Trading Volatility in Fear-Driven Markets

Spikes in the CBOE Volatility Index (VIX) can cause fear in the marketplace, but historical data shows that such situations may represent an attractive opportunity to sell options premium.

All market participants are different, and every investor and trader has their own preferred market conditions.

Traditional long-only investors obviously love bullish trading environments. And short players love corrective trading environments—similar to what’s been observed in the global indices since late November.

Due to the dynamic nature of options, participants in the options market tend to thrive in a wide variety of market conditions. However, short options players tend to get really excited (and engaged) when market volatility is rising.

On Dec. 1, the CBOE Volatility Index (VIX) closed above 30 for the first time since Feb. 1, and it looks like the infamous “fear gauge” could remain elevated heading into 2022.

During tumultuous periods in the financial markets, risk premiums tend to increase—as observed through increasing levels of implied volatility. In essence, that means options premiums are getting richer, and relatively more attractive to sell.

However, with markets making bigger swings, investors and traders may be more hesitant to sell options, due to the risk profile of such positions. But despite that natural hesitancy, research conducted by tastytrade suggests it’s not necessarily the risks that increase during a correction, but rather the potential rewards.

That’s because the market is unpredictable, and can theoretically make a big move at any time. Considering that reality, one would obviously prefer to sell options premium when it’s relatively more expensive (i.e. during periods of elevated implied volatility).

However, pulling the trigger to “sell fear” amidst a market downturn isn’t necessarily easy. That’s one reason that objective market research is so useful, because it provides the quantitative foundation necessary to back up a so-called gut feeling.

Along those lines, the tastytrade network recently published a new market study that examines the historical success rate of a short options approach across a variety of market environments.

Spoiler alert, short options performance tended to improve as the severity of the correction intensified—primarily due to the fact that options prices are richer during these periods.

In order to evaluate this question, the tastytrade research team constructed a market study incorporating the following parameters:

- Utilized data in the SPDR S&P 500 ETF Trust (SPY) from 2005 to present

- Backtested short straddle performance (16 delta straddles) with 45 days-to-expiration

- Managed all trades at 21 days (i.e. closed each position after 21 days)

- Segmented results based on market environment (any day, any down day, 1% correction, 2% correction, 3% correction)

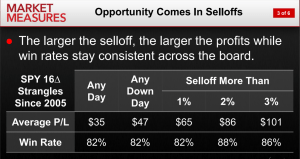

This series of backtests revealed that the win rates and average P/L from short straddles tended to increase along with the veracity of the correction. The image below provides a snapshot of the summarized results from the aforementioned backtests.

As one can see in the data above, the larger corrections tended to produce more attractive win rates and average P/Ls.

Further research conducted by tastytrade revealed that this was mostly due to the fact that option prices were higher during these periods, thus providing more protection for premium sellers, as illustrated below.

While the short premium approach has demonstrated attractive results across all market environments, this research helps illustrate why it becomes even more effective during periods of rising market volatility.

These findings dovetail well with previous tastytrade research that demonstrated the high historical success rate of selling puts in “blue chip” stocks after 5% corrections. To learn more about this trading approach, readers are encouraged to review this previous installment of Market Measures.

For more information on the short options trading philosophy, readers can also review this new installment of Options Jive.

For timely updates on everything moving the financial markets, readers can also tune into TASTYTRADE LIVE—weekdays from 7 a.m. to 4 p.m. CST—at their convenience.

Sage Anderson is a pseudonym. He’s an experienced trader of equity derivatives and has managed volatility-based portfolios as a former prop trading firm employee. He’s not an employee of Luckbox, tastytrade or any affiliated companies. Readers can direct questions about this blog or other trading-related subjects, to support@luckboxmagazine.com.