp corrections in their stock prices following their Q1 earnings announcements.

That wasn’t the case for Nvidia (NVDA), which reported strong quarterly earnings results on May 22. That said, even Nvidia’s forward guidance wasn’t as strong as some might have hoped. On a quarter-over-quarter basis, Nvidia expects revenue to grow by just 8% from Q1 of 2024 to Q2 of 2024. That’s well below the 18% quarter-over-quarter growth rate observed from Q4 of last year to Q1 of this year.

Looking beyond Nvidia, companies such as Dell Technologies (DELL), MongoDB (MDB), Salesforce (CRM), Super Micro Computer (SMCI) and UiPath (PATH) all suffered downturns after earnings, arguably because investor expectations didn’t align with actual performance.

Commenting on potential vulnerabilities in the AI narrative, Sam Stovall—Chief Investment Strategist at CFRA—recently wrote, “Like a thin film of ice on a pond in early winter, the support from Artificial Intelligence (AI) has cracked under the growing weight of concerns about the Federal Reserve and the direction of monetary policy.”

For a deeper look into the dynamics, we highlighted additional details below.

Dell

Dell shares have been on a tear in 2024, appreciating by nearly 80% during the first five months of 2024. But Dell’s stock pulled back sharply after its earnings report due to investor apprehension associated with its Q1 report. Dell released earnings after the close of trading on May 30. The very next day, shares corrected by 18%.

On May 30, Dell reported that Q1 revenues were above analyst expectations, while Q1 profitability was mostly in line with expectations. For example, actual Q1 revenues were $22.2 billion, which was above the $21.64 billion estimate. On the other hand, earnings per share (EPS) were $1.27, which was slightly above the $1.26 forecast.

Despite these robust figures, deeper insights into the earnings report revealed concerns, particularly around the profitability of its AI-focused offerings. Notably, while revenue for Dell’s Infrastructure Solutions Group—which includes AI products—grew by 22% to $9.2 billion, the profit margins from these services were minimal.

Analysts at Bernstein recently highlighted this weakness, stating that the operating margin on Dell’s AI servers was “near zero.” As such, Bernstein analysts felt the overall report was underwhelming, writing in a note to clients: “On net, relative to very high expectations, Dell’s Q1 25 results were disappointing.”

MongoDB

Like Dell, MongoDB reported Q1 earnings on May 30. MongoDB is a software specialist that focuses primarily on “NoSQL” databases.

NoSQL databases are unique, because they don’t use SQL for queries, and instead rely upon other programming languages and constructs. MongoDB is a leader in NoSQL space and has traditionally grown sales at a rapid rate.

In Q1, the company reported that sales had grown at a healthy rate of 22%. For most companies, that level of growth would be viewed as a positive. But for MongoDB, that was the slowest rate of year-over-year quarterly sales growth in some time, which helps explain why MongoDB shares sold off sharply in the wake of the report.

According to management, generative AI won’t contribute to a meaningful increase in revenues during the current fiscal year. In response to that sobering news, MongoDB shares dropped by about 24%, pushing the stock down from over $300 per share to $236 per share. Shares of MDB are now down about 40% on the year.

