Trading the Next Big Inflation Report

Historical data illustrates that the stock market tends to underperform when a Federal Reserve rate hike cycle is accompanied by high levels of inflation.

Two big things are happening in the financial markets right now: interest rates are rising and the stock market is falling.

But those two trends aren’t necessarily linked—at least not in the way most might think.

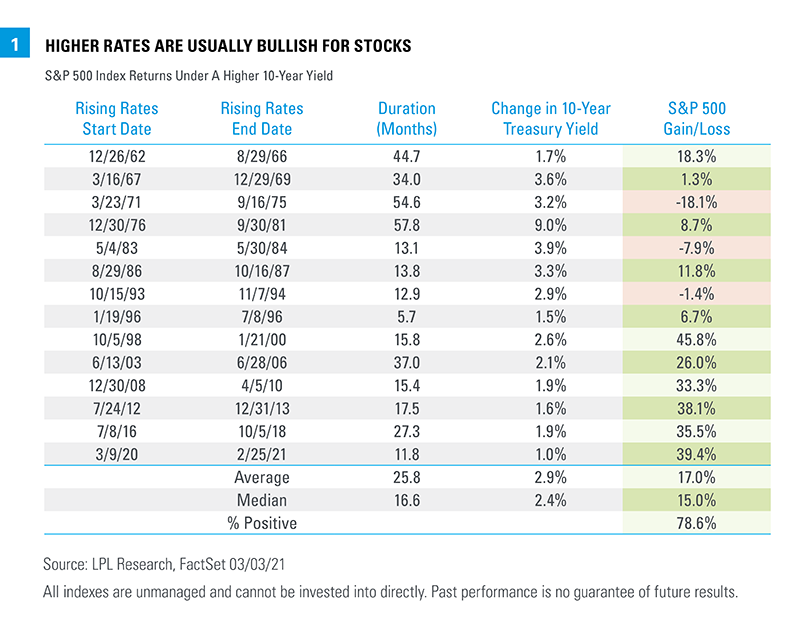

Historically, the stock market actually tends to perform quite well when interest rates are rising. According to research conducted by LPL Financial, the S&P 500 has returned on average +17% during periods in which the 10-year Treasury yield climbs by more than 1%.

As shown in the chart below, there have been 14 such instances going back to 1962.

Stocks typically perform well during these periods because interest rate hikes are usually accompanied by a strengthening in the underlying economy. And a growing economy is in turn good for stocks because of the positive impact on corporate earnings.

The difference in 2022 is that the Federal Reserve isn’t raising interest rates because the economy is strengthening.

This year, the Federal Reserve has been forced to raise interest rates in an effort to combat rampant inflation. And in contrast with many previous rate hike cycles, the underlying economy in the United States is actually deteriorating—although only moderately, for now.

Over the past two quarters, GDP growth in the U.S. has been slightly weak—Q1 saw GDP growth of -1.6%, while Q2 saw GDP growth of -0.6%.

GDP growth over the next two quarters is forecasted to be slightly better than Q1 and Q2, with a +0.3% growth rate expected in Q3. But in 2023, forecasts suggest the U.S. economy could be even more sluggish—with negative GDP growth potentially pushing the economy into a significant recession.

It’s that troublesome scenario—severe weakness in the economy—that is likely pushing the stock market lower in 2022, as opposed to just the rate hikes on their own.

According to research by LPL Financial, stock market performance is a lot weaker historically when a rate hike cycle is accompanied by red-hot inflation. For example, during rate hike cycles when the Consumer Price Index (CPI) was above 6%, the stock market returned on average -0.4%.

That level of return is considerably weaker than the +17% observed during all rate-hike cycles dating back to 1962.

In August 2022, core CPI in the U.S. was 6.3%. The fact that the current rate-hike cycle is accompanied by red-hot inflation helps explain why the stock market has been weak in 2022, at least in part.

Another important consideration this year is the rising threat of a significant recession. Historically, recessions and depressions have acted like a type of kryptonite for stocks.

Of the last 12 serious market corrections in the U.S. (listed below), only two did not coincide with an economic recession (1962 and 1987). Listed below are the 12 most recent significant market corrections in the U.S. stock market, including the month/year of the market bottom, and the trough decline of the market during that particular correction.

- May 1946 (-21%)

- June 1948 (-20%)

- October 1957 (-21%)

- June 1962 (-28%)

- October 1966 (-22%)

- May 1970 (-36%)

- October 1974 (-48%)

- August 1982 (-27%)

- December 1987 (-33%)

- October 2002 (-49%)

- March 2009 (-57%)

- March 2020 (-34%)

- March 2022 (-23%, year-to-date)

With the S&P 500 down 23% year-to-date, it appears that a contraction in the underlying economy has contributed to yet another serious market correction in the U.S. stock market.

The big question right now is whether the worst is yet to come.

A recession is generally defined as a state of economic contraction in which two consecutive quarters reflect a decline in gross domestic product (GDP). A depression, on the other hand, is generally regarded as a more pronounced recession, and one that lasts a lot longer.

Q1 and Q2 of 2022 both saw negative GDP growth, but those figures were by no means severe. That said, the Federal Reserve has indicated that it will likely raise rates two more times before the end of the year. That means higher rates could eventually take an even bigger bite out of the economy.

Economy uncertainty heading into 2023 is undoubtedly contributing to the current bout of weakness in the stock market.

Going forward, the performance in the underlying U.S. economy, as well as ongoing inflation readings, will likely play a role in where the market trades from here.

If inflation starts to cool, and the economy remains relatively strong, then the stock market could rebound quickly. But if inflation remains hot, and the economy contracts in severe fashion, then the stock market could fall further—a move that could push the S&P 500 below 3,600.

Investors and traders should therefore be following the monthly inflation reports closely, as well as ongoing projections for U.S. GDP growth. Currently, the CPI report for the month of September is scheduled to be released on Oct. 13 at 8:30 a.m. EDT.

For more perspective on how red-hot inflation is affecting the financial markets, watch this new episode of Jones and Friends on the tastytrade financial network. For daily updates on everything moving the markets, check out TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.