Trading Implied and Realized Volatility in a Post-pandemic World

The stock market has been moving a lot since the start of the COVID-19 pandemic, but new tastylive research shows that implied volatility has consistently outpaced realized volatility since the start of 2020

The options market isn’t perfect, but it is known for its efficiency.

Movement in the market, or expected movement, is central to the pricing of options. That’s why most options traders think in terms of implied volatility—the expected future movement that’s implied by the price of a given option in the market—instead of the dollars and cents value of an option.

Over the long haul, the premium built into an options value tends to overstate the actual movement observed in the associated underlying. For this reason, short options strategies have historically outperformed long options strategies.

This is the same principle observed in the insurance market, where insurance premiums are robust enough to not only cover insured losses, but also a steady stream of profits.

However, during the last several years, the stock market has been moving more than usual. Does that mean that actual volatility in the stock market has outpaced implied volatility (i.e. the market’s expectation for volatility)?

According to new research conducted by the tastylive financial network, the answer to that question is a resounding no.

In order to analyze the relative overstatement in options prices during the last several years, the tastylive network reviewed two specific sets of data.

1. Implied volatility (IV) represents the current market price for volatility, or the fair value of volatility, based on the market’s expectation for future movement in a given underlying over a defined period of time.

2. Historical volatility (HV), on the other hand, is the actual movement that occurs in a given underlying over that same period. Historical volatility may also be referred to as “realized volatility” or “actual volatility.”

When implied volatility outpaces historical volatility, the difference between the two should be a positive number. For example, if implied volatility in hypothetical stock XYZ is 20, and historical volatility in XYZ is 15, then the spread would be +5 (20 – 15 = 5). That spread, or overstatement in options premium, represents potential profits for options sellers.

In order to evaluate the relative overstatement of implied volatility over the last several years, tastylive reviewed both implied volatility and historical volatility going back to the start of 2020. This exercise was conducted in 28 popular ETFs, including the SPDR S&P 500 ETF Trust (SPY), which is an index ETF representing the S&P 500.