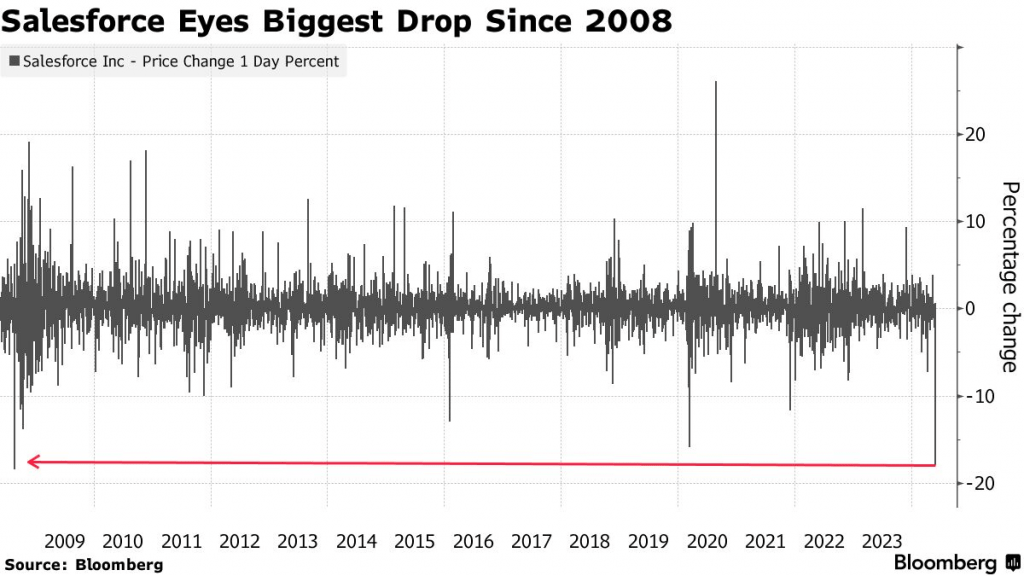

Salesforce

Salesforce (CRM) is a mainstay in the technology sector and has consistently outperformed earnings and revenue forecasts. However, the first quarter of 2024 brought unexpected challenges for the company.

On May 29, Salesforce reported Q1 revenues of $9.13 billion, narrowly missing analyst estimates and marking the first revenue shortfall since 2006, as noted by CNBC. Additionally, the company’s Q2 earnings forecast fell short of Wall Street expectations, guiding earnings of $2.34 – $2.36 per share, as compared to the anticipated $2.40 per share.

Despite an 11% increase in Q1 revenues, the slower growth and cautious outlook led to a significant 20% drop in Salesforce shares on May 30, the sharpest decline in nearly two decades (illustrated below). This reaction shows the company’s AI potential underwhelmed investors because it has not fully materialized in financial performance.

Analysts at Citibank attribute the lackluster results to severe macroeconomic headwinds, which aren’t conducive to growth. Currently, Salesforce’s stock is trading at approximately $235 per share, about 26% below its 52-week high of around $319/share, reflecting the market’s disappointment with both the immediate financial results, as well as the delayed realization of the company’s AI-focused growth strategies.

Super Micro Computer

Along with Nvidia, Super Micro Computer (dba Supermicro) has been a poster child of the recent AI revolution. Over the last 52 weeks, Supermicro shares have surged by approximately 245%, reflecting the company’s critical role in the expanding AI technology sector.

However, despite this impressive growth, Supermicro’s stock is currently trading significantly below its 52-week high of around $1,230 per share and now trades at approximately $785 per share, marking a 36% decline. This drop primarily stems from the company’s April 30 earnings report which, while not disastrous, did not meet the lofty expectations that fueled the stock’s recent rally.

During the first three months of the year, Supermicro reported earnings per share of $6.65, surpassing analysts’ expectations of $5.78/share. However, the company fell short on revenue, bringing in $3.85 billion against the forecasted $3.95 billion. The market’s reaction was lukewarm, with Investor’s Business Daily characterizing the report as “mixed” and noting that sales “came in light.”

Despite these challenges, Supermicro offered strong guidance for the second quarter, predicting revenues of around $5.3 billion and adjusted earnings of $8.02 per share, exceeding analyst expectations of $4.86 billion and $7.13 per share, respectively.

Supermicro’s forward guidance appears to be underpinned by its core ability to deliver high performance, through the delivery of scalable server solutions that are optimized for AI applications. The company’s servers are uniquely suited to handle the intense computational demands and cooling requirements of GPUs, which are crucial for both AI training and inference.

If Supermicro can exceed its optimistic Q2 guidance, the company’s shares could easily rebound, and trend back toward 52-week highs.

