Best Pot Stocks? Several are Rallying as Cannabis Becomes Sixth-Largest Cash Crop in the U.S.

Farmers in the U.S. grew roughly 2,800 metric tons of cannabis in 2022, making this commodity the country’s sixth most valuable cash crop by total annual production

- In 2022, American farmers grew roughly 2,800 metric tons of cannabis.

- Cannabis now represents the sixth most valuable cash crop in the United States by annual production.

- Cannabis prices have been trending lower since the start of 2022, but despite that headwind, some single stocks in the cannabis sector have posted strong gains in 2023.

The legal cannabis sector in the United States has made significant strides since the late 1990s, when California became the first state in the country to legalize it for medicinal use.

In fact, growth in the sector has been so robust over the last decade that cannabis now represents the sixth most valuable crop in the United States, by total annual production.

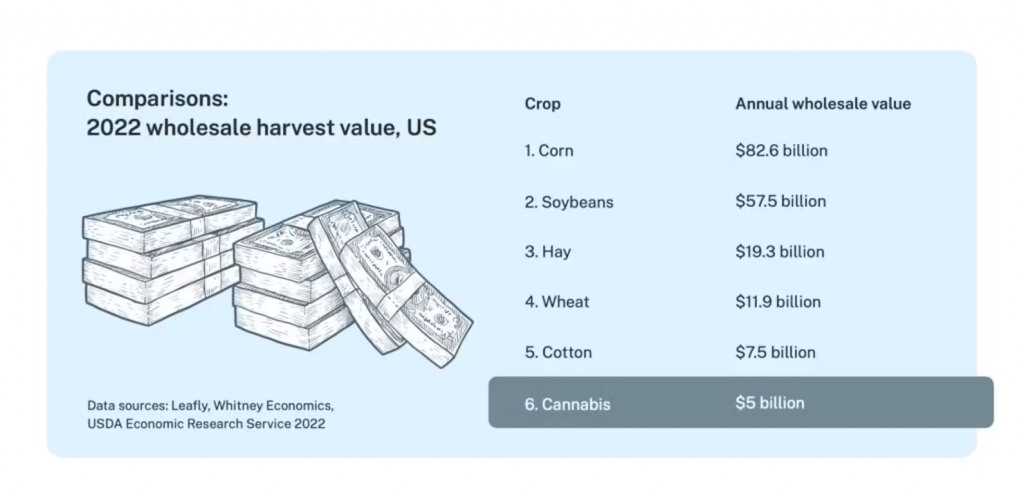

According to the 2022 Leafly Cannabis Harvest Report, farmers in the U.S. grew roughly 2,800 metric tons of cannabis in 2022. For context, one metric ton of cannabis equates to about a million one-gram joints.

And with an estimated 2022 harvest value of $5 billion, that means total annual cannabis production in the U.S. is now more valuable than that of potatoes and rice, but still behind the likes of corn, soybeans, hay, wheat and cotton, as illustrated below.

Interestingly, the cannabis harvest in 2022 was actually about 24% larger than 2021, but the overall value of the harvest fell by about $1 billion year-over-year, due to lower realized prices.

The last couple of years have been especially tumultuous for prices in the legal, adult-use cannabis market. But the primary trend has been a steady weakening in wholesale prices.

In 2018 and 2019, the average retail price for an ounce of marijuana consistently traded above $400/ounce. However, in 2022, prices started moving incrementally lower—first dropping below $350/ounce, and then dipping below $300/ounce by late summer. During a few brief periods in 2022, the price even dropped below $200/ounce.

And those figures match closely with price trends observed in Canada, where wholesale prices dropped by about 40% last year, according to MJBizDaily.com.

In 2023, prices have stabilized somewhat—the Daily Mail reported in April that the national average for an ounce of “high-grade” cannabis in the U.S. was trading for about $315/ounce, whereas an ounce of “regular” cannabis was trading closer to $250/ounce.

However, it’s important to note that prices can vary widely by state, due to taxes, quality and supply/demand.

For example, in April of this year, an ounce of “top-notch” cannabis was trading for about $210/ounce in Portland, Oregon. But on the other side of the country, prices in Washington D.C. were closer to $590/ounce.

The market for cannabis in the U.S. is especially difficult to ascertain (and predict) because the substance remains illegal at the federal level, which effectively eliminates the potential for interstate commerce. For this reason, supply and demand dynamics in a given state can heavily influence prices.

And, as evidenced by the wide gulf between prices in Oregon versus Washington D.C., varying state-level dynamics effectively translate to a fragmented market. The current paradigm won’t change until cannabis is finally legalized at the federal level.

As one might expect, the recent decline in prices has represented somewhat of a headwind for the cannabis niche of the stock market. Over the last 52 weeks, the Global X Cannabis ETF (POTX) is down roughly 52%. Year-to-date, POTX is down 33%.

However, the news hasn’t been all bad. The global cannabis sector is expected to grow rapidly in the coming years, with one forecast indicating it could grow from $28 billion in 2022 to $82 billion by 2027.

As a result of that future potential, some single stocks in the sector have soared in 2023, as highlighted in the list below:

- Ayr Wellness (AYRWF), +113%

- Verano Holdings (VRNOF), +54%

- Green Thumb Industries (GTBIF), +30%

- AdvisorShares Pure US Cannabis ETF (MSOS), +18%

- Cresco Labs (CRLBF), +17%

- Curaleaf Holdings (CURLF), +12%

- AdvisorShares Pure Cannabis ETF (YOLO), -1%

- Amplify Seymour Cannabis ETF (CNBS), -2%

- Sundial Growers (SNDL), -5%

- Alternative Harvest ETF (MJ), -6%

- Tilray Brands (TLRY), -11%

- Cronos (CRON), -12%

- Trulieve Cannabis (TCNNF), -13%

- Global X Cannabis ETF (POTX), -33%

- OrganiGram Holdings (OGI), -49%

- Canopy Growth (CGC), -55%

It should be noted that many of the stocks listed above have relatively low market capitalizations, and may not trade with robust liquidity. In such cases, investors and traders often gravitate toward sector ETFs, such as the aforementioned Global X Cannabis ETF (POTX), or the Alternative Harvest ETF (MJ).

Aside from prices, one of the key narratives influencing the cannabis sector is the ongoing battle to legalize marijuana at the federal level. For more background on the cannabis trade, readers can check out this installment of Market Measures on the tastytrade financial network.

To follow everything moving the markets this year, including the options markets, tune into tastylive—weekdays from 7 a.m. to 4 p.m. CDT.

Hungry for more? The next issue of Luckbox is food-focused looking at new growth opportunities and trading ideas in food, beverage, agricultural, hospitality and grocery stocks. Not a subscriber? Subscribe for free at getluckbox.com.

Andrew Prochnow has more than 15 years of experience trading the global financial markets, including 10 years as a professional options trader. Andrew is a frequent contributor Luckbox magazine.