Economic Optimism Pushes Crude Oil Prices to 12-Month Highs

Hopes for a strong economic recovery in 2021 have boosted the fortunes of crude oil, which has rallied more than 30% during the first couple months of the new trading year.

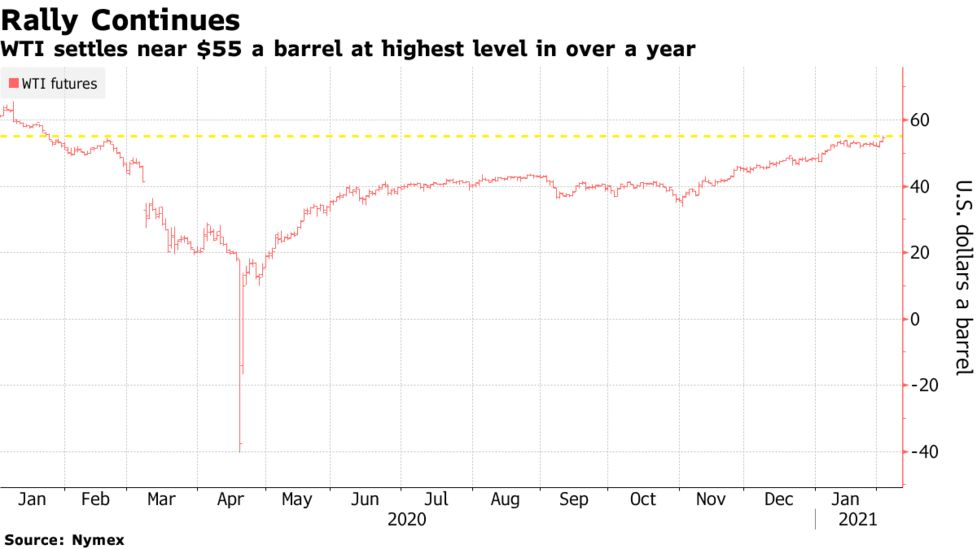

At the outset of the COVID-19 pandemic, crude oil prices nose-dived as declining economic activity greatly reduced demand for the world’s most heavily traded energy commodity.

In Q1 of 2020, the contraction in global oil demand was so severe that futures prices briefly traded in negative territory (the first time in history).

With vaccines now being administered globally, many economists are predicting that a broad-based economic recovery could take hold in 2021. That optimism has clearly spilled over into the energy sector, illustrated by the strong rally in oil prices during the first two months of the year.

Since the start of the year, crude oil prices have increased by an impressive 35% and are currently trading nearly $62/barrel. The chart below highlights oil’s fantastic journey since the start of 2020.

Rising demand expectations are undoubtedly responsible for a large portion of the above rally, but in the commodities business, the supply side of the equation also typically plays a big role in price direction.

In the case of crude oil, bullish supply-side factors can also be tied back to the onset of the pandemic.

When demand started tailing off last year, many global oil producers responded by cutting production in an attempt to reduce costs and maintain profitability. As a result, a large portion of pre-pandemic daily oil production was taken offline—a reality that is undoubtedly contributing to the upward trajectory in prices at this time.

As many are aware, the Organization of the Petroleum Exporting Countries (OPEC) wields considerable influence over the price of oil. In recent years, OPEC countries have worked in a highly coordinated fashion to closely control the amount of oil reaching the market. The ultimate goal, of course, is to control prices.

Prior to the pandemic, OPEC had even pulled Russia into the cartel (now known as OPEC plus, or OPEC+) to widen the group’s influence. OPEC+ agreed last year to sharply cut production in response to plummeting demand. With prices now recovering, it’s expected the group will meet again soon to renegotiate ongoing production targets.

The result of those negotiations, and the ultimate stance adopted by OPEC going forward, will consequently play a key role in the future price of oil.

Some projections suggest crude oil could rise above $75/barrel in the next several months. But it’s difficult to accurately predict future prices without additional supply guidance from OPEC and more insight on the potential economic rebound.

During the fourth quarter of 2020, U.S. gross domestic product (GDP) grew about 4%. Current projections suggest that U.S. GDP could grow another 6%-8% during Q1 2021.

If actual Q1 growth comes in significantly higher than that, one could imagine crude oil rallying further, even if OPEC does increase production. One can’t forget that extra oil doesn’t just magically appear in the market, it takes a significant amount of time for oil companies to ramp up production.

Due to its ubiquity, oil exposure is easy to find in the market—whether through single stocks, exchange-traded funds (ETFs), options or futures.

Two of the best-known oil ETFs, the Energy Select Sector SPDR Fund (XLE) and the VanEck Vectors Oil Services ETF (OIH), are already up 28% and 21% year-to-date, respectively. For reference, the CBOE Crude Oil Volatility Index (OVX) is currently trading about 40.

To learn more about trading the oil sector, check out a previous installment of Futures Measures on the tastytrade financial network.

An archived episode of Futures Measures should also prove useful for anyone seeking to learn more about trading energy futures. As always, daily market coverage is also available via TASTYTRADE LIVE, weekdays from 7 a.m. to 4 p.m. Central Time.

Subscribe to Luckbox in print and get a FREE Luckbox T-shirt! See SUBSCRIBE or UPGRADE TO PRINT (upper right) for more info.

Sage Anderson is a pseudonym. The contributor has an extensive background in trading equity derivatives and managing volatility-based portfolios as a former prop trading firm employee. The contributor is not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about any of the topics covered in this blog post, or any other trading-related subject, to support@luckboxmagazine.com.