Here is What You Need to Know to Trade the Biggest Market Events in January

January 2023 is full of key market events, with reports on employment, inflation and corporate earnings set to be released the first two weeks of the year

For active investors and traders, the start of a fresh trading year is always an exciting time. In 2023, the action gets underway almost immediately, as January features the start of quarterly earnings season, which is slated to start on Jan. 13.

There are two important dates to keep in mind before earnings—Jan. 6 and Jan. 12.

On Jan. 6, the U.S. Bureau of Labor Statistics will release its monthly jobs report. Next up is the inflation report on Jan. 12.

Then, at the end of January, the Federal Reserve is scheduled to meet for the first time in 2023. That two-day meeting will take place on Jan. 31 and Feb. 1. Additional details on each of the upcoming events are highlighted below.

Employment Report, Jan. 6

The state of the labor market is always an important consideration on Wall Street. But with the economy on weak footing, the upcoming employment report has added gravity.

At the end of December, the Federal Reserve announced that it expects the unemployment rate in the U.S. to expand from roughly 3.7% (where it is today), to between 4.5-5.0% in 2023.

The market will be watching closely to see if that prediction comes true, which is why the monthly employment reports will be so important this year.

The Jan. 6 report will provide a summary of the employment data from December 2022. During the month of November, nonfarm payrolls (the measure of the number of workers in the U.S. excluding farm workers and those in other job classifications) in the U.S. increased by 263,000—slightly less than the 284,000 jobs added in October, as illustrated below.

While the report could show positive gains, most experts expect the economy will start hemorrhaging jobs at some point in 2023.

Inflation Report, Jan. 12

Inflation was a key theme during the 2022 trading year, and it will undoubtedly remain a key focus in 2023. For this reason, most investors and traders will be waiting anxiously for the first government update on inflation.

The last two reports—summarizing inflation data from October and November 2022—indicated that inflation had cooled slightly as compared to the summer. But it’s important to recognize that inflation is still running extremely hot by historical standards.

As part of its so-called dual mandate on employment and inflation, the Federal Reserve targets an annual inflation rate of 2% in the U.S. economy. With inflation still running well above 7%, it’s easy to see why anxieties over record-high inflation remain high, and why the Federal Reserve is working so hard to rein it in.

Current Federal Reserve projections indicate that inflation could revert to normal levels by the end of 2023, and based on historical data, that appears to be a reasonable expectation.

However, the future is always uncertain, and other challenges may arise that could cause disruptions to the global economy. Under that scenario, inflationary pressures could persist for longer than the Federal Reserve currently anticipates.

Earnings Season, Jan. 13

Earnings season for Q4 is set to ramp up on Jan. 13, when several of the country’s largest financial institutions are set to release their financial results for the last quarter of 2022. On the 13th, Citigroup (C), JPMorgan (JPM) and Wells Fargo (WFC) are scheduled to announce their quarterly earnings before the market opens.

Traditionally, earnings season kicks off with Alcoa (AA), but in recent years, the big financial companies have stolen Alcoa’s thunder, and typically report ahead of the aluminum titan. For reference, Alcoa is scheduled to report earnings on Jan. 18.

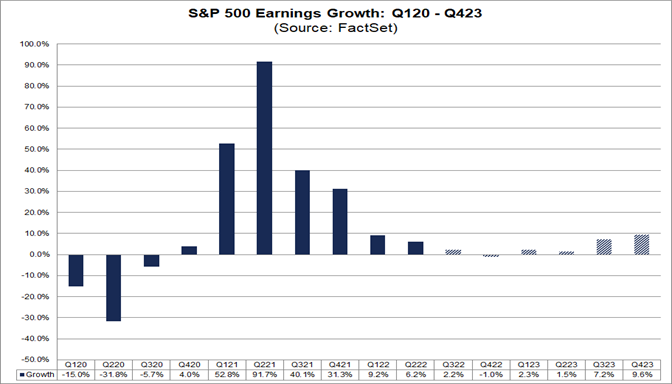

Quarterly earnings season is a critical period for the stock market because profits and revenues play a big role in stock market valuations. When corporate profitability is robust, stock prices usually move higher. The reverse is true when earnings growth stagnates, or even worse, moves into negative territory.

In 2022, profitability in the corporate sector declined, which may help explain why the S&P 500 dropped roughly 20%. As of now, many projections suggest earnings growth will turn negative in H1 2023 for the first time in two years.

The last time earnings declined on a year-over-year basis was Q3 2020, when the global economy was still reeling from the onset of the COVID-19 pandemic. Importantly, however, the forthcoming earnings slump could be short-lived.

As illustrated below, projections compiled by FactSet suggest earnings growth could turn positive again as soon as H2 2023.

When corporate profitability slumps, companies typically compensate by cutting back on expenses. That process usually leads to layoffs, as organizations attempt to operate with leaner overhead. In 2022, the technology sector was the first to start cutting jobs, but other sectors have also followed suit.

As of early December, the financial industry had laid off about 18,000 employees in 2022, which was more than double the total figure from 2021. In comparison, the tech sector saw more than 150,000 layoffs in 2022.

Q4 earnings season will provide important insight into the current business environment, and whether additional layoffs may be forthcoming.

Federal Reserve Decision on Interest Rates, Feb. 1

The Federal Reserve will meet for the first time in 2023 on Jan. 31, and the Fed’s decision on interest rates will be announced at 1 p.m. CDT on Feb. 1.

In December, the Federal Reserve raised benchmark rates by half a percentage point, bringing the target range to 4.25%-4.50%. That’s the highest level observed in the federal funds rate since 2007.

Current projections suggest the Fed will raise benchmark rates above 5% during 2023, which means another half-percentage point hike may be coming on Feb. 1.

The likelihood of another half-point hike increased recently, after the U.S. government announced that Q3 GDP for the country was +2.6%. That figure represents somewhat of an upside surprise, because economic growth in the U.S. during the first half of 2022 was basically flat.

With GDP trending higher, the Fed will likely feel more confident to stay the current course. But when the group meets for the second time in 2023—on March 15 and 16—the outcome could be more uncertain.

For more about getting active trading in 2023, check out the latest Luckbox issue, now live on the home page at luckboxmagazine.com.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastylive or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.