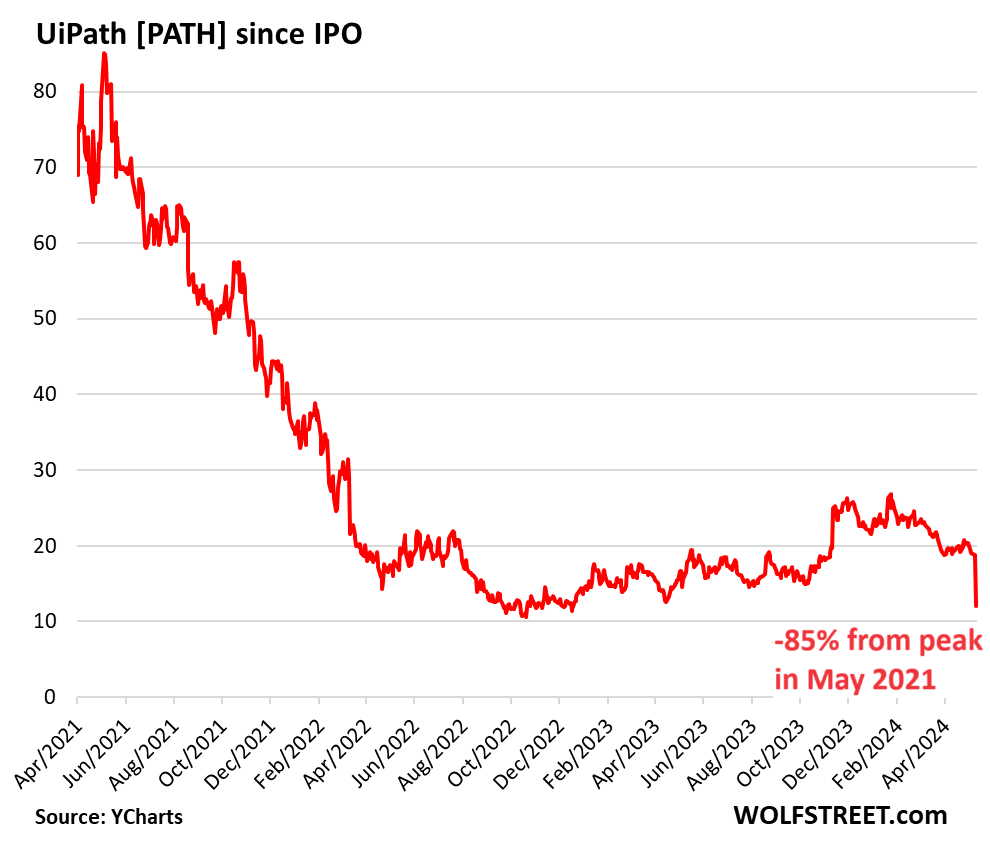

UiPath

One of the companies hardest hit by underwhelming Q2 earnings guidance was UiPath (PATH). On May 29, the company reported Q1 earnings that comfortably beat expectations.

However, UiPath experienced unforeseen headwinds and lowered its financial guidance for the full year. Not long ago, management at UiPath had indicated that revenues would rise by about 19% in 2024. But the company amended those figures lower on its Q1 conference call. UiPath now expects revenue growth of closer to 7% to 8% for the year.

On top of the above, CEO Rob Enslin will be stepping aside. In his place, the company’s chief innovation officer, Daniel Dines, will take the reins. This was surprising because Enslin hadn’t been in the position for long, indicating that leadership at UiPath believed an urgent change was needed at the top.

Year-to-date, shares in UiPath are now down about 50%, dropping from around $24 per share down to $12 per share. However, looking back further in UiPath’s history, the stock is now down about 85% from its 2021 peak, as illustrated below.

UiPath uses an interesting business model because it sits at the crossroads of robotics and artificial intelligence. UiPath develops digital (e.g. virtual) robots that assist with the automation of business processes. This segment is known as robotic process automation (RPA), which falls under the broader umbrella of enterprise automation.

In the case of UiPath, the company deploys digital “bots” to assist with these automation efforts. And AI advancements should help enhance the capabilities of these bots, enabling them to handle increasingly complex tasks with greater accuracy and minimal human intervention. This evolution could significantly boost operational efficiencies and drive transformative changes across the business world, positioning UiPath as a potential leader in this niche.

Shares of UiPath currently trade at an 80% discount to its IPO value, suggesting that investors and traders bullish on the prospects of UiPath may want to consider adding to existing positions—or deploying new ones—at this time.

Final takeaways

The recent earnings season has shown that not all AI-focused companies are thriving, suggesting that cracks may be forming in the once “bulletproof” AI narrative that has driven much of the recent bull run in the stock market.

Alongside Dell, UiPath, and others, companies like Snowflake (SNOW) and Workday (WDAY) also experienced declines in their valuations after earnings.

Weakness in these key tech stocks hints that the bullish trends in the major market indices may not fully reflect overall sentiment. And with the AI narrative playing a significant role in recent market gains, investors may need to be more cautious.

Along those lines, strong growth in corporate earnings underpins current valuations in the stock market. However, the information and data above suggest that many AI and technology companies could struggle to meet those optimistic projections.

The disconnect between market expectations and corporate performance could lead to additional market volatility as valuations realign with underlying economic realities. And the potential for increased volatility is particularly acute given that a presidential election is on the horizon.

Andrew Prochnow has more than 15 years of experience trading the global financial markets, including 10 years as a professional options trader. Andrew is a frequent contributor of Luckbox Magazine.

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.