SPACs’ Bad Rap

If you in the SPAC game you know what I’m talking about

We sick of IPOs day one lockin’ us out

My man Randy first told me DraftKings would go public

It’s mergin’ wit’ a SPAC and the market gonna love it

I’m like a SPAC, what’s the hell’s that?

You get in on the ground floor

It paid big, so I searched and then I found more

—SPAC Dream, Cassius Cuvee (feat. Mags Lionne), 2021

In today’s frenzied finance world of YOLO trades, trendy tendies and NFTs, your bubble radar shouldn’t start blinking until some rapper spits rhymes about special-purpose acquisition companies.

Well, drop the mic and call us paper hands.

In 2019, entrepreneur Richard Branson dusted off the 20-year-old SPAC structure to introduce Virgin Galactic to space-minded investors in a spectacular initial public offering. Since then, the SPAC comeback has ignited a firestorm of institutional and retail investing.

Meanwhile, financial journalists are using the SPAC phenomenon as a vehicle, too. Reporters assert their own toughness and make a showy display of their skepticism by lambasting the very idea of SPACs. Their thinking goes like this: Some SPACs have traded at unreasonable valuations, SPAC sponsors charge high fees, and entertainers and athletes serve as mere shills for SPACs—therefore, SPACs must be bad!

But it’s not that simple, as we’re reminded by our conversation with attorney Doug Ellenoff. He’s a partner in the law firm that’s overseen more SPAC deals than any other since the structure began coming on strong again in 2019. SPACs have become the go-to market vehicle for strong private companies coming out of venture capital and for private equity portfolios. That’s because they offer a faster, cheaper and less restrictive path to funding than traditional, more-regulated initial public offerings or direct listings.

When Virgin Galactic burst open the door, the company’s success was duly noted at private companies that sought more expansion capital and by strong operating teams seeking their next platform. Not withstanding the naysayers, SPACs are supplying hundreds of transformational businesses with billions of dollars to become public.

But any overheated “next new thing” will invariably cool off. Investors will become more discriminating, fees will come down and the frequency of new issuance will slow. In the meantime, some SPACs appear overvalued, some show promise and a few are brimming with explosive potential. That’s why this issue is packed with perspectives. But discerning readers will burrow through the mountain of information and emerge wiser on the other side.

The bottom line is SPACs are not going anywhere—they’re here to stay. And while SPACs are having their moment, investors can have their moment, too.

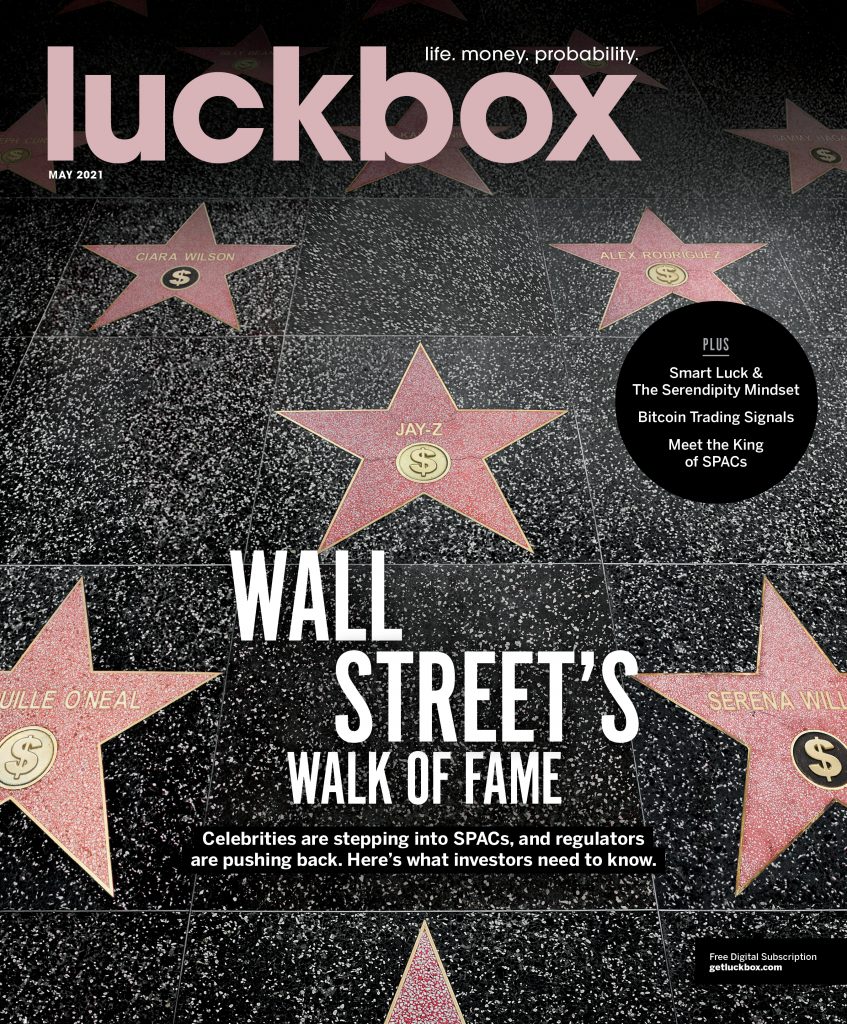

Instead of speculating on a star management team to negotiate the acquisition of an undervalued private asset, Garrett Baldwin, Luckbox editor-at-large, has a better idea. He shares the specifics behind a consistently profitable, Treasury-backed SPAC arbitrage tactic that savvy, yield-seeking institutional investors are using to lock in profits. They simply buy SPACs that trade at meaningful discounts to their trust redemption values.

Like all great high-probability arbitrage plays, these trades will not be around forever. In time, the bubble babble will pass, but SPACs will continue to deliver on their potential to raise funds for innovative but cash-hungry companies that provide good, sustainable jobs and solidly lucrative investment opportunities.

Ed McKinley, Editor in Chief

Jeff Joseph, Editorial Director

Click here to subscribe for FREE to the digital edition of Luckbox magazine.