Macro Moves in 2024

Mexico is looking up, China down, and recession risk is "on"

A series of events sure to cause whiplash began in March when the failure of Silicon Valley Bank plunged credit markets into crisis. Wild swings continued past mid-year as U.S. debt-ceiling woes abated but stubborn inflation prompted central banks to raise interest rates. Then tragedy struck in October as war broke out in the Middle East.

What pitfalls lie ahead in 2024 is unclear. Nevertheless, here are two themes to keep in mind as the new year approaches: Mexico will strengthen its position as America’s biggest trading partner, and stock prices will be in danger from the threat of global recession and a possible debt debacle.

CHINA’S LOSS, MEXICO’S GAIN

Investors dreamed of a splashy recovery in the world’s second-largest economy as China began to scrap “zero-COVID” lockdowns in December 2022.

Meanwhile, the end of the Federal Reserve’s cycle of interest rate hikes came into view, so a lucrative 2023 seemed likely.

But that misplaced optimism soon dimmed.

China didn’t shake off its pandemic restrictions until more than a year after its main customers in the U.S. and Europe. By then, China’s clientele was busy switching to other supply chains.

Those markets had also come down from a pop of sharp catch-up economic growth linked to their own reopening, exhausting most of the stimulus money left in consumers’ pockets.

Combative central banks’ efforts to force down inflation didn’t help, either.

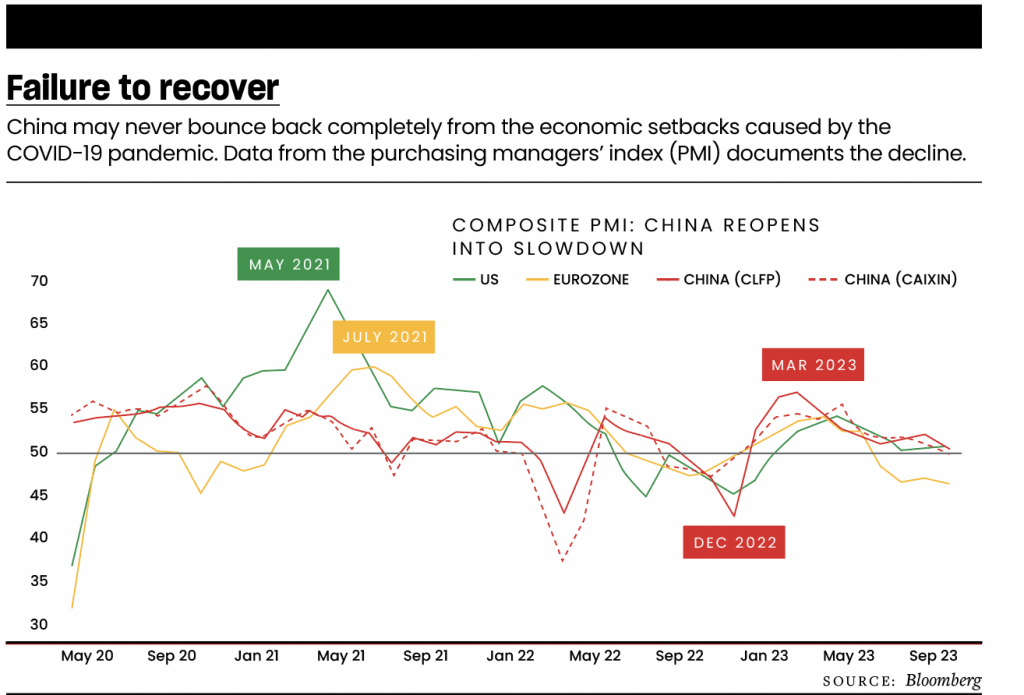

China loses plum position

As 2024 approaches, a brief upswell in the service sector has unraveled and economic growth has stalled. Growth in real gross domestic product (GDP) has ominously outpaced nominal expansion for two consecutive quarters, suggesting a yawning deflationary gap of close to 1.5%. That points to anemic economywide demand.

The way back to prosperity looks tenuous. China may have suffered lasting damage to its role as the go-to middle step in the global supply chain—the place where raw materials become finished goods and are shipped to rich-world consumers. Its share of worldwide trade volume has fallen to 12.7% from 15% in a mere three years.

