4 Key Market Events to Watch in December

These four major market events will heavily influence where the markets trade during the final month of 2022 and beyond

December is traditionally a quiet month in the financial markets, but after an extremely volatile year of trading, the last month of 2022 could be more chaotic than usual.

At present, there are four key market events scheduled for December, and each of them could catalyze a significant move in the major market indices.

The first event arrives imminently, with the November employment report due on Friday, Dec. 2. After that, the focus shifts immediately to the November inflation report, which is due on Dec. 13.

Coincidentally, the last meeting of the Federal Reserve in 2022 is also set to kick-off on Dec. 13, with the group’s final decision on interest rates scheduled to be announced on Dec. 14.

Anxiety in the markets is also elevated at this time because of a looming strike by railroad workers. Unless a deal is reached in the next two weeks, roughly 115,000 railroad workers are scheduled to walk off the job on Dec. 9.

Traditionally, the month of December is one of the least volatile months on the calendar, which means the second half of the month could be relatively quiet, assuming no additional events pop up on the calendar.

Additional information on each of the upcoming December events is detailed below.

Employment report, Dec. 2

The state of the U.S. labor market is always an important consideration for the financial markets. However, the monthly employment report has added gravity at this time because of heightened concerns over the health of the underlying U.S. economy.

As many are aware, the technology sector has announced significant layoffs in recent months, and many are now anxiously waiting to see if other business sectors are forced to follow suit.

Widespread layoffs are a red flag for the economy because deteriorating conditions in the labor market are almost always accompanied by economic recessions.

Investors and traders are also watching the monthly employment reports closely because this data influences decision-making at the Federal Reserve. For example, a weak employment report could cause the Federal Reserve to rethink its current hawkish stance.

On the other hand, a strong employment report may embolden the Federal Reserve to stay the current course (of aggressive rate hikes), which could in turn be bearish for the stock market.

Economists are currently forecasting that roughly 200,000 jobs have been added to the economy during the month of November, and that the nationwide unemployment rate will hold steady at 3.7%.

Railroad strike, Dec. 9

Generally speaking, the financial markets don’t like uncertainty, which is why the looming prospect of a strike by railroad workers in the U.S. represents another potential market catalyst in December.

Just two months ago the U.S. government intervened to help avert a strike. Unfortunately, railroad workers haven’t agreed to the terms negotiated back in September, and may walk off the job as soon as Dec. 9.

A nationwide strike, which would paralyze a significant portion of the U.S. supply chain, became more likely after two key railroad unions officially rejected the deal on Nov. 21.

If a deal isn’t agreed upon before Dec. 9, it would represent the first significant railroad strike in the U.S. since 1992. That one lasted only two days because the government intervened, and ultimately forced a solution upon the industry.

The railroad sector is somewhat unique because it plays such a critical role in the U.S. economy. Today, it’s estimated that a nationwide shutdown of the entire freight-related railroad system would cost the country upwards of $2 billion/day in lost productivity.

Strikes have been far less common in the last 75 years due to the passage of the Taft-Hartley Act in 1947. This legislation restricts the activities and powers of labor unions, and specifically authorizes the president to intervene in strikes (or potential strikes) that create a national emergency.

Today, however, the Railway Labor Act (RLA) tends to guide the U.S. government’s response to disagreements between owners and workers. This legislation empowers Congress to intervene in railroad-related labor disputes to help ensure that undue harm isn’t done to the underlying U.S. economy.

The RLA allows Congress to force a new labor contract on both parties, or to extend the existing labor agreement. As such, Congress will have options available to it should a strike in fact materialize on Dec. 9.

For more background on the prospect of a nationwide strike in the railroad industry, check out this new Luckbox article.

Inflation report, Dec. 13

Inflation has been a hot-button issue in 2022, and the next major government update on this topic is set to be released on Dec. 13.

Last month, the inflation report catalyzed an immense move in the major market indices, with the Dow Jones Industrial Average jumping by 1,200 points (3.7%) in a single session. On that same day, the S&P 500 was up 5.5%, while the Nasdaq Composite surged by 7.35%.

Whether the upcoming report on Dec. 13 will be equally impacting is anyone’s guess. Last month’s euphoria was driven by a cooler-than-expected rise in inflation during the month of October.

For October, the Bureau of Labor Statistics reported that the consumer price index rose 0.4%, which was slightly below the 0.6% estimate.

However, inflation forecasts for the month of November aren’t quite as rosy, which sets the stage for another big move in the indices if the upcoming announcement features some sort of surprise.

Current forecasts suggest that inflation during the month of November has been running slightly hotter than it was in October, with an expectation that the consumer price index rose by about 0.5% during November.

As illustrated below, the rate of inflation peaked in the summer of 2022, but has remained stubbornly high in the interim.

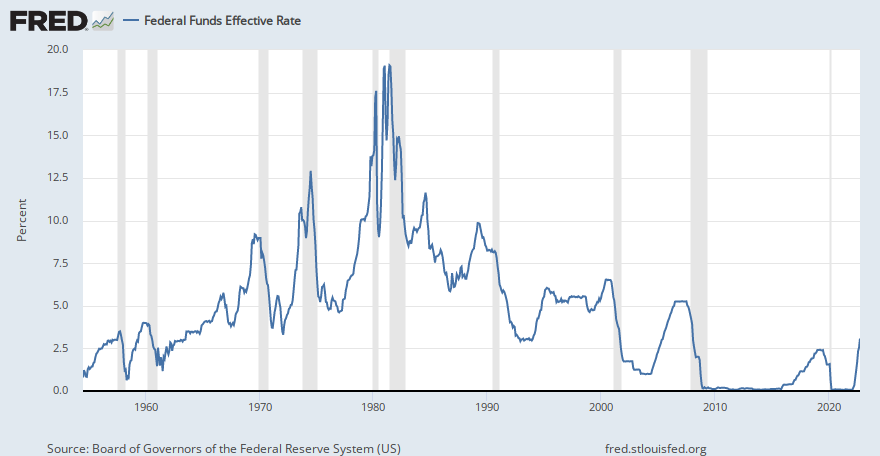

Fed decision on interest rates, Dec. 14

The Fed’s decision on interest rates is arguably the main event in December, and quite possibly the last key market catalyst of 2022.

The Federal Reserve is set to meet on Dec. 13, with the final decision on any forthcoming rate hike to be announced on Dec. 14.

Most projections suggest that the Fed will raise benchmark rates by an additional 0.50% in December. The current target on the federal funds rate is 3.75%-4.00%, which means an increase of 0.50% would move the target to 4.25%-4.50%.

Many believe the Fed’s ultimate goal is to raise the federal funds rate to about 5.0%, which means a couple of additional hikes may be forthcoming in Q1 2023. That said, ongoing performance in the economy, with particular emphasis on employment and inflation, will undoubtedly continue to influence future decisions taken by the Fed.

Barring some sort of major surprise, the U.S. will enter 2023 with the highest benchmark interest rates since 2007, as illustrated below.

To follow everything moving the markets during the remainder of 2022, monitor TASTYTRADE LIVE, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.