Hawkish Fed Stirs Up Fresh Volatility in Financial Markets

Recent reports suggest the Federal Reserve will stick to its hawkish stance on interest rates over the foreseeable future, with benchmark rates expected to increase by 1.25% through the end of July.

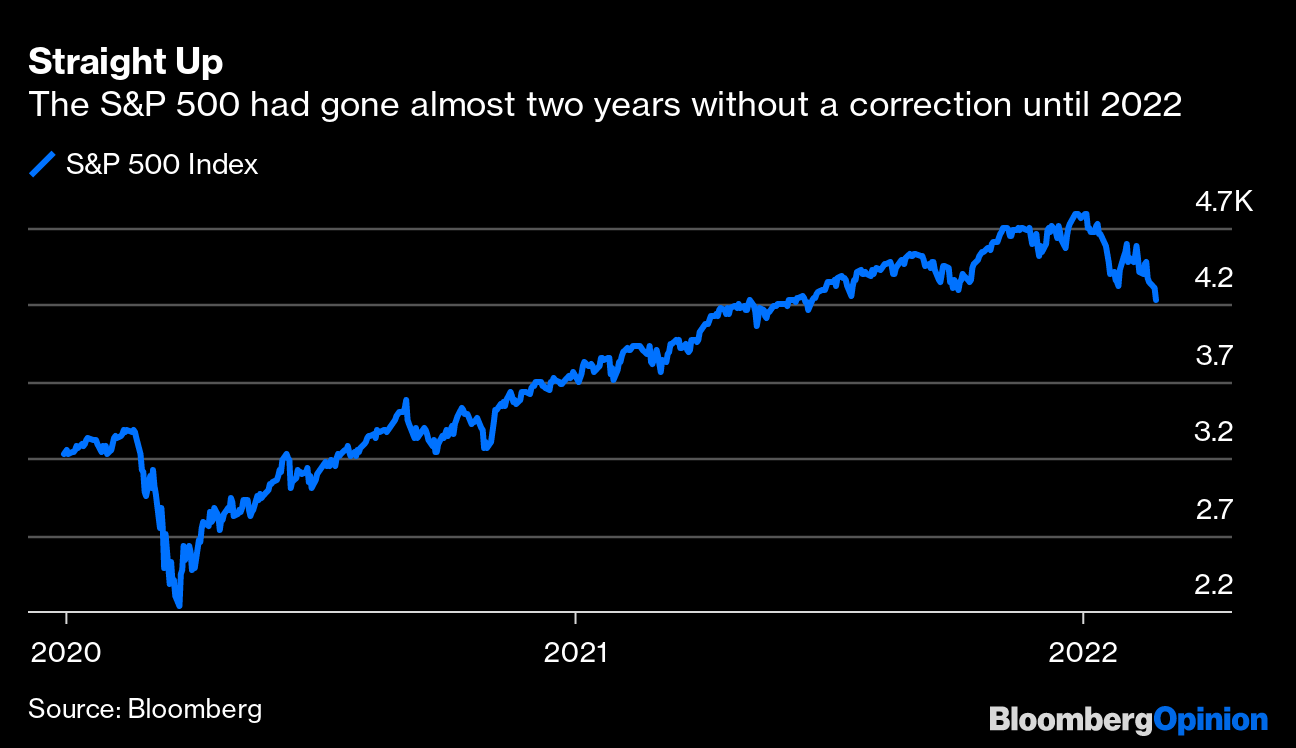

The stock market rollercoaster of this year continued last week after hawkish comments from the Chairman of the Federal Reserve sent prices spiraling lower on April 21 and 22.

The financial markets had already been in turmoil this year due to continuing supply chain issues linked to the COVID-19 pandemic, as well as the outbreak of full-scale war in Eastern Europe.

Prior to last week, the S&P 500 had recaptured a good chunk of the losses it sustained when Russia expanded its conflict with Ukraine in February. The S&P 500 hit its 2022 closing low of roughly 4,170 on March 8, which was about 13% lower as compared to the start of the year.

However, from March 8-28, the S&P 500 appeared to shrug off negativity associated with the war and rallied all the way back to 4,600.

A rally that stalled after reports started circulating last week that indicated the Federal Reserve was planning to be more aggressive than originally expected in its pursuit to tame inflation.

Expectations now suggest the Fed could raise benchmark rates by 1.25% over the course of its next three meetings, ultimately pushing the federal funds rate up to 1.50% by the end of July. The first stage of that plan was seemingly confirmed by Fed Chairman Jerome Powell on April 21, when he said, “I would say 50 basis points will be on the table for the May meeting.”

The next major meeting of the Federal Open Market Committee (FOMC)—the group charged with overseeing most of the central bank’s most important operations—is slated for May 3-4. Subsequent meetings this summer are already set for June 14-15 and July 26-27.

The chart below highlights how the interest rates swaps market now expects benchmark rates to climb above 2% by the end of 2022.

One of the biggest concerns lately is that the Fed now intends to use rate hikes to tame inflation, no matter what the data says about the underlying economy. That means in relative terms, the possibility of a near-term recession has increased marginally.

The day after Chairman Powell voiced his hawkish comments, the stock market fell hard, with the S&P 500 and the Dow Jones both dropping by nearly 3% on April 22.

Rising rates environments are often viewed as a negative for the corporate sector because that type of trend effectively makes financing more expensive and can in turn compress profitability.

However, some measures suggest that corporate profitability is currently at record highs, a factor that may have equipped the Fed with the confidence it needs to stay aggressive.

Data from Factset recently revealed that companies in the S&P 500 had booked a collective net profit margin of 12.18% over the last 12 months—a record high in the metric.

That degree of profit is especially interesting when one considers that American consumers have been dealing with record rates of inflation for quite some time. This data suggests that American businesses have been passing along a good chunk of increased costs to consumers, as opposed to absorbing them on their own.

With American consumers now stretched thin, the Fed might see its current plan to raise rates as a way of playing hardball with American businesses. During the remainder of 2022, the corporate sector will likely have to accept lower levels of profitability or be forced to deal with a deteriorating consumer environment—the latter of which could ultimately push the U.S. economy back into recession.

Earnings reports from the current quarter haven’t been as rosy as expected, which suggests that the corporate sector could be shouldering a larger share of the inflation burden. So far, Q1 earnings season has seen some positive surprises, but slightly less positive than the five-year average.

Over the past five years, earnings surprises have been on average 9% higher than estimates, but that percentage has now dropped to around 8%. That’s a subtle difference, but it may represent the start of a more significant trend.

The last two major recessions in the U.S. have coincided with significant corrections in the stock market (2008-2009, 2020). Those historic trends may help explain why the major market indices are back near 2022 lows.

To learn more about trading interest rates, readers can review this installment of Market Measures on the tastytrade financial network.

For updates on everything moving the markets, readers are also encouraged to tune into TASTYTRADE LIVE, weekdays from 7 a.m. to 4 p.m. CDT.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.