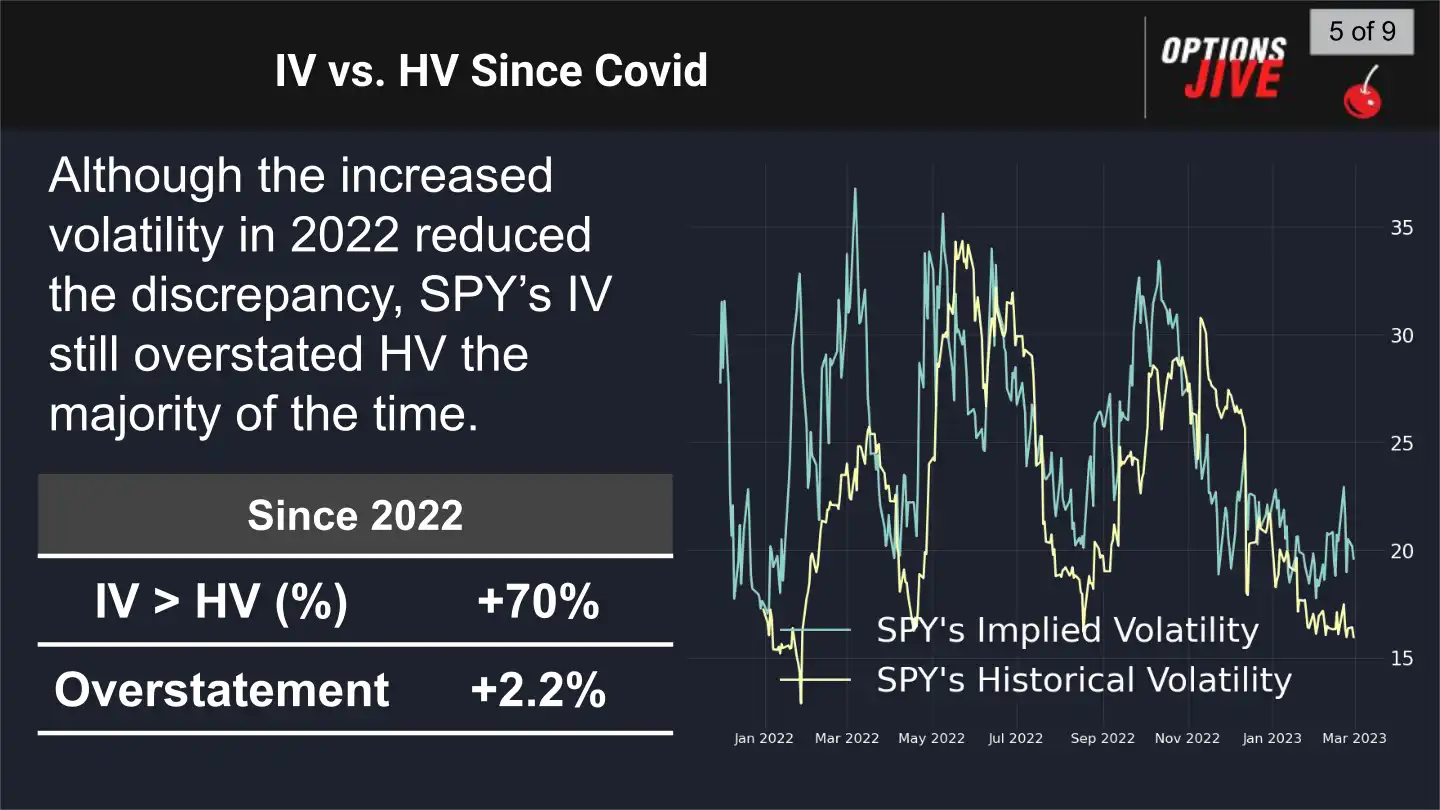

Looking at the market as a whole (i.e. the S&P 500), tastylive found that implied volatility consistently overstated realized volatility during that period.

The only difference was that in 2022, the degree of overstatement shrunk as compared to the degree of overstatement observed during the entire window of time (2020 to present). The summarized findings from this analysis are highlighted below.

The above shows that options premiums have continued to overstate actual movement in SPY since the start of 2020, despite the predominant feeling that the market is moving more than usual.

The reasoning behind this continued overstatement is attributable to the efficiency of the options market. As stocks start moving more, participants in the options market (intentionally or unintentionally) start building a larger buffer into the price of the options.

That means on average, short options strategies have outperformed long options strategies during the last few years.

That said, the degree of overstatement has varied widely across different stocks, and different sectors of the market during that period. If one were to look only at the biggest movers in the market, then one might find that actual volatility surpassed implied volatility, but only for short periods.

In order to better understand how different sectors of the market performed—in terms of realized volatility vs. implied volatility—the tastylive financial network also performed the analysis on 28 popular ETFs representing different sectors of the overall market.

