Cooking Up an NFT

Non-fungible tokens, or NFTs, have garnered a lot of attention in recent months. In the first half of 2021 alone more than $2.5 billion in NFT sales volume has exchanged hands, up from $13.7 million in the first half of 2020.

So, what gives? What are NFTs, and how does one create, buy or sell them?

Put simply, NFTs are assets—predominantly digital ones—that are minted and stored on a blockchain, effectively making them unique and scarce. Only one person can claim ownership of any given NFT, and all ownership records are public.

They come in various forms, from photos and videos to music and video games to just about anything in-between—including tokenized real-world assets. One way to think of an NFT is as a digitally stored collectible.

Intrigued by the prospect of the burgeoning NFT marketplace, the editors at Luckbox decided to make one. What follows is the recipe used to create that NFT, as well as a guide for adding NFTs to any interested investor’s portfolio. — Mike Reddy

Preparation Time <One day

Yield One NFT

Ingredients

1 tangible or digital asset to turn into an NFT

1 ethereum cryptocurrency wallet

1 ethereum-powered NFT marketplace account to list the NFT $25-$80 (estimated) worth of ethereum to cover fees

Step 1

Decide what to make into an NFT

The first step in making an NFT is deciding what to turn into one. Artwork is among the most popular categories of NFTs on marketplaces, but other categories include music, domain names, collectibles and trading cards.

While NFTs exist predominantly in digital form, they can be linked to physical assets as well. In those cases, the owner of the NFT can redeem it for the delivery of the physical goods.

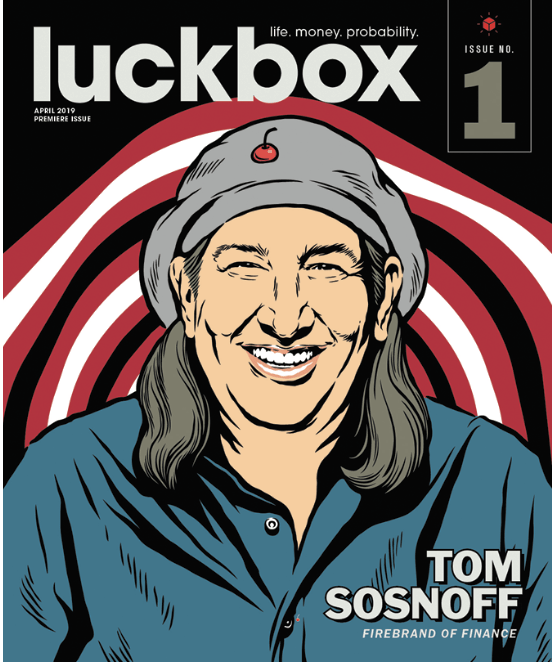

Luckbox created an alternative digital rendering of its debut April 2019 issue cover for its NFT.

Step 2

Decide which blockchain is right for the NFT

Different blockchains have different token standards, require different crypto wallets and power different NFT marketplaces.

Ethereum is by far the most popular blockchain for NFTs, but others, such as Tron and Tezos, have also been gaining traction.

Luckbox opted for the ethereum blockchain for its NFT because of its size, popularity and familiarity among cryptocurrency traders.

Step 3

Make an ethereum wallet and an NFT marketplace account

Cryptocurrency is essential for buying or listing NFTs, so that necessitates having a cryptocurrency wallet—

or a digital place to store some crypto.

Because Luckbox opted to mint its NFT with the ethereum blockchain, an ethereum wallet was needed. Worth noting, not all NFT marketplaces support the same blockchains, so Luckbox needed to find one based in ethereum.

OpenSea, Rarible and Mintable are among the most popular ethereum-powered NFT marketplaces—OpenSea being the largest. For that reason, Luckbox decided to go with OpenSea, which offers seamless integration with the MetaMask ethereum wallet and web browser extension.

Step 4

Mint and list the NFT on the marketplace

On OpenSea, minting an NFT is as simple as clicking the “Create” button. Doing so will prompt linking the MetaMask wallet to the OpenSea account. Then, upload the asset and create a description for it.

Once created, list the NFT on the marketplace. NFTs can be sold on OpenSea for a set price, in an auction or as part of a bundle of other assets. Listing the NFT may incur a network congestion fee, known as a “gas” fee, which will vary at different times.

When Luckbox listed its NFT on OpenSea, the gas fee was roughly $60.

Step 5

Finished! Now wait for offers

While waiting, explore other listings on the marketplace. Placing bids for NFTs, or buying them outright, should feel familiar to anyone who has shopped on eBay—with the distinction of using cryptocurrency.