How Sky-high Corporate Profit Margins Are Exacerbating Record Inflation

The results from Q3 earnings season reveals that corporate profit margins are still high—an indication that consumers in the U.S. have been shouldering a significant portion of the inflation burden in 2022

Halloween may be over, but the specter of inflation still haunts the world economy.

On Nov. 3, the U.S. Federal Reserve took another shot at exorcising the inflation demon, when the U.S. central bank raised benchmark interest rates another 0.75%. Hopefully, the latest rate hike will perform as intended.

However, one could argue that U.S. central bankers, and many of their global counterparts, are using the wrong tool for the job. One could also argue that if not for sky-high corporate profit margins, they may not have needed to act so aggressively in the first place.

Newly raised interest rates should help ultimately cool inflation, but in this case, the medicine (i.e. higher rates) could end up being just as toxic as the disease itself (i.e. red-hot inflation).

Elevated interest rates increase the cost of borrowing for businesses and consumers. To compensate for increased financing costs, (i.e. corporate loan payments, mortgage payments, car payments, etc.) businesses/consumers tend to cut back on other parts of their budgets. That all has a direct effect on the underlying economy, as fewer dollars get pumped into circulation.

Inflation is typically characterized by too many dollars chasing a limited amount of goods and services. So with fewer dollars chasing those same goods and services, prices are expected to stagnate, or possibly even reverse course, as the upward pressure on prices dissipates.

Unfortunately, it’s no simple task to exert precise control over the economy, especially using a blunt tool like interest rates. By raising rates so quickly over such a short period of time, the U.S. central bank could soon find itself facing another problem—negative growth in the American economy (AKA a recession).

That’s why hiking rates to fight inflation represents a double-edged sword.

Record corporate profit margins have exacerbated inflationary pressures

One key statistic that’s been underreported in financial media is the fact that corporate profit margins are currently hovering at record levels in the U.S.

According to FactSet, the blended net profit margin for S&P 500 companies reporting earnings during Q3 so far has been about 12%. That’s down from 12.9% a year ago, but still above the five-year average of 11.3%.

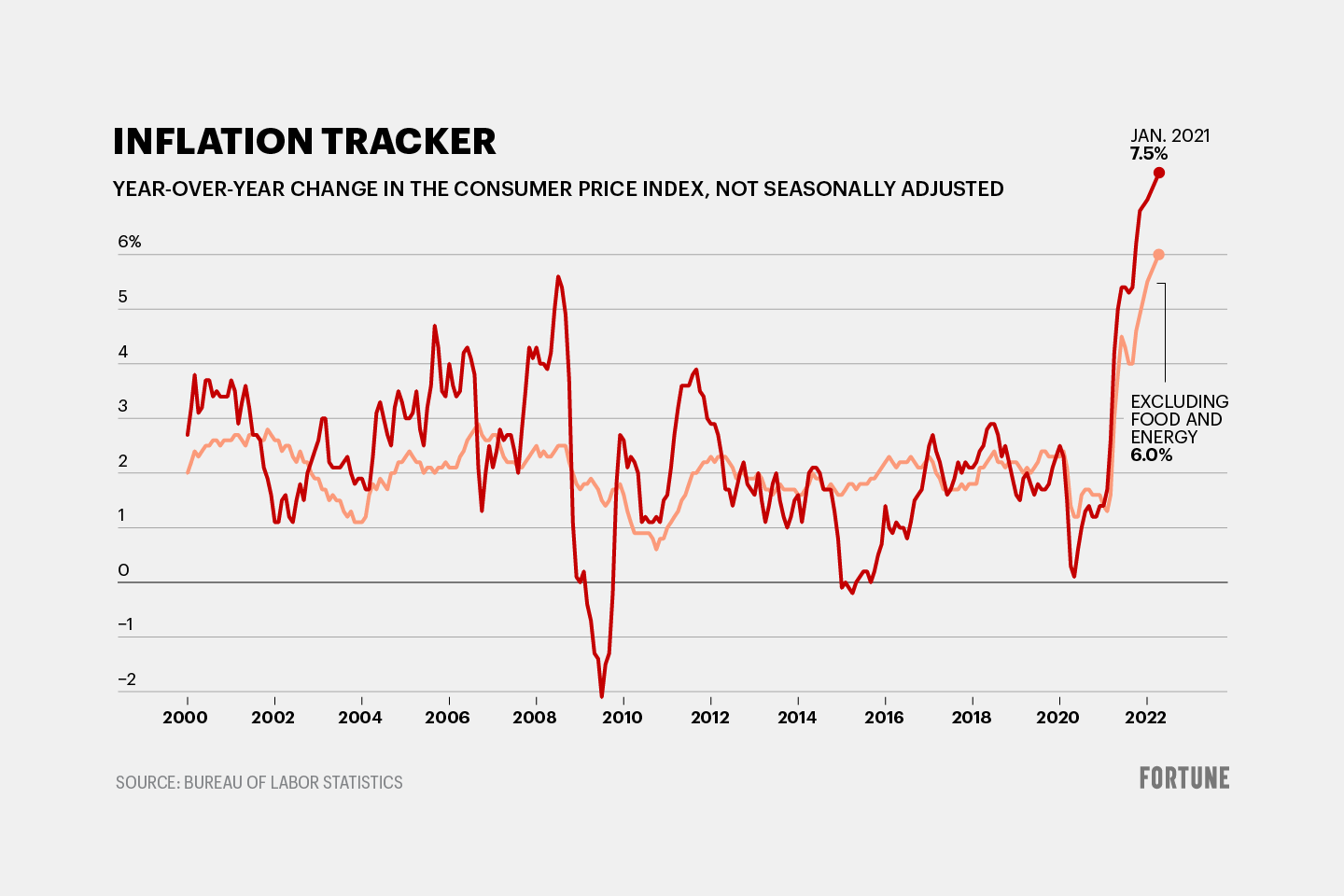

The above chart illustrates that even amidst record inflation, the U.S. corporate sector is still booking record profit margins. Ostensibly, that means businesses are passing on rising costs to their customers, instead of absorbing those costs themselves.

In a capitalist system, that could be the nature of the beast. Business managers are tasked with increasing shareholder value, and that’s typically accomplished by maximizing profitability. That’s the reality of the system, and it won’t likely change anytime soon.

However, one has to at least recognize that this aspect of the system has negative consequences. In the last two years, the drive for greater profitability has unfortunately served to exacerbate the negative impact of inflation.

Sadly, the remedy to the current situation won’t likely be easy to endure either.

Facing elevated borrowing costs, businesses and consumers will undoubtedly be forced to cut other expenditures from their monthly/annual budgets. In turn, the U.S. economy will contract. Ultimately, this will force the corporate sector to cut jobs—the true kryptonite for the economy.

All told, these forces should also put pressure on corporate profit margins, pushing them back toward their long-term average.

Regrettably, the forthcoming pain could have been avoided—at least in part—if consumers hadn’t been forced to shoulder such a large degree of the inflation burden in the wake of the COVID-19 pandemic. This reality was echoed recently by a U.S. House Committee on Oversight and Reform, which noted “certain corporations are using the cover of inflation to raise prices excessively, resulting in record prices and profit margins.”

In a few days, the U.S. government will release its latest report on inflation. That report will summarize inflationary conditions in the U.S. during the month of October, and is scheduled for release on Nov. 10.

To learn more about trading quarterly earnings, check out this installment of Best Practices on the tastytrade financial network. For daily updates on everything moving the markets—including the next inflation report—monitor TASTYTRADE LIVE, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.