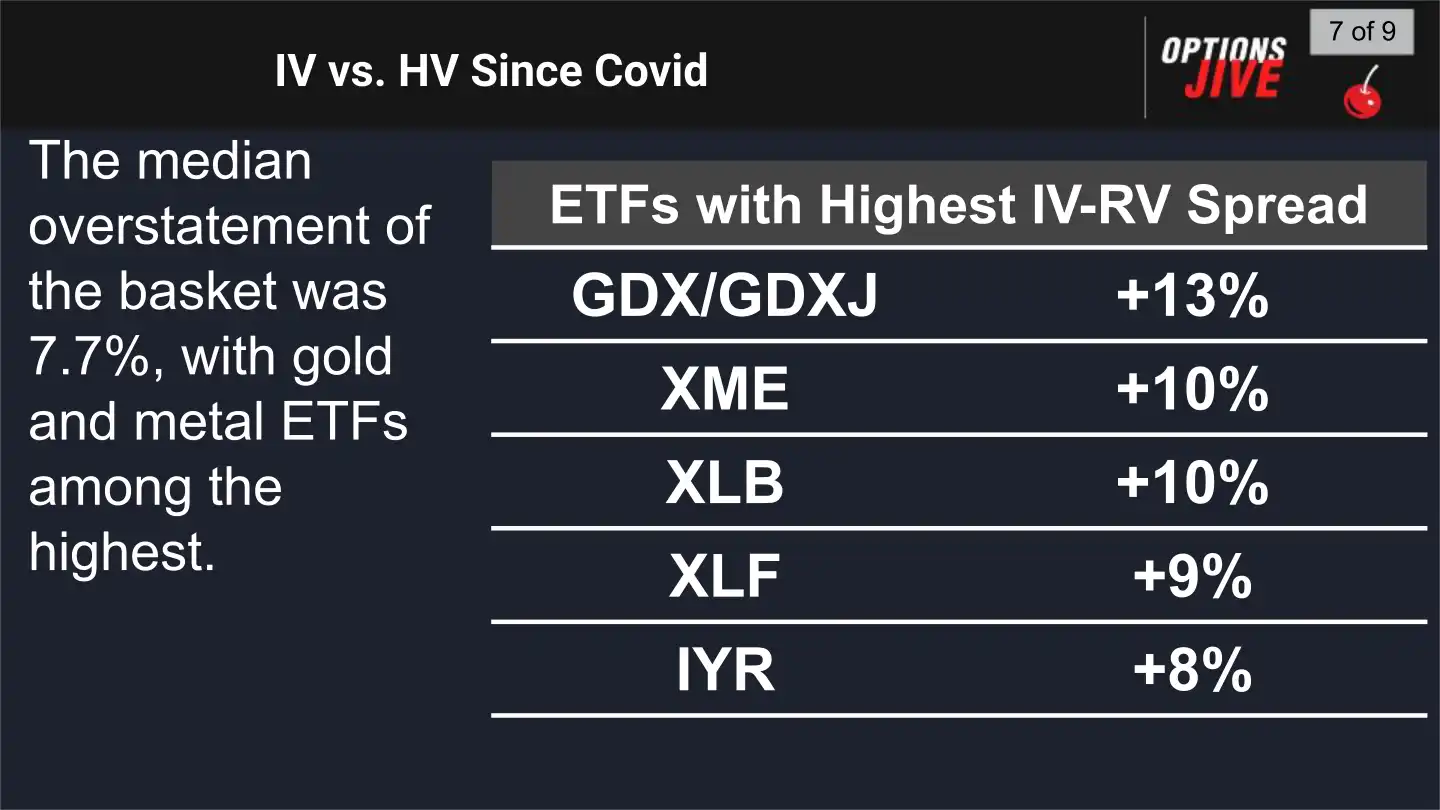

Through that analysis, tastylive found that the degree of overstatement between implied volatility and realized volatility widely varied across sectors.

For example, gold-focused ETFs showed some of the highest overstatement between implied volatility and historical volatility, as did basic materials and the financials.

