Lucid Motors Takeover Talk Triggers Sharp Rally

M&A activity slumped in 2022, but many industry experts expect a rebound in 2023 with Lucid Motors and other attractively valued companies

Mergers and acquisitions (M&A) can be a boon for investors and traders—assuming they find themselves on the right side of the deal.

That was certainly the case for investors in Activision Blizzard (ATVI) and VMware (VMW)—two tech companies that were acquired by Microsoft (MSFT) and Broadcom (AVGO) in 2022.

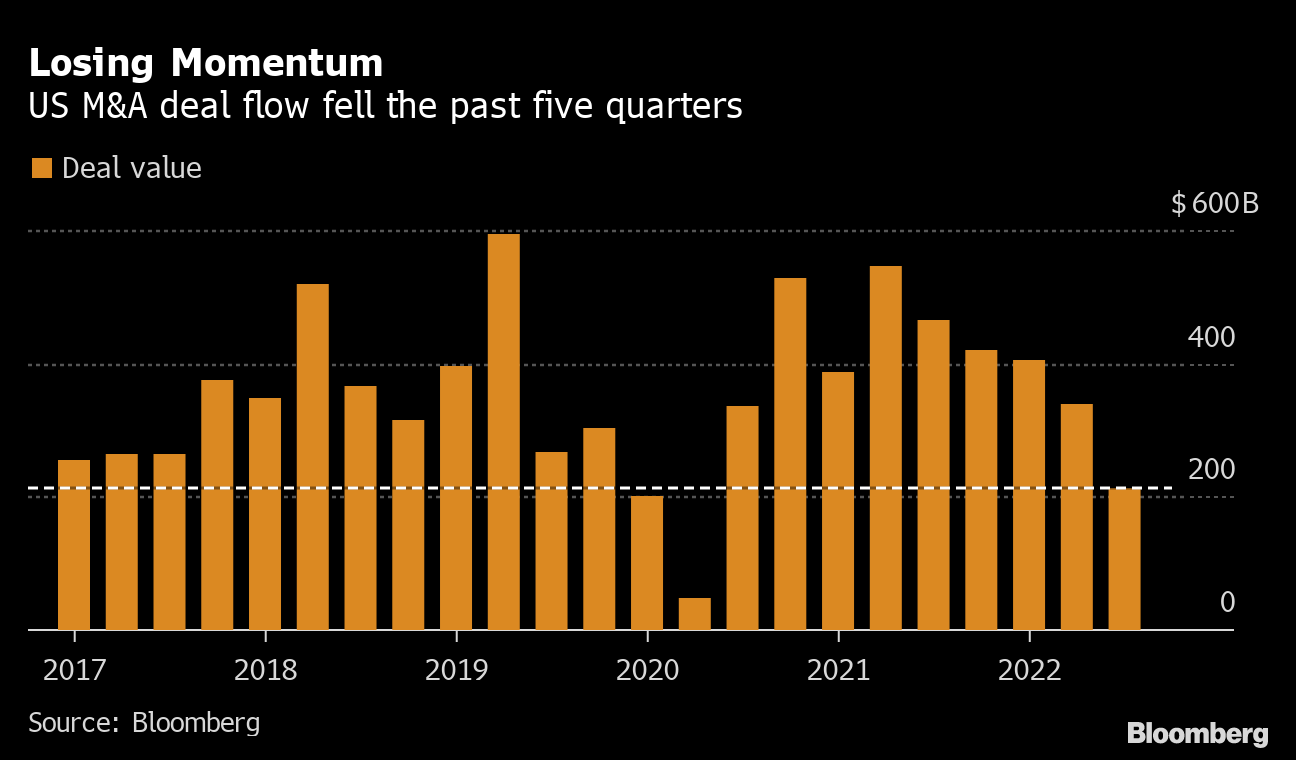

Overall however, M&A activity was relatively depressed last year. Data compiled by Refinitiv indicates that M&A-related dealmaking dropped by roughly 37% in 2022, as compared to 2021.

That said, industry experts expect M&A activity to rebound in 2023, as depressed valuations in the market—and a potential recession—help drive a fresh wave of consolidation in the corporate sector.

Backing up those forecasts, Lucid Motors (LCID) became the subject of a takeover rumor on Jan. 27.

LCID shares spiked as much as 63% that day after a report circulated that Saudi Arabia’s Public Investment Fund (PIF) was considering a full takeover of the U.S.-based manufacturer of electric vehicles (EVs).

LCID shares opened trading on Jan. 27 at roughly $9/share and closed the session at nearly $13/share. However, the intraday high was closer to $18/share.

The Saudi Public Investment Fund already owns 65% of Lucid and is reportedly considering a full takeover of the EV maker.

In 2022, Lucid produced about 7,200 EVs. To put the company’s size in perspective, Tesla (TSLA) produced roughly 5,000 EVs per day in Q4 2022. As of Jan. 29, Lucid is valued at about $24 billion.

Source: marketbeat.com

2023 M&A outlook

Whether Lucid is ultimately acquired in 2023 is anyone’s guess. But regardless of the particular deal, most industry experts expect M&A activity to rebound in 2023, as compared to last year.

In 2022, total global M&A sunk to $3.6 trillion, which represented a 37% decline as compared to 2021, according to Refinitiv data. That was the biggest drop in M&A activity year-over-year since 2001.

In 2023, lower market valuations—stemming from last year’s stock market selloff—are expected to make mergers and acquisitions relatively more attractive. Moreover, a slowdown in the global economy could help foster an environment that’s conducive to industry consolidation.

According to the Harvard Business Review, research conducted in the wake of the 2008-2009 Financial Crisis has shown that acquisitions made during economic downturns tend to outperform those made during normal or boomtime economies.

That’s because corporate valuations tend to suffer in recessions—sometimes to an outsized degree. This means acquisitions made during a recession or depression are somewhat similar to scooping a downtrodden stock amid a market correction, ahead of a rebound.

A comprehensive study conducted by PwC mirrored those findings, suggesting that acquisitions made during a downturn tend to outperform those made in normal or boomtime economies. The PwC research also indicated that dealmaking can slump during the early part of an economic contraction, but then surge in confidence as the economy is restored.

The fact that more businesses are often up for sale in recessions—as a result of the financial and emotional toll taken on owners—is another reason why M&A activity can pick up during an economic contraction.

Unfortunately, it’s never easy to predict exactly which companies will get acquired (or when), but investors and traders that keep close tabs on individual market sectors can undoubtedly put themselves in a better position to jump on emerging M&A targets.

Because the biotechnology niche of the financial markets is always one of the most active when it comes to M&A, that can be a natural place to start.

There have already been two big acquisitions in the biotechnology sector of the market in 2023, including the $6 billion purchase of LHC Group (LHCG) by UnitedHealth (UNH), and the $8 billion purchase of Signify Health (SGFY) by CVS Health (CVS).

On a much smaller scale, Shockwave Medical (SWAV) also acquired its peer Neovasc Inc. (NVCN) for $100 million.

To follow everything moving the markets on a daily basis, including the latest M&A activity, monitor tastylive, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastylive or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.