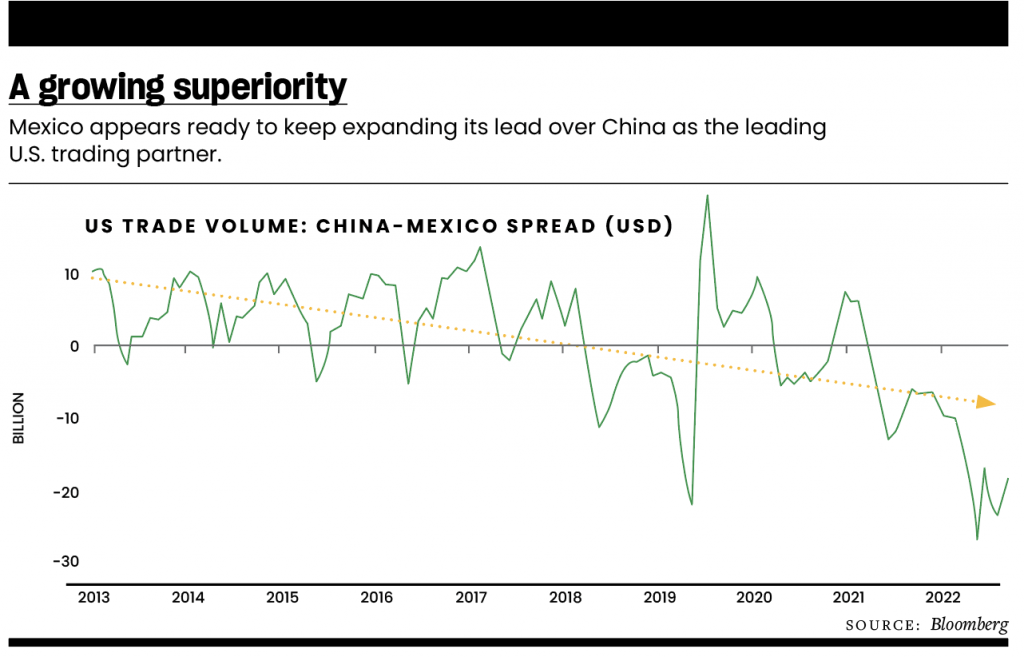

For the United States—which became China’s largest trading partner in 1998—a deepening rift over Beijing’s increasingly assertive geopolitics and Washington’s newly bipartisan appetite for mercantilism has spurred a search for alternatives closer to home. Mexico looks to be the prime beneficiary of this pivot.

Mexico’s time has come

Shifting supply chains from China to just south of the U.S. border offers a slew of benefits beyond sheer proximity to consumers.

Mexico’s largest population cohort is aged 10-25 years old, while China’s is 30-55 years old. Mexico’s birth rate is over 1.4 times higher. It spends 4.3% of GDP on education to China’s 3.6%, and its pupils are in school for an extra year on average. Meanwhile, a whopping 42% of Mexico’s population lives below the poverty line.

Put all this together and Mexico offers a younger, faster-growing and possibly more educated workforce at a lower price than China. Also, the U.S. and its southern neighbor already have a free trade agreement, making cross-border business comparatively easy and cost-effective. Therefore, it isn’t surprising Mexico already surpassed China to become the largest U.S. trading partner in 2022.

As this transition continues, assets linked to Mexico’s improving fortunes—like the iShares MSCI Mexico ETF (EWW) and the Mexican peso (MXN)—appear likely to outperform those anchored to China. These include popular funds like the iShares China Large Cap ETF (FXI) and the Xtrackers Harvest CSI 300 China A-Shares ETF (ASHR), as well as currencies like Australian dollar (AUD).

Currency markets to capture transition

Constructing a synthetic short Australian dollar to Mexican peso (AUD/MXN) position in the spot foreign exchange (FX) market by triangulating the two currencies’ exchange rates against the U.S. dollar may be the most straightforward way to gain exposure to the shift in capital flows underlying this historic change. The trade would call for selling AUD/USD and USD/MXN in comparable USD-equivalent size.

This ratio had been trending in the Aussie dollar’s favor since 1993 as China grew more dominant. It peaked in early 2021 and now looks to have broken the long-term trend. That sets the stage for a long-term push in the opposite direction.

STOCK MARKET: RISK ON

As 2023 draws to a close, Wall Street is cheering signs that the Federal Reserve is finished raising interest rates. That isn’t surprising. Telltale surveys of purchasing managers suggest global economic growth came to a standstill in October. A catch-all recession is almost certainly on the menu.

On the one hand, that situation makes it logical for investors to celebrate the end of a blistering rise in global borrowing costs and signs of an incoming turn in the opposite direction.

On the other hand, it warns that stocks’ heady gains may not continue beyond the very near term. Policymakers aren’t pivoting because things are going well, but quite the opposite.

Managing vast debt

Perhaps the scariest proposition is managing a historically large mountain of public- and private-sector debt at sharply higher interest rates. As of September 2023, the global debt stock stood at a record-high $307 trillion, according to the Institute of International Finance (IIF).

Not all or even most of this vast sum will roll over next year. Still, a pile this large and financed at far lower interest rates means issues with repayment are likely to appear even if a small share of the load comes due. Moreover, S&P Global estimates that about a third was incurred at floating rates, so servicing costs present a risk even before maturity.

That will become more onerous still as growth sputters. A rare benefit from surging inflation is that it helps make debts more manageable because debtors repay with money that inflation depreciated in real terms. Now, IIF data shows that the global debt-to-GDP ratio has ended a two-year decline as economic output stalls and inflation cools.

More of the same appears likely, making it harder for troubled borrowers to swallow pressure from higher funding costs. Stock markets will fall, and the U.S. dollar will rise if this becomes a forcing function triggering investors to liquidate portfolios and raise cash.

Trading the greenback’s exchange rate to the euro (spot EUR/USD or 6E futures)—the U.S. currency’s most liquid pairing—can offer broad-based exposure to its overall direction. Dialing up sensitivity to market-wide sentiment swings to capitalize on the risk-off mood might also make the Australian dollar (spot AUD/USD or 6A futures) an attractive vehicle.

Whatever happens with currencies, the coming year feels fraught with uncertainty. But staying mindful of factors like Mexico’s rise and the probability of recession can present opportunity and soften adversity.

Ilya Spivak heads tastylive global macro and hosts the network’s Macro Money show. @ilyaspivak