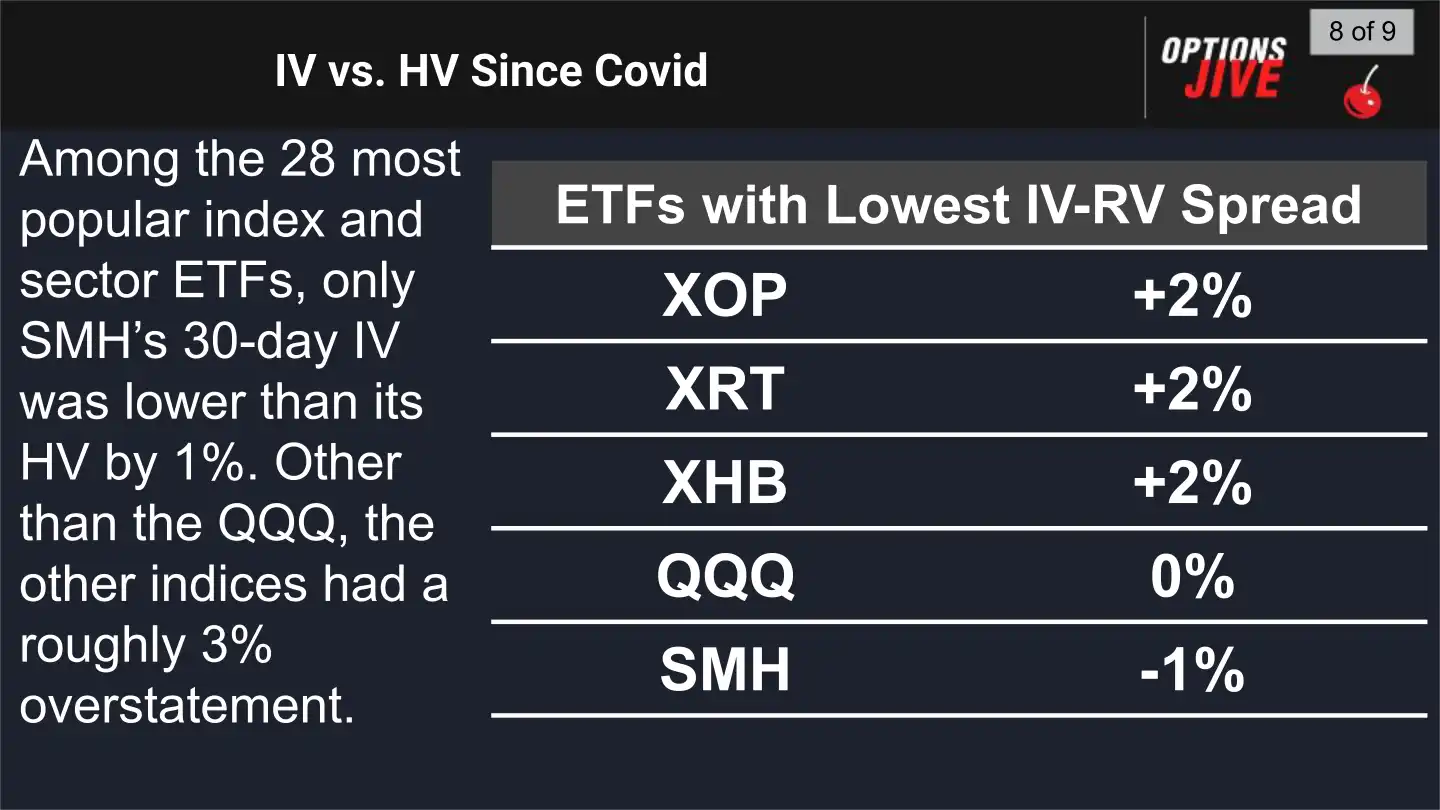

On the other side of the spectrum, some of the sectors showing the least overstatement between implied volatility and actual volatility were technology and energy. The findings from that sector analysis are highlighted below.

The degree of overstatement in the options market varies widely by market sector. And in any given year, it’s difficult to predict which sectors might see the greatest overstatement in premium.

That’s one reason some investors and traders choose to deploy short options strategies in broad diversified products, such as SPY. However, depending on one’s specific market outlook and trading approach, there may be instances when a particular ETF or single stock also looks attractive for selling premium.

To learn more about using implied volatility rank (IVR) to help identify potential opportunities in the options market, check out this new installment of Options Jive on the tastylive financial network.

For more context on the aforementioned research into implied volatility and historical volatility, check out this link. Daily market updates are also available via tastylive, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastylive or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.